PMIs Higher as Economic Rebound Gains Momentum, Week in Review

3 Min. Read Time

Week in Review

- Earlier in the week, global CEOs, including Apple's Tim Cook, were in attendance at the China Development Forum.

- On Tuesday, Alibaba announced it would become a holding company comprised of six business groups in order to “unlock shareholder value and foster market competitiveness."

- On Wednesday, BYD and Kuaishou released their financial results for the quarter, beating analyst expectations across the board.

- On Thursday, Premier Li gave a keynote speech at the Boao Forum, stating, “In the first two months of this year, the Chinese economy showed an encouraging momentum of rebound. The situation in March is even better than that in January and February.”

Friday's Key News

Asian equities ended the week and quarter positively as India outperformed while the Philippines -2.18%. I’ll contact my main man in Manila, Brian, to find out what happened. In your mind, you’d think global stocks were crushed, but Asia, the US, and especially Europe (double-digit gains) had a shockingly strong 1st quarter. Yes, I’m knocking on wood, as there is no reward/upside performance without risk. Like many investors, the scary headlines and lack of confidence in the Fed are the main contributors. Personally, I’ve added to cash/money market funds markets which yield nearly 5%, so of course, stocks went up! The key is to look at the data and don’t act emotionally!

At the market’s open, we had the “official” PMIs released as Manufacturing PMI was 51.9 versus expectations of 51.6 and February’s 52.6, and Non-Manufacturing was 58.2 versus expectations of 55 and February’s 56.3. Remember PMIs track month-over-month changes, not year-over-year. The growth rate in manufacturing, geared to the global economy, slowed while domestic China's growth increased. Manufacturing new export orders slowed month over month from 52.4 to 50, while non-Manufacturing new export orders declined into contraction mode from 51.9 to 48.1. Business expectations in both surveys are very high, with Manufacturing expectations 55.5 and Non-Manufacturing 63.3! Remember what Premier Li stated yesterday that things are picking? I would anticipate month over month; this positive momentum will increase.

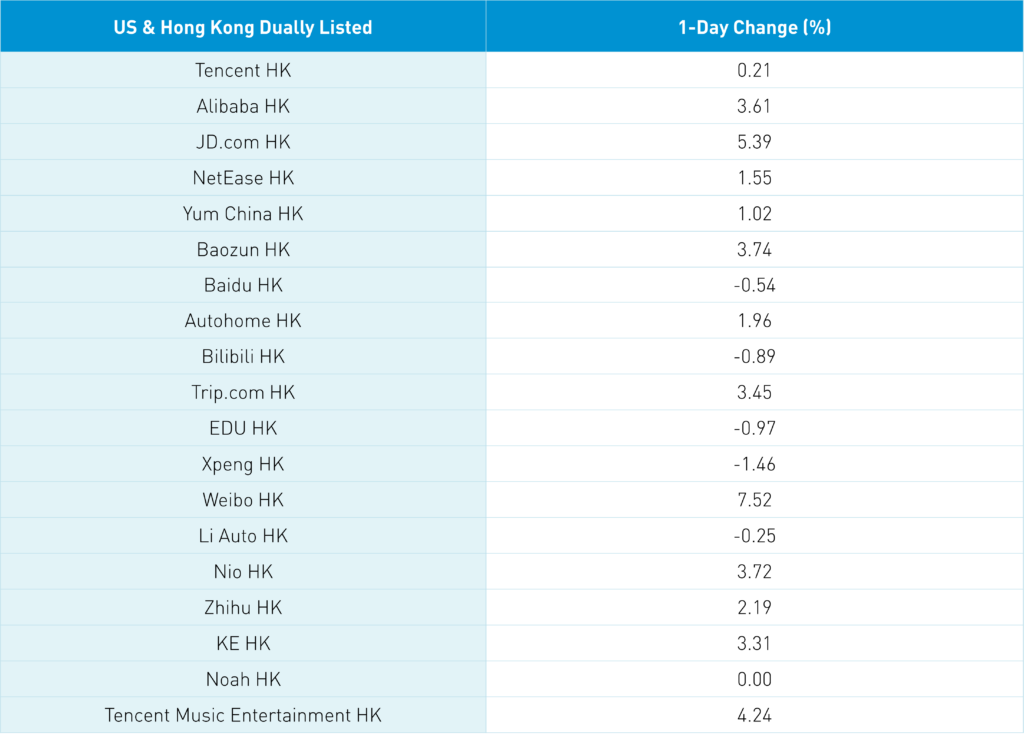

Hong Kong’s most heavily traded by value were Tencent +0.21%, Alibaba HK +3.61%, Meituan +1.06%, JD.com HK +5.39%, and BYD +2.04%. Investors cheered the corporate restructuring moves from Alibaba and JD.com, which are very shareholder friendly, in my opinion. Is Tencent next? Breaking out gaming and WeChat/social media would be interesting. Important to point out that these new IPOs will happen in Hong Kong and not the US, which is too bad.

