Baidu Blasts Off, Evergrande Restructures, RRR Cut, Week in Review

4 Min. Read Time

Week in Review

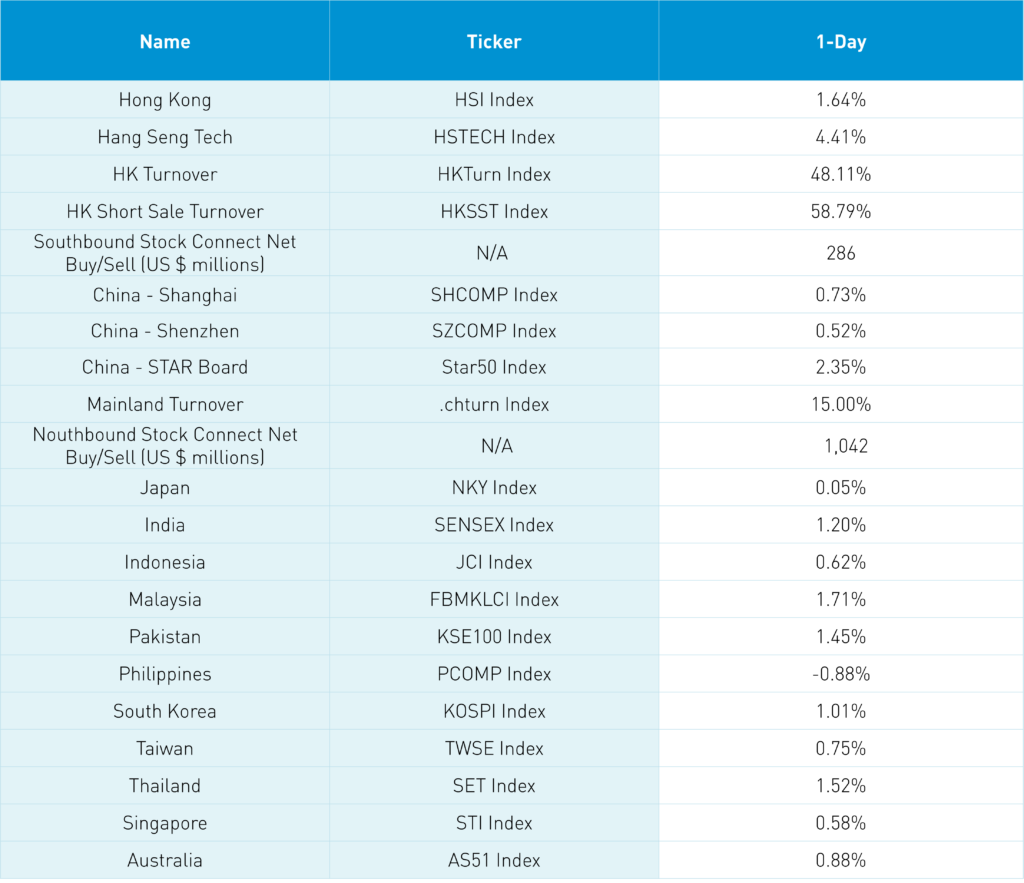

- Asian equities were mostly lower this week as the uncertain path of US Fed rates hikes and US turned global bank failures weighed on risk sentiment globally.

- The Public Company Accounting Oversight Board (PCAOB) is returning to China to finalize audits, demonstrating the good access that the US regulatory authority has been granted.

- China’s property and fixed asset investment figures came in above expectations for the first two months of the year.

- The “Two Sessions” political meetings concluded last weekend. In this week’s video update, Xiabing gives an introduction to the “Two Sessions” and interviews attendees on what they heard and expect to come out of the important policy summit.

Friday’s Key News

Asian equity markets ended the week up on high volumes driven by S&P Dow Jones and FTSE Russell indices rebalancing along with trading driven by the expiration of stock index futures, stock index options, stock options, and single stock futures derivatives, an occurrence known as “Quad Witching”. Big liquidity days like today are important to watch as they provide investors the opportunity to adjust portfolios thanks to the ample liquidity provided by these events.

US banks depositing cash at First Republic Bank helped investor sentiment. All this TikTok focus during a US banking crisis, which I would argue is crisis of confidence in the US government, is bewildering, though I digress.

