Huawei & Apple Sales Prove The Strength of The China Consumer

3 Min. Read Time

Key News

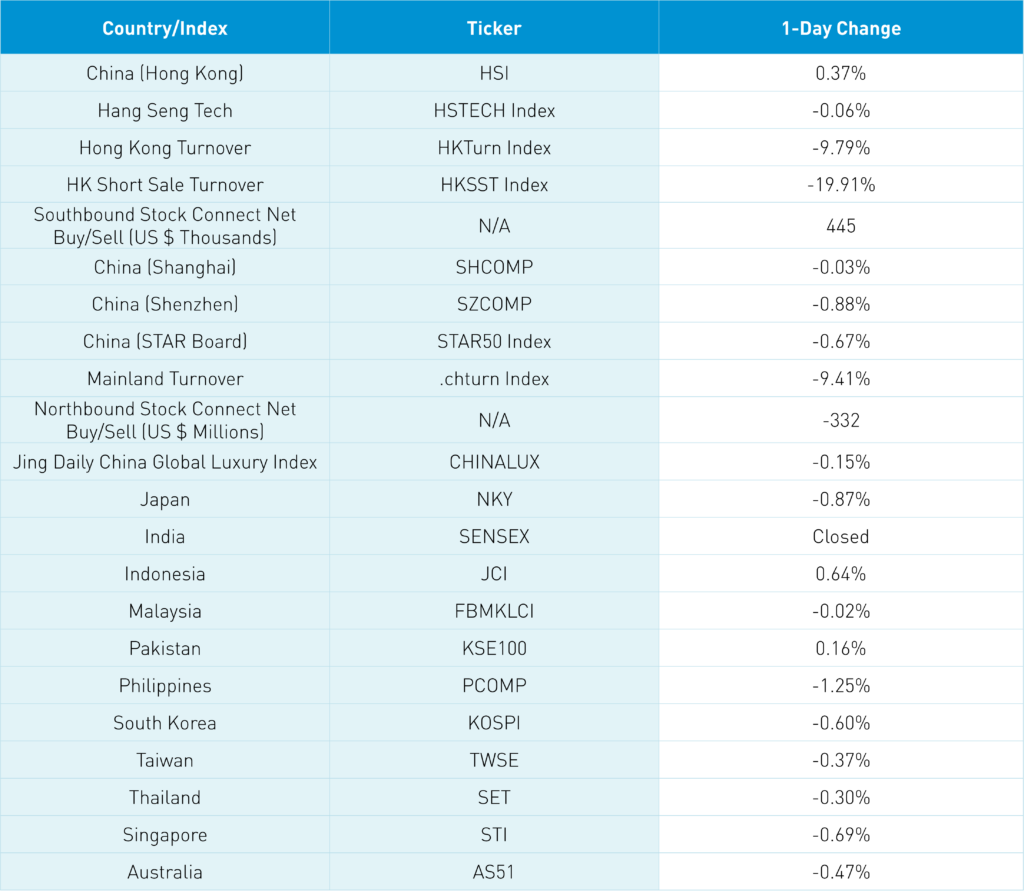

Asian equities were off on light volumes except for Hong Kong. India was closed for Ganesh Chaturthi, a Hindu festival commemorating the birth of the god Ganesha.

Investors are sitting on their hands in advance of central bank meetings. Meanwhile, we continue to see incrementally positive US-China diplomatic and economic news as US Secretary of State Antony Blinken met with Vice President Han Zheng during the United Nations General Assembly. The odds of a Biden-XI summit at the Asia Pacific Economic Cooperation (APEC) meetings this November in San Francisco appear to be increasing.