Mainland China posted small gains as the Boao Forum garnered significant attention with President Xi meeting the Spanish, Malaysian, and Singaporean Prime Ministers. We also had Premier Li’s speech applauded regionally, though there was no attention here in the US. UN Secretary-General Ban Ki-moon stated, “Emerging and developing Asia remains the best hope and chief driver of global growth. Combined, they would contribute 75 percent of global growth.” Wow! Are you allocated appropriately?

Quiet night overnight, with Mainland markets posting small gains. Slow and steady as onshore China now has half the volatility of offshore China.

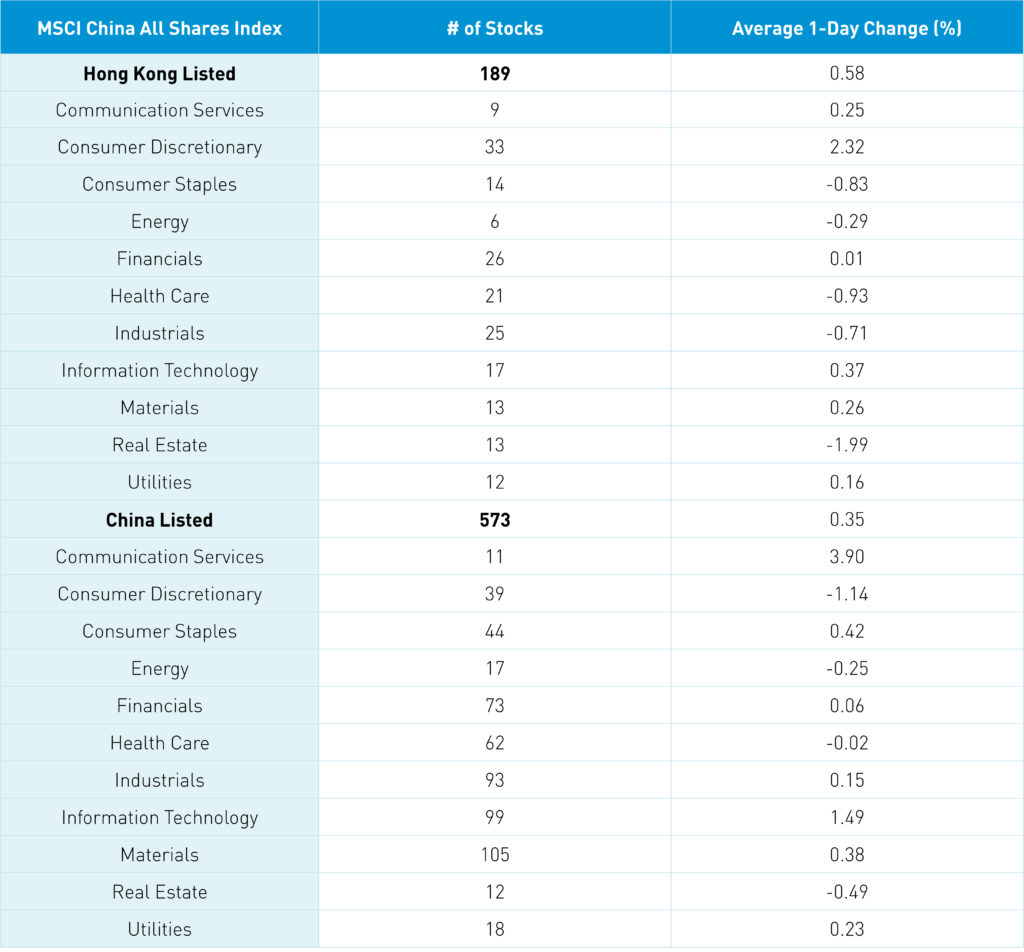

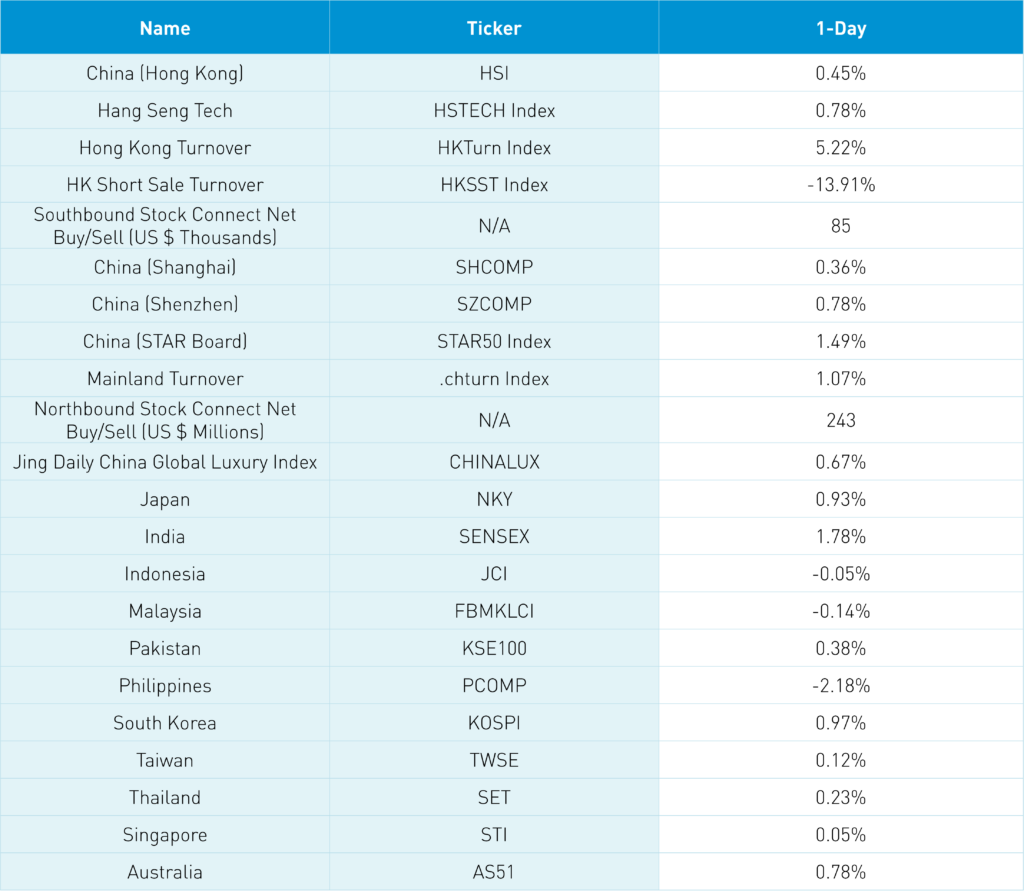

The Hang Seng and Hang Seng Tech gained +0.45% and +0.78% on volume +5.22% from yesterday, 116% of the 1-year average. 244 stocks advanced, while 251 stocks declined. Value and growth factors were mixed as large caps outpaced small caps. Main Board short turnover declined -13.91% from yesterday, 87% of the 1-year average, as 13% of the 1-year average was short turnover. The top sectors were discretionary +2.32%, tech +0.37%, and materials +0.26%, while real estate -1.99%, healthcare -0.93%, and staples -0.83%. The top sub-sectors were food/staples, retailing, and telecom, while transportation, pharmaceuticals, and household products were the worst performers. Southbound Stock Connect volumes were light/moderate as Mainland investors bought $85mm of Hong Kong stocks, with Tencent a large buy, Kuaishou a small buy, and Meituan a small sell.

