Foreign Freak-out as Mainland Buys Hong Kong, Tencent Results Review

3 Min. Read Time

After the Hong Kong close, Tencent (700 HK, TCEHY US) reported Q1 financial results as revenue beat analyst expectations though adjusted net income and adjusted EPS missed. There were plenty of positives including revenue, net income, and EPS were strong year-over-year gains, international/non-China game revenue shined/+25% to RMB 13.2 billion, advertising revenue improved, and margins and cash flows were strong. Chairman and CEO Ma Huateng noted a “domestic consumption recovery” which drove the pick up in advertising and mobile payments. Quarterly revenue was the highest for the company ever. In the management call, Tencent noted President Xi’s April meeting and speech supportive of Chinese internet companies as evidenced by Tencent’s regular game approvals.

Revenue grew 11% to RMB 149.986 billion ($21.8 billion) from RMB 135.471 billion versus analyst expectations of RMB 146.286 billion

VAS (games) Revenue grew +9% to RMB 79.3 billion led by international games +23% to RMB 13.2 billion and domestic games by +6% to RMB 35.1 billion

Online advertising revenue grew +17% to RMB 21 billion

FinTech/Business Services grew +14% to RMB 48.7 billion

Adjusted Net Income grew +27% to RMB 32.538 billion from RMB 25.545 billion versus analyst expectations of RMB 33.22 billion

Adjusted EPS grew +28% to RMB 3.35 from RMB 2.62 versus analyst expectations of RMB 3.44

Key News

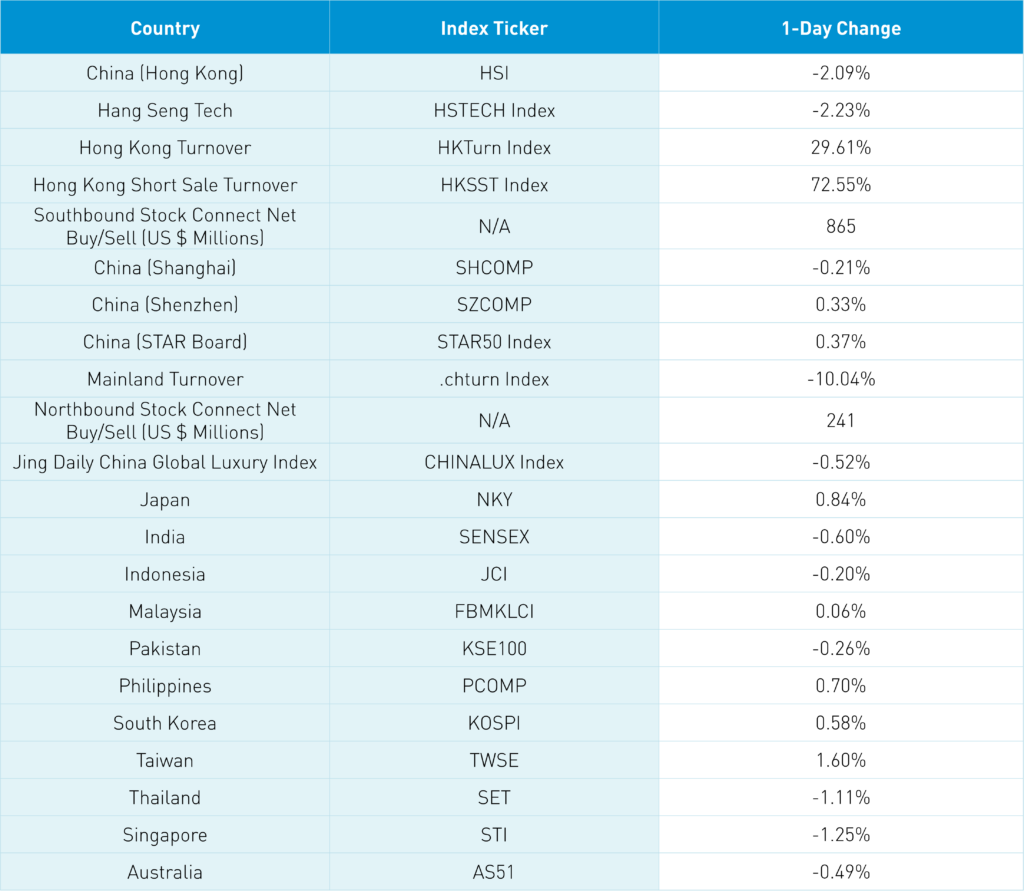

Asian equities were mixed as Taiwan outperformed while Hong Kong, Singapore, and Thailand underperformed. The US debt ceiling is a factor as investors ponder if the two sides can come to an agreement leading to risk-off, conservative positioning on light volumes as buyers wait to see how things pan out. While Mainland China had a mixed day, Hong Kong sold off following the National Development and Reform Commission’s (NDRC) mid-morning statement that everything in China’s economy is improving. The release appears tone-deaf to yesterday’s underwhelming April economic release which had raised hopes policymakers would respond with economic support. The NDRC statement dashed those hopes sending stocks down as potential buyers of stimulus news receded while shorts pressed their bets.

