August Economic Data Improves & Lifts Hong Kong Stocks, Week in Review

4 Min. Read Time

Week in Review

- Alibaba’s leadership reshuffle went into effect on Monday as Joe Tsai became Executive Charman and Eddie Wu became CEO while it was announced that former CEO Daniel Zhang would run the company’s new technology fund instead of the cloud division.

- It was a positive and busy week for August China economic releases as the country reported a return to slight inflation from a short stint of slight deflation, retail sales and industrial production both beat estimates, and credit data indicated an expansion of lending.

- Shenzhen became the latest Chinese city to allow trials of autonomous vehicles and robo-taxis.

- China’s central bank cut banks reserve requirement ratio (RRR) by 0.25%, in the latest easing move to support the economy.

Key News

Asian equities ended a positive week higher on strong volume driven by FTSE Russell's index rebalance today, except for Mainland China, which pared morning gains to close lower.

The Mainland’s move lower was despite yesterday’s lowering of banks’ reserve requirement ratio (RRR) from 10.75% to 10.50%, which will allow more lending. Today, we also saw the People’s Bank of China (PBOC) injecting liquidity into the financial system and China released better-than-expected economic data for August.

YoY = Year-over-Year

Within retail sales, restaurant spending increased +12.4%, indicating spending habits are picking up. Year to date, online retail sales have increased +12.1% YoY as 26.4% of total retail sales of consumer goods took place online. August’s housing data was unsurprisingly mixed as reforms are just kicking in as property investment fell -8.8% year-over-year and home prices fell -0.29% month-over-month.

In addition to the successful IPO of Arm lifting sentiment, there were several positive catalysts overnight, especially for internet and technology. We had positive chatter on ticket sales going into China’s weeklong National Holiday, rumors that Alibaba is looking at investing in a South Korean E-Commerce company, and Meituan’s promotions going into the holiday.

Travel plays such as Macau gaming stocks, hotels, and travel agencies all gained overnight. Meanwhile, foreign investors were net sellers of large and mega caps and growth names, which weighed on the Mainland benchmarks. We are starting to see “green shoots” economically, which, with continued policy support, should allow for incremental growth to tick higher. Do you think global investors are positioned for an improvement? Neither do I.

I recently finished E.H. Gombrich’s A Little History of the World, which was written originally in the 1930s to educate children on the history of the world. The book emphasizes European history, though I really enjoyed the sections on the roots of civilization in Egypt and Middle East. Up until the 1700s and the onset of the Enlightenment, European human existence was relatively miserable. Serfdom, wars, and diseases were constant, and superstitions added another element of misery due to a lack of scientific thought. The book covers many of the amazing scientific accomplishments that occurred along the way. The Renaissance kicked off the rise in scientific thinking, which sought to “…combat the darkness of superstitions with the pure light of reason.” The three fundamental principles of the Enlightenment, also called the Age of Reason, were “tolerance, reason, and humanity,” as “more mysteries of nature were studied and explained than in the preceding two thousand years.”

Why do I bring this up? Last week, CNBC’s Becky Quick interviewed a member of the US-China Economic & Security Review Commission, a body that advises Congress. As he recommended a cybersecurity company, Quick called him out for recommending a company that he advises! As with other Commission members, the conflicts of interest, the lack of economic or China experience and ties to defense companies are blatant conflicts of interest. Quick is the first and only US journalist to point this out. How is that feasible? Is it surprising that Congress is so negative with this group as their “experts”?

This week, a Congressional committee visited New York. Who did they meet with? A short selling hedge fund!!! They visited the home of the largest asset managers in the world and they met with a short selling hedge fund with a few hundred million in assets under management (AUM). Benightedness or existing in a state of intellectual and moral darkness is the opposite of enlightenment, which only explains Washington’s recent rejection of reason, data, and intellectual curiosity.

