It’s Always Darkest Before The Dawn On Geopolitical Green Shoots, Week in Review

3 Min. Read Time

Week in Review

- Asian equities were mixed but rangebound for the week as Hong Kong and Japan were slightly higher and Mainland China was slightly lower.

- It was a busy week for internet earnings as Baidu, Tencent, and Alibaba all beat estimates on Q1 revenue.

- China’s April economic release came in below sky-high estimates though retail sales increased by over +18% year-over-year.

- There were a couple of “green shoots” on the geopolitical front this week as China’s diplomatic team met with Ukrainian leaders in Kyiv and Biden indicated that he will speak with Xi at some point after tackling the debt ceiling, that is.

Friday’s Key News

Asian equities ended a mixed week largely higher though Hong Kong was off following yesterday’s sell-off in US-listed China stocks.

Following strong results and guidance from JD.com, Baidu, and Tencent, expectations likely rose for Alibaba, which increased revenue by +2% year-over-year in Q1 with strong upticks in adjusted net income and EPS. Due to the company’s Hong Kong listing, it cannot officially provide forward guidance, though some cited a conservative/tepid outlook as a culprit for the stock’s underperformance while giving away the cloud business to shareholders struck some as surprising. Like sell-side analysts’ reports coming out post-earnings, I felt Alibaba’s moves to unlock shareholder value should be cheered. Maybe paying dividends would motivate investors rather than buying back stock. The move would also stick it to short sellers, who would be forced to pay the dividend.

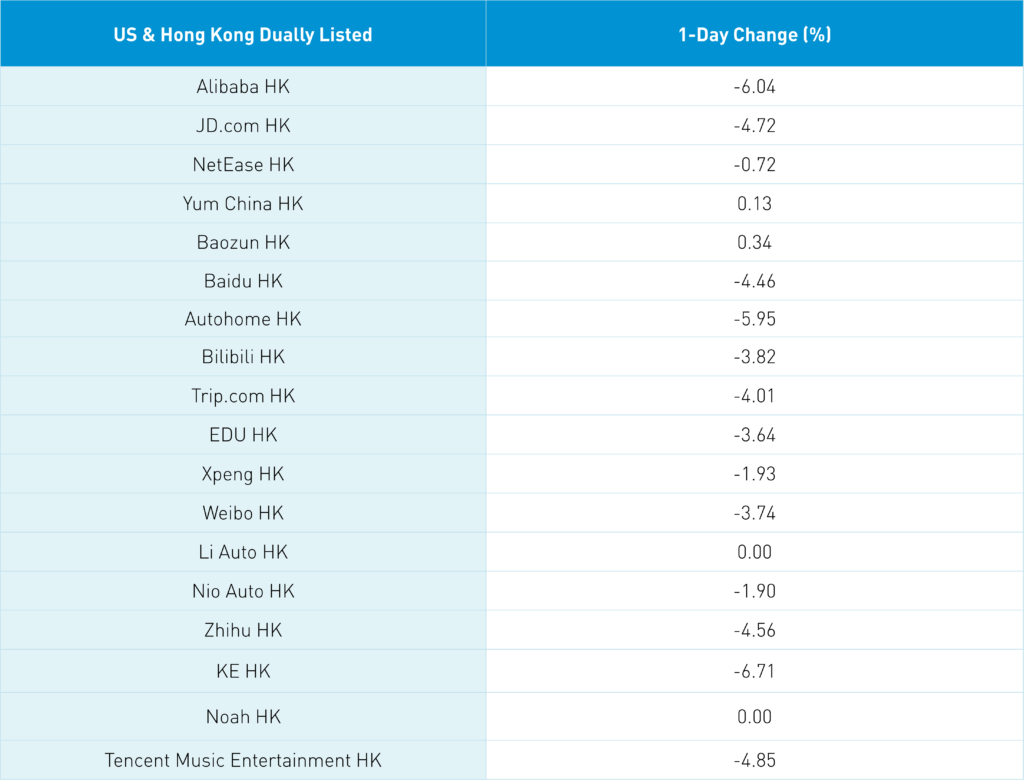

Hong Kong’s most heavily traded stocks overnight were Alibaba, which fell -6.04%, Tencent, which fell -1.24%, Meituan, which fell -3.67%, JD.com, which fell -4.72%, and China Construction Bank, which fell -1.11%. Financials were led lower by brokers on talk that institutional commissions will be lowered by the regulator. It is worth noting that Hong Kong volumes were light overall, which exacerbated moves as one local broker noted the lack of buying or selling. Buyers need catalysts.

China’s tepid/incremental economic recovery was noted by Premier Li Qiang while visiting Shandong Province last night. He spoke of “efforts to boost the real economy, expand domestic consumption, and stabilize external demand to promote economic recovery.” He also had some positive comments on electric vehicles. This is all good talk, though actions are needed, especially because the central bank cannot lower rates until mid-June.