Hong Kong Main Board's short turnover accounted for 20% of the total turnover as only 48 stocks advanced while 453 declined. CNY sold off versus the US dollar to 6.99 with the Asia dollar index off as well. Not helping was tepid April property sales as real estate in Hong Kong was off -4.26% though off only -0.97% in the Mainland. High dividend-paying stocks were hit with profit-taking exacerbating today’s move. After the market close, the PBOC released a statement speaking to China’s low inflation though mentioned the economy is improving incrementally and policy tools are available. This should give investors confidence policymakers are aware of the situation and ready to act.

While macro concerns are center stage, microanalysis/bottom-up is improving as evidenced by JD.com, Baidu, and now Tencent’s Q1 financial results. Remember Alibaba reports tomorrow morning. We had another “foreign investor freakout” driven by low positioning to China due to geopolitical concerns which allowed shorts to drive stocks down in the absence of foreign buyers though Mainland Chinese investors bought a very healthy $865 million of Hong Kong stocks today. Mainland China took the same news and yawned in a mixed day on light volumes. Amazing to see the disparity between onshore China and the vast majority of owners, Chinese investors versus offshore China and HK-US ADRs, the majority owned by foreign investors. Foreign investors did buy $241 million of Mainland stocks today.

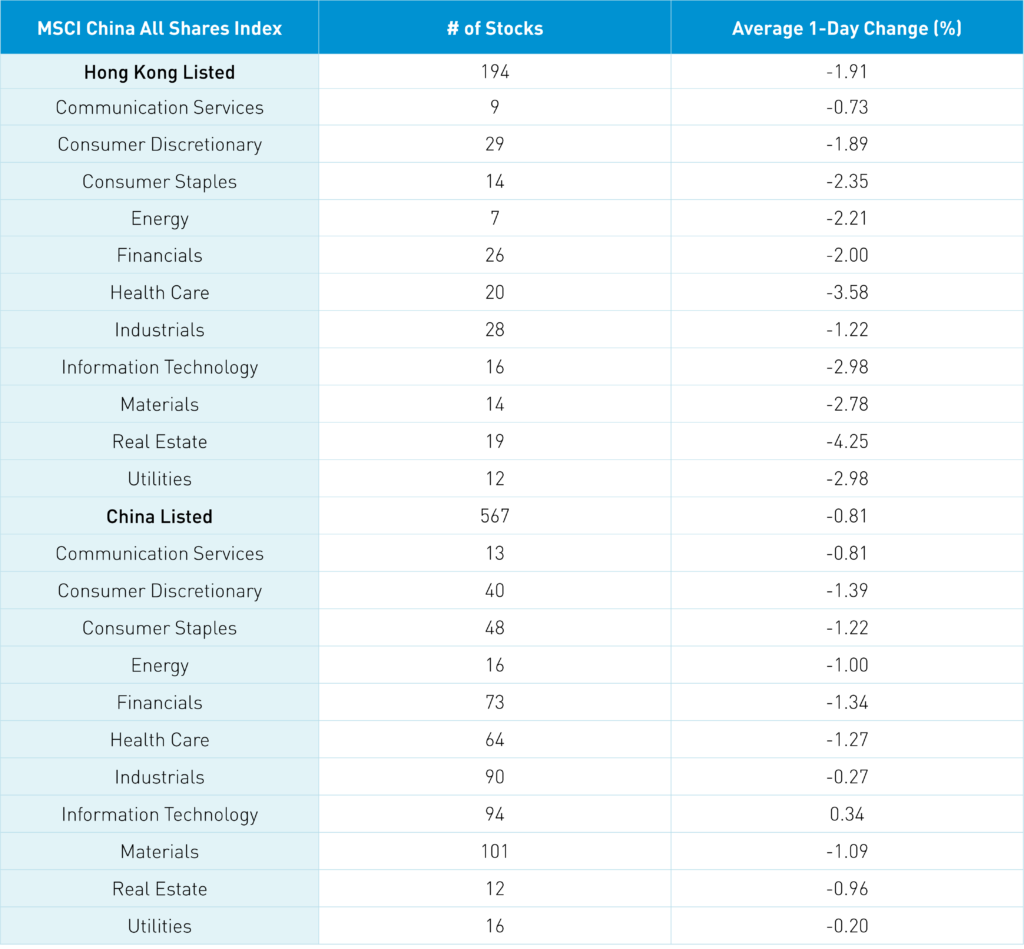

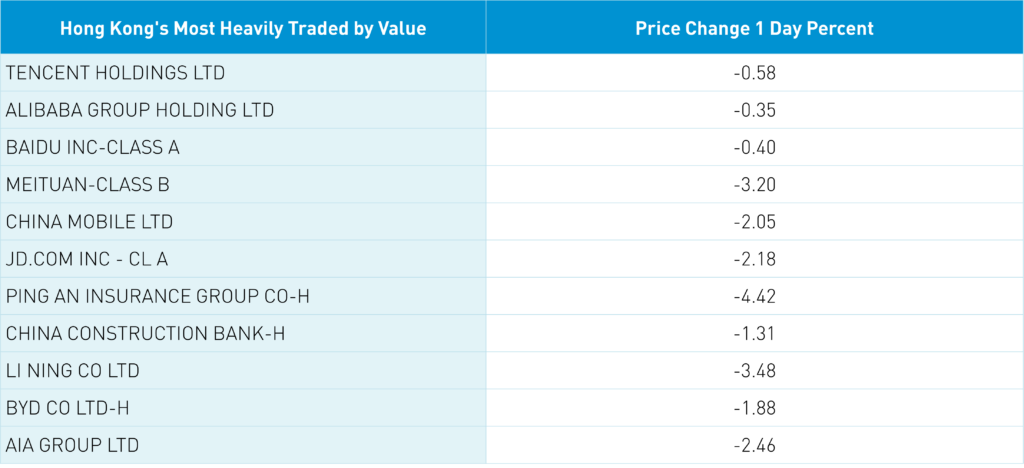