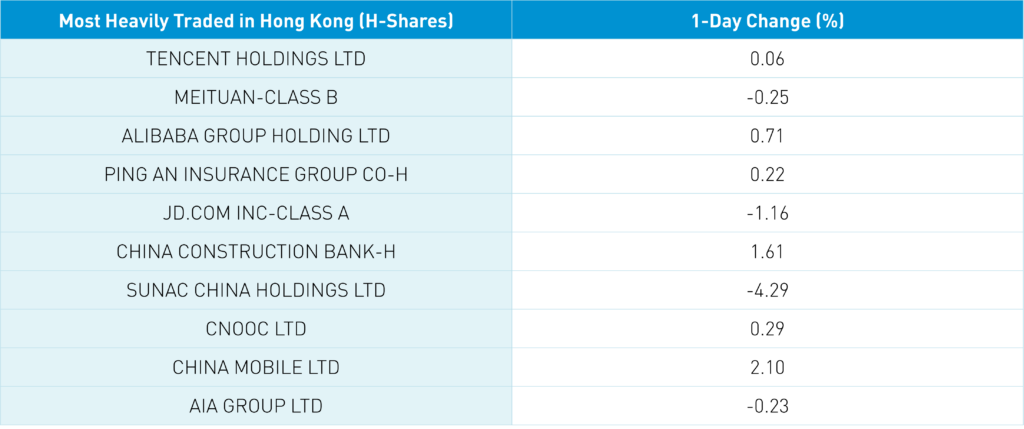

Hong Kong’s most heavily traded stocks by value were Tencent, which gained +0.06% on a new game release, Meituan, which fell -0.25% as the CEO trims his stake in Li Auto, which fell -2.72%, and Alibaba, which gained +0.71% on its expansion in Turkey and Ant Group’s South Korean mobile payment purchase. However, JD.com closed -1.16% lower on no news. Nio fell -4.45% after issuing a convertible bond. Hong Kong Main Board short turnover was 21% of total turnover as buyers remained on the sidelines, though Mainland investors bought $445 million worth of Hong Kong stocks via Southbound Stock Connect.

Mainland markets were off on very light volumes despite continued verbal efforts to improve market sentiment and increase trading from regulators and ministries.

Wuhan joined the growing list of cities removing home purchase restrictions. Meanwhile, distressed developer Sunac filed for Chapter 15 bankruptcy protection to restructure debt, similar to Evergrande’s filing in August.

Huawei’s new Mate 60, Mate 60 Pro, and foldable MateX5 are apparently selling faster than stores can re-stock them. This enthusiasm will affect Apple iPhone sales, though the recent iPhone 15 launch also looks very strong. Consumers can consume the things they want as travel plans look pretty strong. Meanwhile, the PBOC added liquidity to the financial system in advance of the upcoming holiday.

USAFacts.org is an excellent resource as it takes an analytical approach to issues rather than hyperbole, exaggeration, clickbait, and misinformation. The organization recently released its report to Congress, which included the statistic, “17% percent of the US population was 65 or older in 2022 — up from 11% in 1980.” The percentage was higher than I thought, which begs the follow-up question, “Where does the US stand versus other countries?” According to the Population Reference Bureau, the US has a lower percentage of +65 older adults than Japan’s 28.2%, less than Europe and the UK though higher than China’s 11.9%. Would anybody have guessed that the US has a higher percentage of +65 older adults than China? Me neither.