Another factor in last night’s price action was concern over geopolitical issues. This has likely also sidelined buyers as a US outbound technology investment ban is likely to be announced at the G-7. The consensus is that the focus will be on private investments, which could relieve some concerns in public markets. Perhaps this will be the final guardrail needed to resume normal relations.

The first high-level meeting between the US and China will occur next week after FIVE years! China’s Commerce Minister Wang Wentao will travel to Washington DC to meet with Commerce Secretary Gina Raimondo and US Trade Representative Katherine Tai. Mainland China was mixed with growth stocks/sectors gaining on light volumes while foreign investors were small net sellers of Mainland stocks. CNY and the Asia dollar index did bounce versus the US dollar.

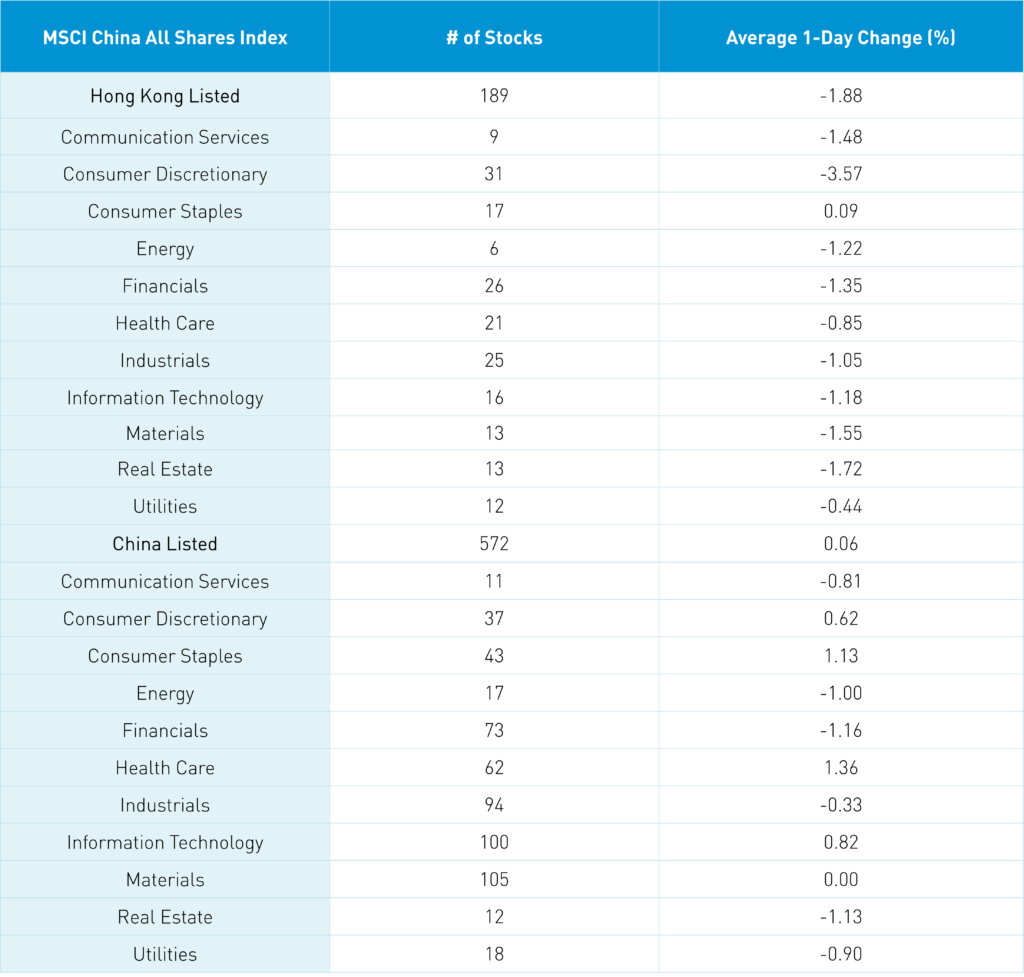

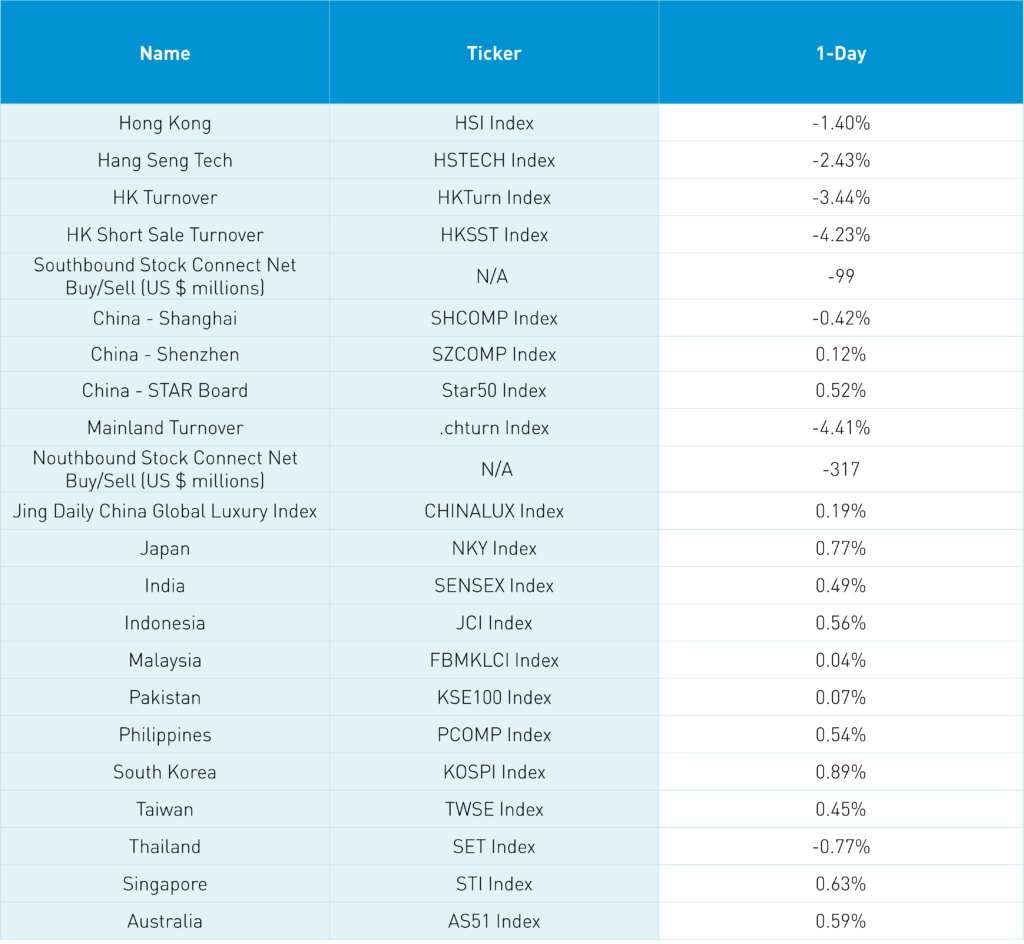

The Hang Seng and Hang Seng Tech indexes fell -1.4% and -2.43%, respectively, on volume that decreased -3.44% from yesterday, which is 80% of the 1-year average. 116 stocks advanced while 369 stocks declined. Main Board short turnover declined -4.09% from yesterday, which is 83% of the 1-year average as 17% of turnover was short turnover. Value factors outperformed growth factors as small caps “outperformed”/fell less than large caps. Consumer Staples was the only positive sector, gaining +0.09%, while Consumer Discretionary fell -3.56%, Real Estate fell -1.71%, and Materials fell -1.54%. The top-performing subsectors were telecom and food while retailers, media, and semiconductors were among the worst. Southbound Stock Connect volumes were light as Mainland investors sold -$99 million of Hong Kong stocks as Kuiashou was a small net sell, and Tencent and Meituan were moderate net sells.