The Hang Seng and Hang Seng Tech were off -2.09% and -2.23% on volume +29.61% from yesterday which is 85% of the 1-year average. 48 stocks advanced while 453 declined. Main Board short selling increased +72.75% from yesterday which is 103% of the 1-year average as 20% of turnover was short turnover. Value factors outpaced growth factors as large caps “outperformed” small caps. All sectors were negative with real estate -4.24%, health care -3.57%, and utilities -2.97%. Household products were the only positive sub-sector while food, pharma, and consumer durables were the worst. Southbound Stock Connect volumes were light as Mainland investors bought $865 million of Hong Kong stocks with Tencent a moderate net buy, Kuiashou a small net buy, and Meituan a very small net sell.

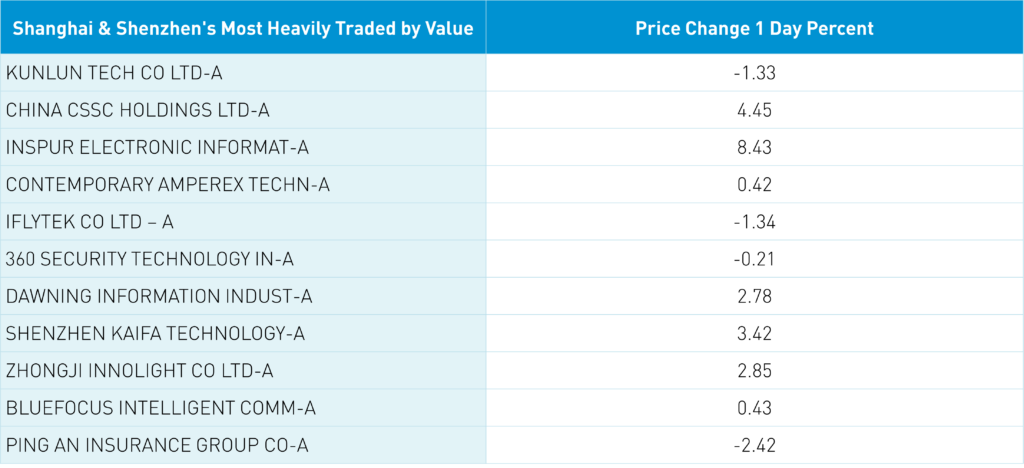

Shanghai, Shenzhen, and STAR Board were mixed -0.21%, +0.33%, and +0.37% on volume -10.04% from yesterday which is 84% of the 1-year average. 3,128 stocks advanced while 1,527 stocks declined. Growth factors outperformed value factors as small caps outpaced large caps. Tech was the only positive sector +0.33% while discretionary -1.4%, financials -1.36%, and healthcare -1.29%. The top sub-sectors were aerospace/military, computer hardware, and internet while telecom, insurance, and precious metals were the worst. Northbound Stock Connect volumes were moderate/light as foreign investors bought $241 million of Mainland stocks with Kweichow Moutai a small net sell, Ping An a very small net buy, and Foxconn a very small net sell. CNY fell -0.25% to 6.99 versus the US dollar along with the Asia dollar index. Treasury bonds sold off along with copper while steel gained.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 6.99 versus 6.96 yesterday

- CNY per EUR 7.57 versus 7.59 yesterday

- Asia Dollar Index -0.20% overnight

- Yield on 10-Year Government Bond 2.72% versus 2.71% yesterday

- Yield on 10-Year China Development Bank Bond 2.89% versus 2.88% yesterday

- Copper Price -0.71% overnight

- Steel Price +0.38% overnight