There were several positive catalysts, though a key one occurred after the market’s close: the People’s Bank of China (PBOC), China’s central bank, cut the bank reserve requirement ratio (RRR), the amount of money banks need to hold in reserves, from 11% to 10.75%, which will allow banks to lend an additional $72 billion. It is difficult not to contrast China’s easing against the backdrop of the country’s continued reopening in light of the European Central Bank’s (ECB) rate hike yesterday and Fed’s likely 25 basis point hike next week.

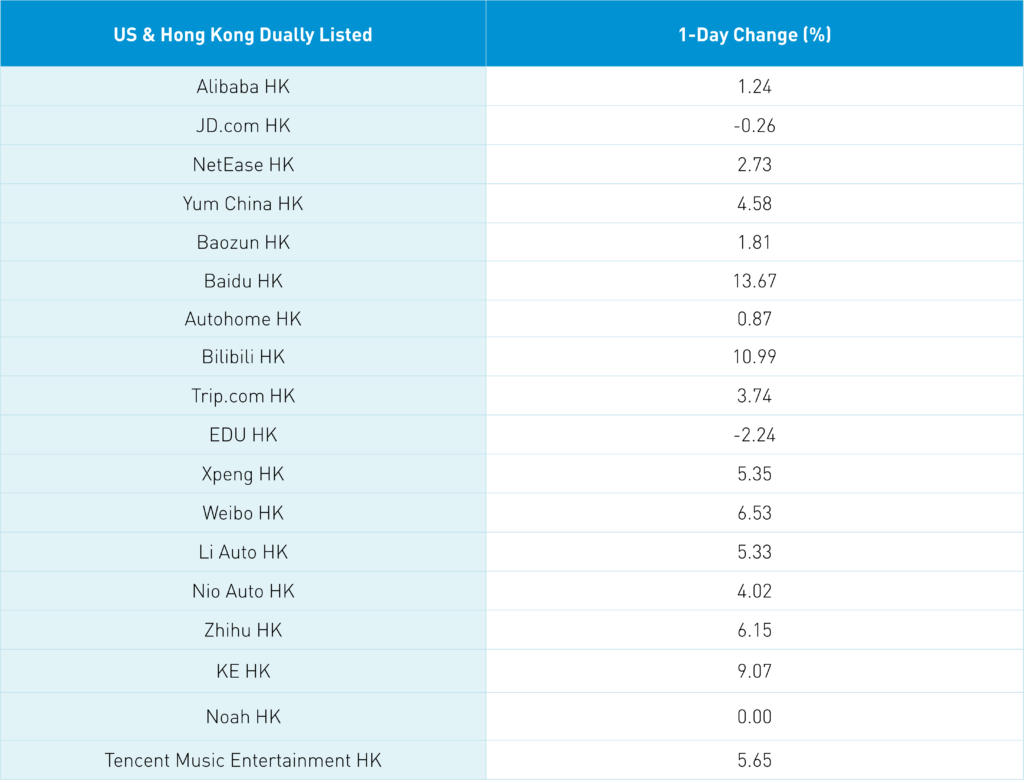

The lack of a live demonstration of Baidu’s “ERNIE” AI chat bot as it launched yesterday disappointed investors. However, overnight, Baidu allowed access to ERNIE, which led to positive reviews. Baidu’s Hong Kong share class gained +13.67% overnight, which lifted internet plays. Baidu was also approved for driverless/robotaxis in another section of Beijing.

The Hang Seng Tech gained +4.41%, led by Hong Kong’s most heavily traded stocks, which included Tencent, which gained +1.01%, Alibaba, which gained +1.24%, Meituan, which gained +3.25%, Baidu, which gained +13%, AIA, which gained +3.34%, and sports apparel maker Li Ning, which fell -9.91% on disappointing results. Mainland investors bought $286 million worth of Hong Kong stocks as Tencent was a large buy, the 2nd largest net buy day year-to-date.

Mainland China posted gains as investors cheered the news of reforms to state-owned enterprises (SOEs). SOEs will be pushed to reach global standards, which should lead investors to reconsider Ex-SOE strategies, in my opinion. Foreign investors bought a very healthy $1.042 billion worth of Mainland stocks today, which may have been driven by today’s index rebalance. Foreign direct investment in China rose +6.1% year-over-year in January and February, an inconvenient truth for US politicians. President Xi will visit Russia to advocate his Ukraine peace plan next week. Talk about a positive Black Swan!

