US-China Relations To Improve “Very Shortly”, Examining the Micron “Ban”, Full Truck & Kuaishou Beat

3 Min. Read Time

Key News

Asian equities had a strong start to the week as Hong Kong outperformed the region.

Investors focused on the G-7 communique on “de-risking, rather than decoupling” and President Biden’s comments that US-China relations will improve “very shortly”. An improvement in relations would remove the last impediment weighing on offshore China stocks as many investors continue to sit on the sidelines due to the fraught US-China political relationship and the volatility it creates.

China’s Minister of Commerce Wang Wentao will visit US Commerce Secretary Gina Raimondo in Washington DC this week. Mainland media noted that Wang met with representatives from US companies operating in China at a Shanghai meeting today to discuss and receive feedback on “optimizing the business environment”. US companies participating included 3M, Dow, Merck, Honeywell, and Johnson & Johnson.

Micron’s chips have not been completely banned in China due to the security review, though sales to telecommunication and government agencies will likely be stopped. The “ban” is unlikely to include manufacturers operating and assembling goods in China. The Micron move is likely negotiating 101 in advance of the US and China Commerce heads meeting, though Micron’s loss would be a gain for South Korean semiconductor manufacturers, which gained overnight.

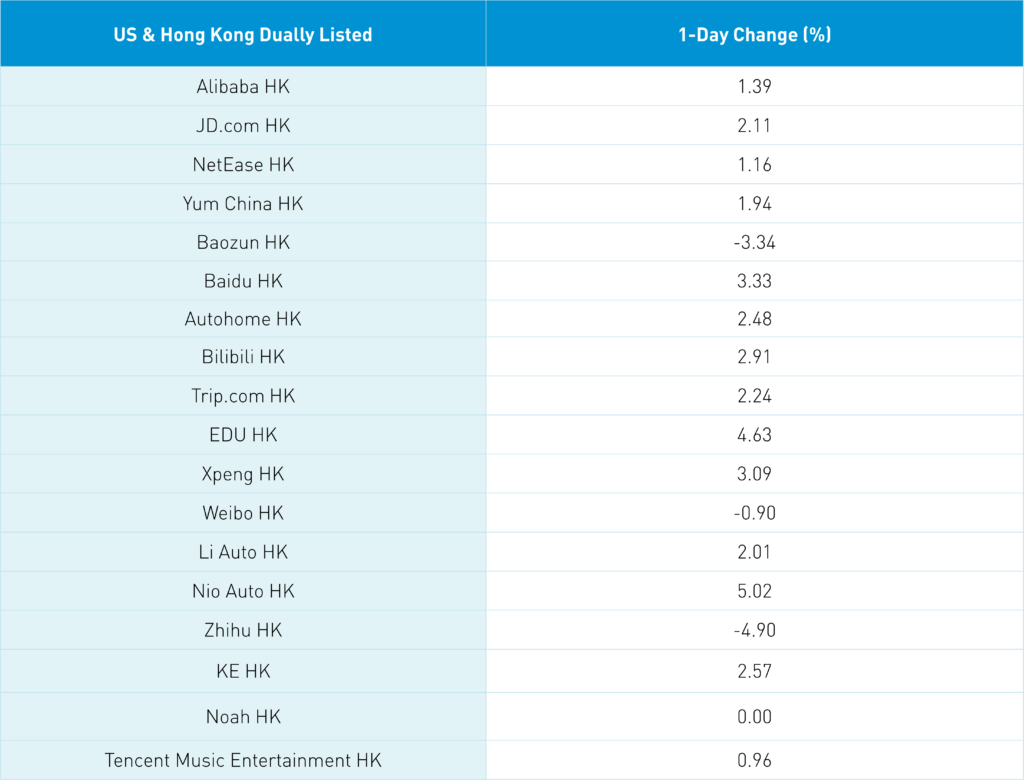

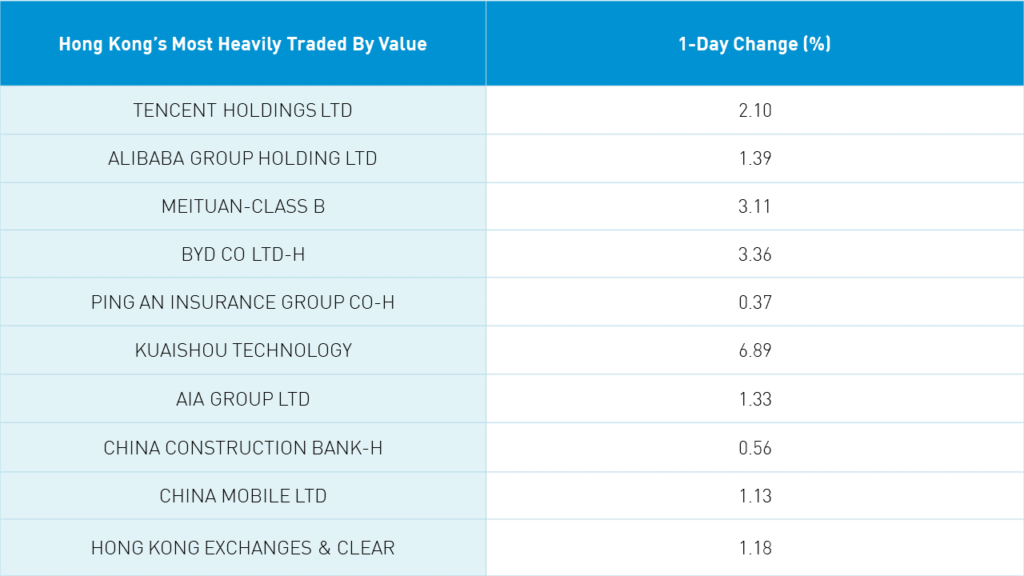

Hong Kong rallied, though volume was light, led by the most heavily traded stocks by value Tencent, which gained +2.1%, Alibaba, which gained +1.39%, Meituan, which gained +3.11%, BYD, which gained +3.36%, and Ping An Insurance, which gained +0.37%.

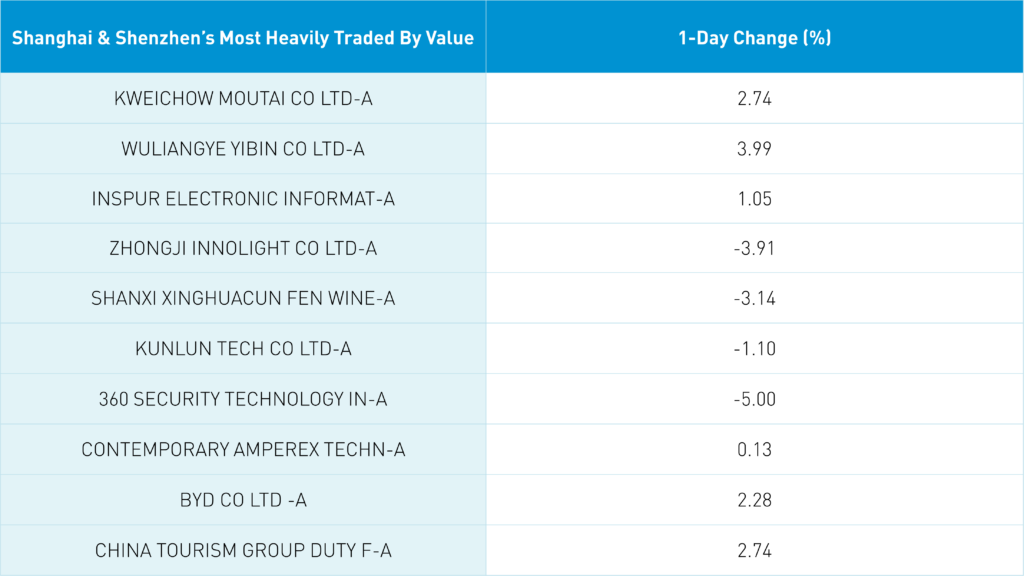

Tencent announced it bought back 1 million shares after the close in Hong Kong. Kuaishou gained +6.89% in advance of Q1 2023 financial results, which were announced after the close. The company beat on the big three: revenue, adjusted net income, and adjusted EPS, as the company swung to profitability. US-listed Full Truck Alliance (YMM) reported earnings before the US market open beating on the big three as well. Liquor stocks had a good day in mainland China as Shanghai and Shenzhen both gained +0.39% while foreign investors bought $578 million worth of Mainland stocks.

The nattering nabobs of negativity are focused on the G-7’s language on addressing China’s “economic coercion”. I find that interesting as the US’ GDP per Capita is $70,249, the UK’s is $46,000, Japan’s is $39,000, France’s is $43,000, the EU’s is $38,000, etc., while China’s is only $13,000! Click here to view the G-7 communique.