Shanghai, Shenzhen, and STAR Board diverged to close -0.42%, +0.12%, and +0.52%, respectively, on volume that decreased -4.41% from yesterday, which is 91% of the 1-year average. 2,251 stocks advanced while 2,423 stocks declined. The Growth factor outperformed the value factor while small caps outpaced large caps. The top-performing sectors were Healthcare, which gained+1.32%, Consumer Staples, which gained +1.09%, and Information Technology, which gained +0.77%. Meanwhile, Financials fell -1.2%, Real Estate fell -1.17%, and Energy fell -1.05%. The top-performing subsectors were household appliances, pharmaceuticals, and semiconductors, while education, cultural media, and diversified financials were among the worst. Northbound Stock Connect volumes were moderate/light as foreign investors sold -$317 million of Mainland stocks as Longi was a moderate/small net sell, Kweichou Moutai and China Tourism Duty-Free were small net sells. CNY and the Asia Dollar Index gained +0.39% and +0.33%, respectively, versus the US dollar. Treasury bonds rallied while copper and steel were off.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.01 versus 7.04 yesterday

- CNY per EUR 7.58 versus 7.58 yesterday

- Yield on 1-Day Government Bond 1.46% versus 1.49% yesterday

- Yield on 10-Year Government Bond 2.72% versus 2.72% yesterday

- Yield on 10-Year China Development Bank Bond 2.88% versus 2.88% yesterday

- Copper Price -0.37% overnight

- Steel Price -1.08% overnight