The Wall Street Journal had a good article on distressed property developer Evergrande is “close to striking a debt restructuring deal with foreign bond investors”. We continue to advocate that investors look at developer bonds as many have left them for dead. We have long stated that the likely outcome would resemble the ECB’s strategy with Greece: extend the maturity of the bonds, cut the interest payments, and allow the company to muddle through. Online real estate company KE Holdings beat financial results yesterday with positive comments on the real estate market stabilizing.

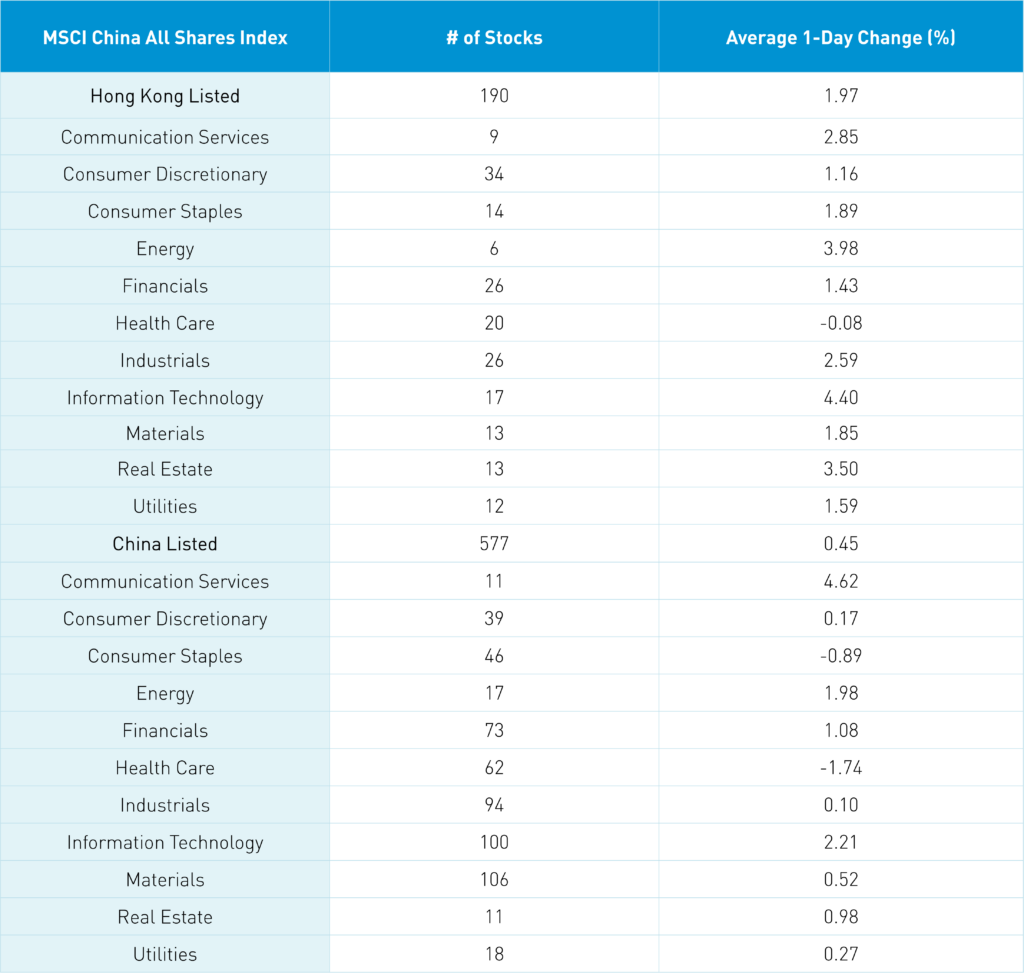

The Hang Seng and Hang Seng Tech indexes gained +1.64% and +4.41%, respectively, on volume that increased +48.11% from yesterday, which is 135% of the 1-year average. 430 stocks advanced while 77 declined. Main Board short sale turnover increased +58.79% from yesterday, which is 129% of the 1-year average, as 17% of turnover was short turnover. Value outperformed growth as small caps outpaced large caps. The top-performing sectors were technology, which gained +4.41%, energy, which gained +3.98%, and real estate, which gained +3.5%. Meanwhile, healthcare was the only negative sector, pulling an inverse James Bond by falling -0.07%. The top-performing subsectors were semiconductors, media, and household products, while no industry group sub-sectors were down. Southbound Stock Connect volumes moderate/light as Mainland investors bought $286 million worth of Hong Kong stocks as Tencent was a large net buy, while Meituan and Kuaishou were small net buys.