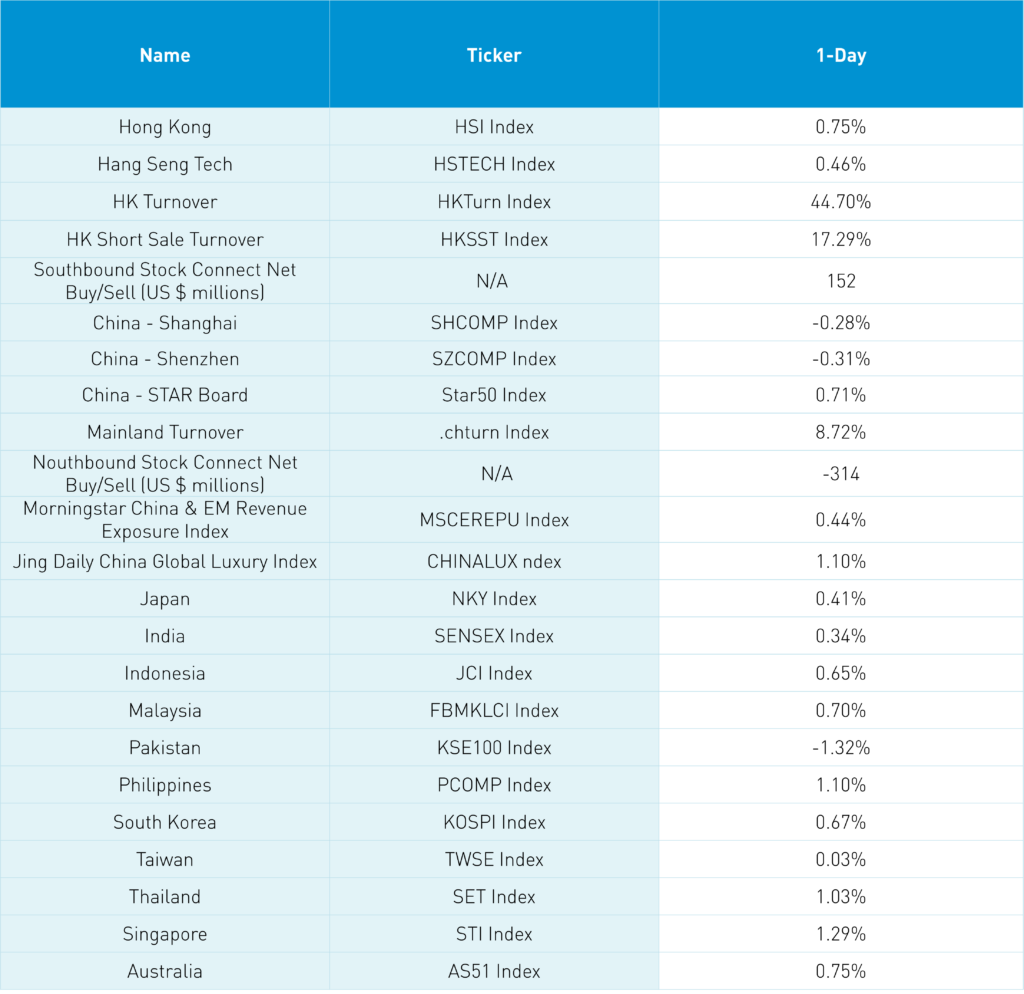

The Hang Seng and Hang Seng Tech indexes gained +0.75% and +0.46%, respectively, on volume that increased +45% from yesterday, which is 10% of the 1-year average. 299 stocks advanced while 183 stocks declined. Main Board short turnover increased +17% from yesterday, which is 95% of the 1-year average as 15% of turnover was short turnover. The growth factor outperformed the value factor as small caps outpaced large caps. The top-performing sectors were Health Care, which gained +2.55%, Materials, which gained +2.09%, and Consumer Staples, which gained +1.09%. Meanwhile, Communication Services fell -0.47%, Real Estate fell -0.39%, and Energy fell -0.35%. The top-performing subsectors were food, pharmaceuticals, and telecom. Meanwhile, diversified finance, software, and energy were among the worst-performing. Southbound Stock Connect volumes were moderate/light as Mainland investors bought a net $152 million worth of Hong Kong-listed ETFs and stocks.

Shanghai, Shenzhen, and the STAR Board diverged to close -0.28%, -0.31%, and +0.71%, respectively, on volume that increased +9% from yesterday, which is 82% of the 1-year average. 2,385 stocks advanced while 2,241 stocks declined. The growth factor outperformed the value factor while small caps outpaced large caps. Health Care was the only positive sector, while utilities fell -1.51%, Consumer Staples fell -1.47%, and Industrials fell -1.17%. The top-performing subsectors were Health Care, Pharmaceuticals, and Biotechnology. Meanwhile, liquor, communication equipment, and gas were among the worst-performing. Northbound Stock Connect volumes were high/moderate as foreign investors sold a net -$314 million worth of Mainland stocks. CNY and the Asia Dollar Index made small gains versus the US dollar. Copper and steel rallied.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.28 versus 7.28 yesterday

- CNY per EUR 7.76 versus 7.74 yesterday

- Yield on 1-Day Government Bond 1.45% versus 1.45% yesterday

- Yield on 10-Year Government Bond 2.64% versus 2.61% yesterday

- Yield on 10-Year China Development Bank Bond 2.76% versus 2.73% yesterday

- Copper Price +0.59%

- Steel Price +1.06%