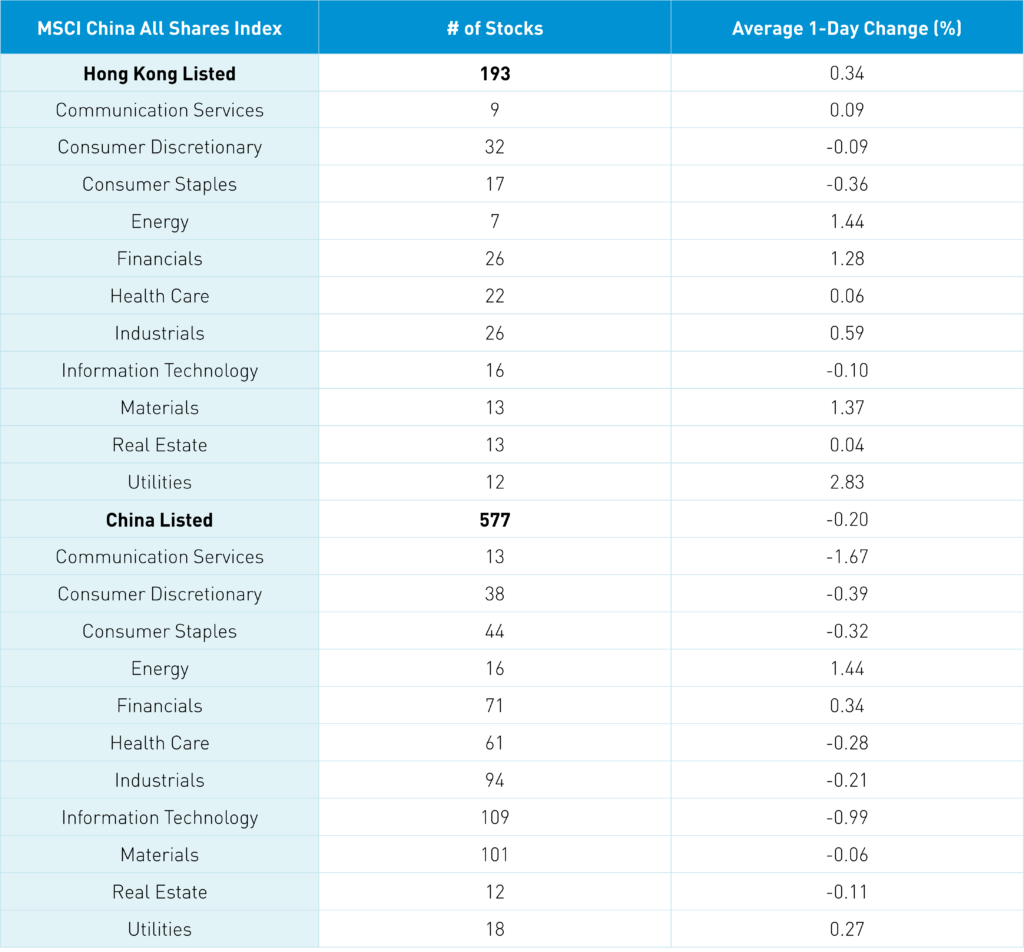

The Hang Seng and Hang Seng Tech indexes diverged to close +0.37% and -0.06%, respectively, on volume that decreased -9.79% from yesterday, which is 66% of the 1-year average. 238 stocks advanced, while 238 declined. Main Board short turnover declined -19.9% from yesterday, which is 82% of the 1-year average, as 21% of turnover was short turnover. The value factor outperformed the growth factor as large caps outpaced small caps. The top-performing sectors were Utilities, which gained +2.83%, Energy, which gained +1.44%, Materials, which gained +1.37%, Consumer Staples, which fell -0.36%, Technology, which fell -0.1%, and Consumer Discretionary, which fell -0.09%. The top-performing subsectors were Telecom, Utilities, and Materials. Meanwhile, Auto Parts, Consumer Services, and Business Services were among the worst. Southbound Stock Connect volumes were light as Mainland investors bought a net $445 million worth of Hong Kong-listed stocks and ETFs with Ping An and Meituan as slight net buys and Li Auto and CNOOC as small net sells.

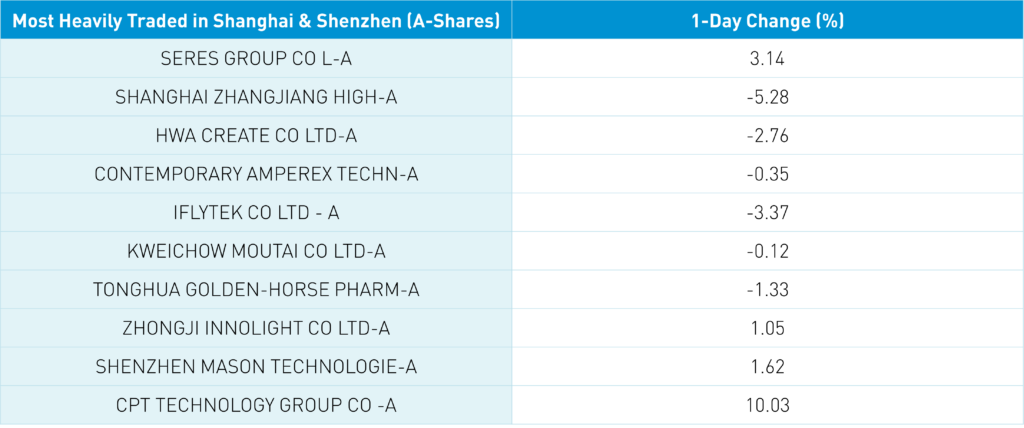

Shanghai, Shenzhen, and the STAR Board fell -0.03%, -0.88%, and -0.67%, respectively, on volume that decreased -9.41% from yesterday, which is 72% of the 1-year average. 864 stocks advanced, while 3,853 declined. The value factor outperformed the growth factor as large caps “outperformed” (i.e. fell less than) small caps. The top-performing sectors were Energy, which gained +1.45%, Financials, which gained +0.34%, and Utilities, which gained +0.28%. Meanwhile, Communication Services fell -1.67%, Technology, which fell -0.98%, and Consumer Discretionary, which fell -0.38%. The top-performing subsectors were Highways, Oil & Gas, and Energy Equipment. Meanwhile, Restaurants, Education, and Internet were among the worst-performing. Northbound Stock Connect volumes were light as foreign investors sold a net -$332 million worth of Mainland stocks with the Bank of Jiangsu and the Agricultural Bank of China as small net buys. Meanwhile, LONGi Green Energy, Kweichow Moutai, and Wuliangye Yibin were slight net sells. Treasury bond prices fell. CNY and the Asia Dollar Index were flat versus the US dollar. Copper fell again while steel gained.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.29 versus 7.29 yesterday

- CNY per EUR 7.79 versus 7.78 yesterday

- Yield on 10-Year Government Bond 2.66% versus 2.65% yesterday

- Yield on 10-Year China Development Bank Bond 2.76% versus 2.76% yesterday

- Copper Price -0.55%

- Steel Price +0.89%