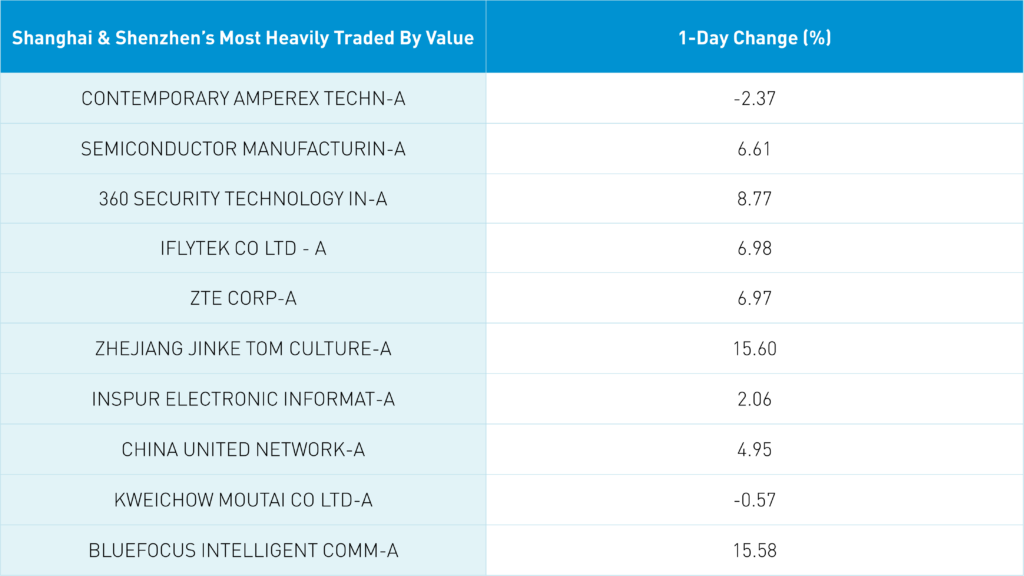

Shanghai, Shenzhen, and the STAR Board gained +0.73%, +0.52%, and +2.35%, respectively, on volume that increased +15% from yesterday, which is 108% of the 1-year average. 3,238 stocks advanced while 1,418 stocks declined. Value factors outperformed growth factors as small caps outpaced large caps. Thew top-performing sectors were communication services, which gained +4.64%, technology, which gained +2.22%, and energy, which gained +1.99%. Meanwhile, consumer staples and healthcare were off -0.87% and -1.73%, respectively. The top-performing subsectors were internet, software, and computer hardware. Meanwhile, motorcycles, healthcare, and pharmaceuticals were the worst performing subsectors. Northbound Stock Connect volumes were high as foreign investors bought $1.042 billion worth of Mainland stocks. CNY appreciated +0.12% versus the US dollar as the Asia Dollar Index posted a small gain versus the US dollar. Treasury bonds sold off while Shanghai copper and steel were both off.