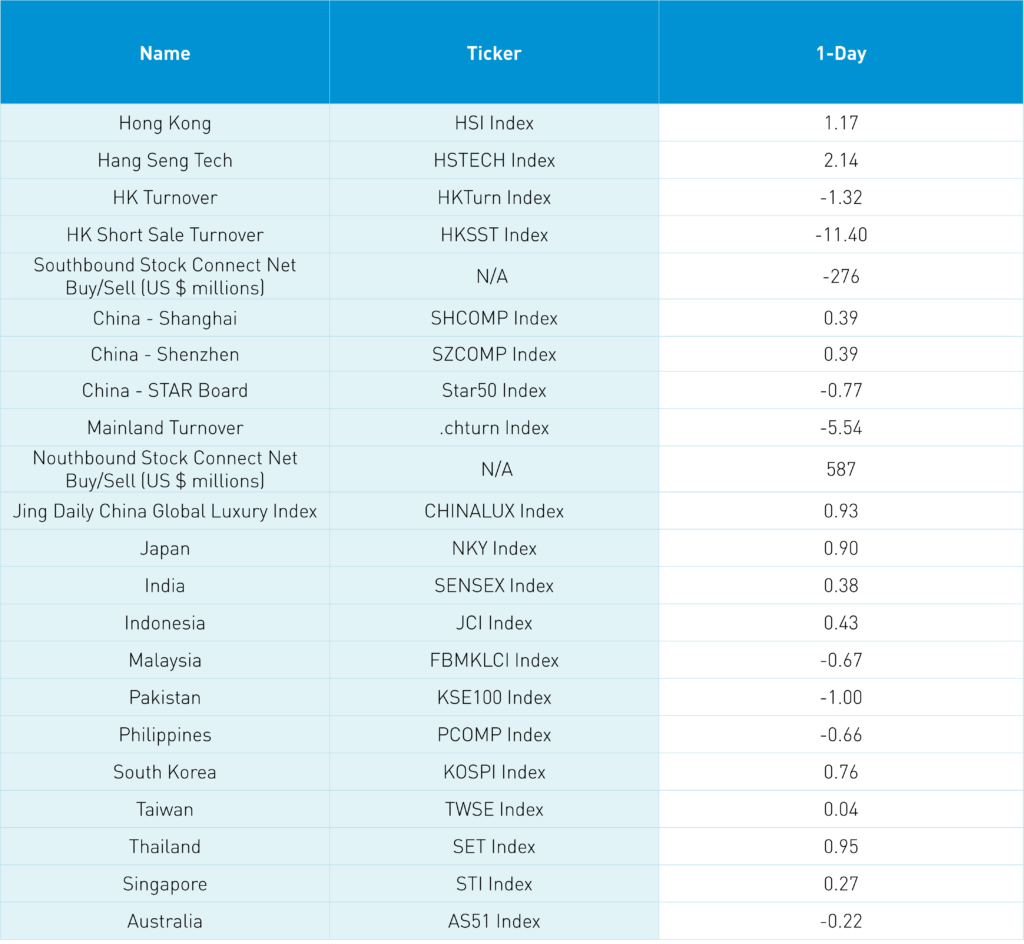

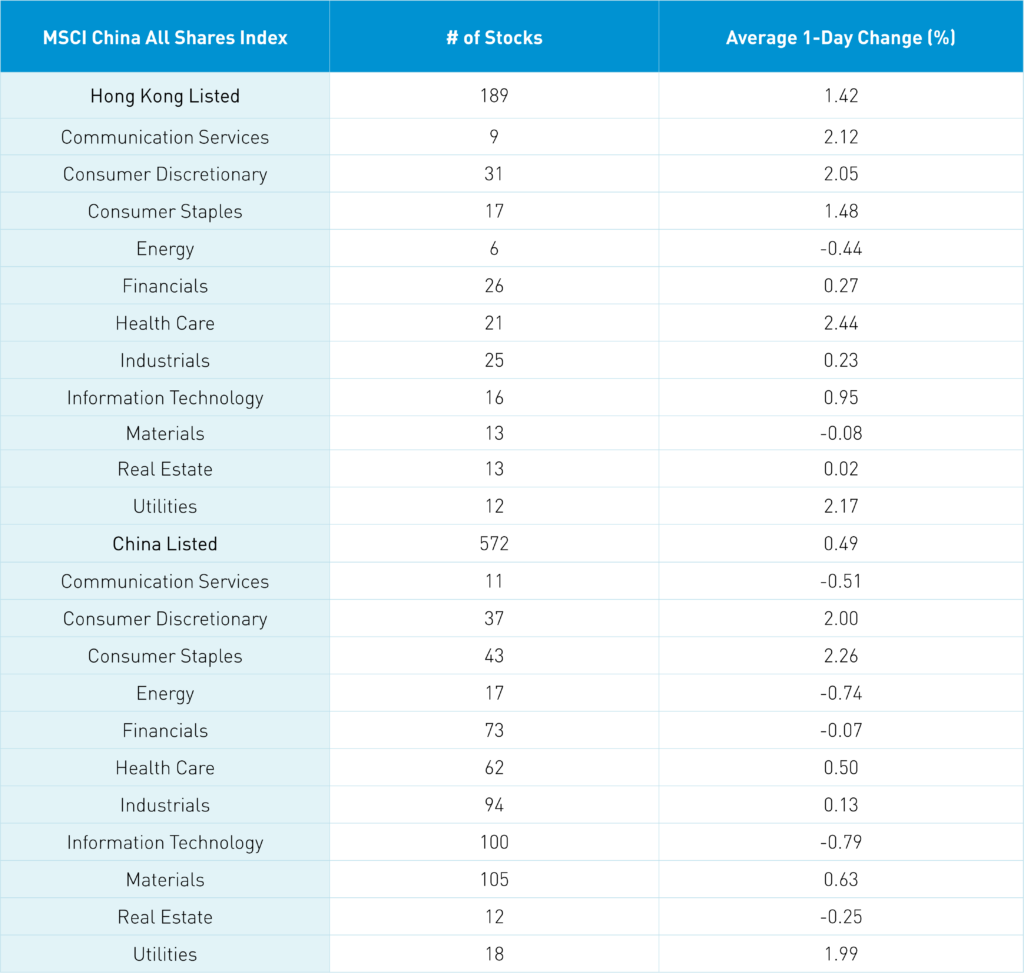

The Hang Seng and Hang Seng Tech indexes gained +1.17% and +2.14%, respectively, on volume that decreased -1.32% from Friday, which is 79% of the 1-year average. 305 stocks advanced while 174 stocks declined. Main Board short turnover fell -11.5% from Friday, which is 74% of the 1-year average as 16% of Main Board turnover was short turnover. Growth factors outperformed value factors as small caps outpaced large caps. The top-performing sectors were healthcare, which gained +2.45%, utilities, which gained +2.17%, and communication services, which gained +2.12%, while energy and materials were off -0.44% and -0.08%, respectively. The top-performing subsectors were autos, software, and pharmaceuticals, while materials, business services, and energy were among the worst performers. Southbound Stock Connect volumes were light as foreign investors sold -$276 million worth of Hong Kong stocks, though Tencent, Meituan, and Kuaishou were all net buys.

Shanghai, Shenzhen, and the STAR Board diverged to close +0.39%, +0.39%, and -0.77%, respectively, on volume that decreased -5.54% from Friday, which is 74% of the 1-year average. 2,566 stocks advanced while 2,060 stocks declined. Growth factors outperformed value factors as large caps outpaced small caps. The top-performing sectors were consumer staples, which gained +2.26%, consumer discretionary, which gained +2.00%, and utilities, which gained +1.98%. Meanwhile, technology fell -0.8%, energy fell -0.74%, and communication services fell -0.52%. The top-performing subsectors were chemical industry, liquor, and restaurants. Meanwhile, education, internet, and communication equipment were among the worst. Northbound Stock Connect volumes were light as foreign investors bought $578 million worth of Mainland stocks overnight as Kweichow Moutai was a strong net buy, Shanxi Fen Wine was a small net sell, and China Tourism Duty Free was a small net buy. CNY and the Asia Dollar Index were down versus the US dollar as Treasury bonds rallied. Copper and steel were both off.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.03 versus 7.01 Friday

- CNY per EUR 7.60 versus 7.58 Friday

- Yield on 1-Day Government Bond 1.43% versus 1.46% Friday

- Yield on 10-Year Government Bond 2.71% versus 2.72% Friday

- Yield on 10-Year China Development Bank Bond 2.88% versus 2.88% Friday

- Copper Price -0.11% overnight

- Steel Price -1.26% overnight