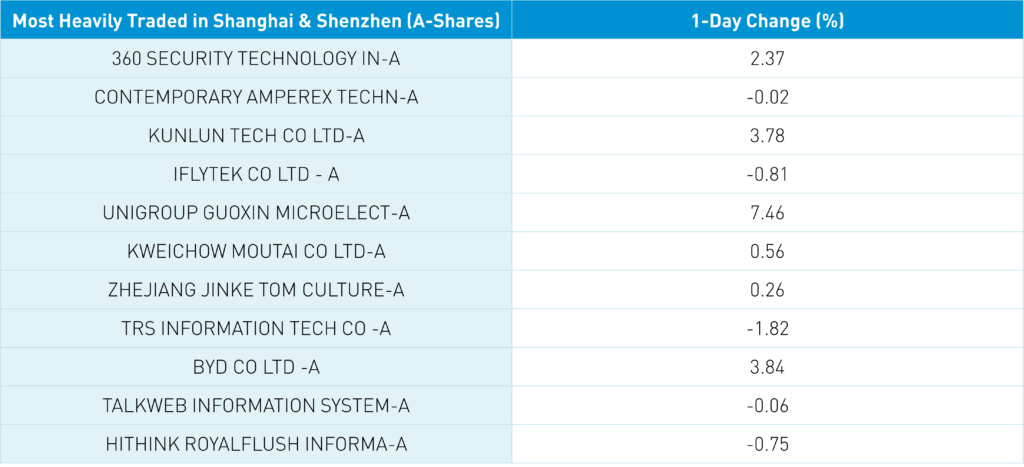

Shanghai, Shenzhen, and STAR Board gained +0.36%, +0.78%, and +1.49% on turnover +1.07% from yesterday, 106% of the 1-year average. 3,241 stocks advanced, while 1,385 stocks declined. Value and growth sectors were mixed, while small caps outpaced large caps. The top sectors were communication +3.9%, tech +1.5%, and staples +0.43%, while discretionary -1.13%, real estate -0.48%, and energy -0.24%. The top sub-sectors were internet, software, and cultural media, while household products, restaurants, and shipping were the worst performers. Northbound Stock Connect volumes were moderate/high as foreign investors bought +$243mm, with Foxconn a small net sell and Kweichow Moutai a small net buy. CNY and the Asia dollar index fell small versus the US dollar. Treasury bonds rallied while Shanghai copper fell and steel gained.

Major Chinese City Mobility Tracker

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 6.88 versus 6.88 yesterday

- CNY per EUR 7.48 versus 7.48 yesterday

- Asia Dollar Index +0.19% overnight

- Yield on 10-Year Government Bond 2.85% versus 2.86% yesterday

- Yield on 10-Year China Development Bank Bond 3.03% versus 3.04% yesterday

- Copper Price -0.37% overnight

- Steel Price +0.58% overnight