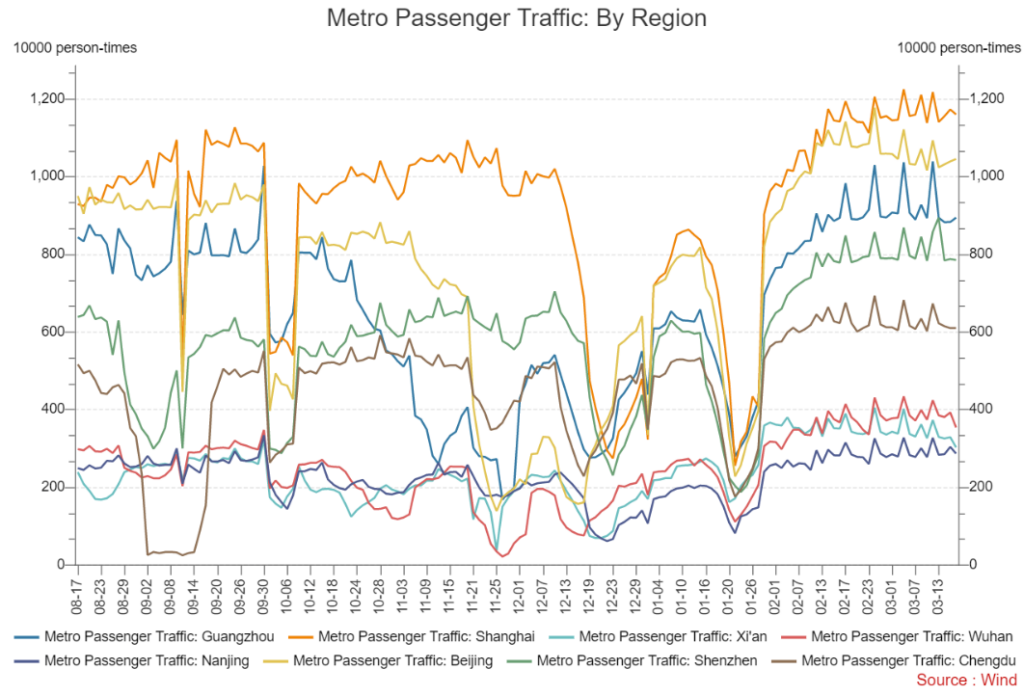

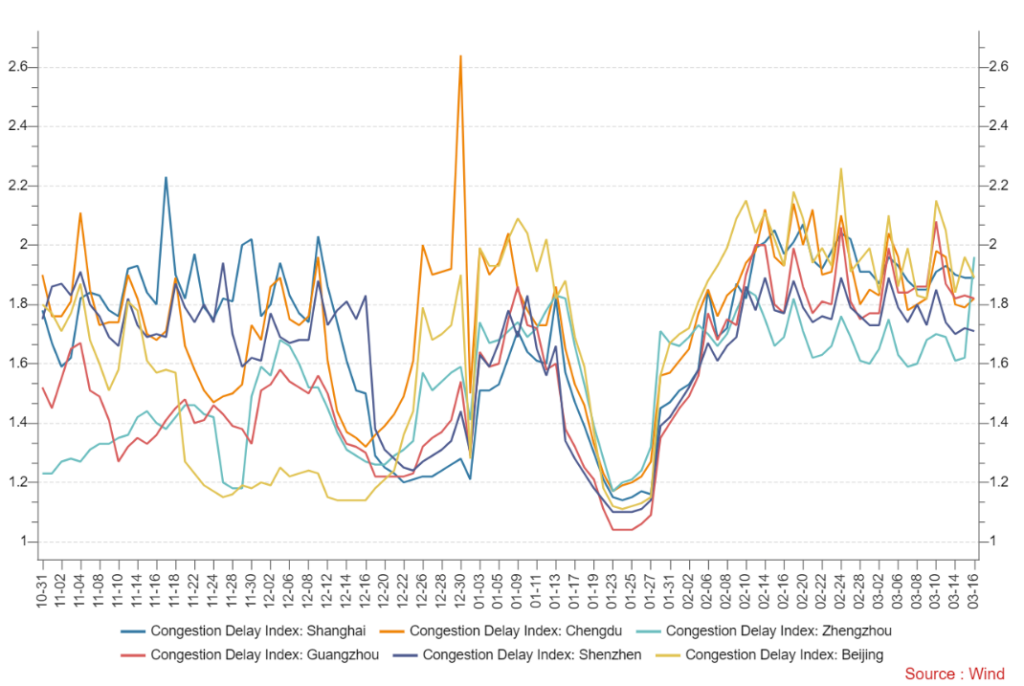

Major Chinese City Mobility Tracker

Last Night’s Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 6.88 versus 6.90 yesterday

- CNY per EUR 7.31 versus 7.32 yesterday

- Yield on 1-Day Government Bond 1.83% versus 1.78% yesterday

- Yield on 10-Year Government Bond 2.86% versus 2.86% yesterday

- Yield on 10-Year China Development Bond 3.02% versus 3.03% yesterday

- Copper Price -0.30%

- Steel Price -0.49%