A Positive Start To A Big Week For US-China Relations

2 Min. Read Time

Key News

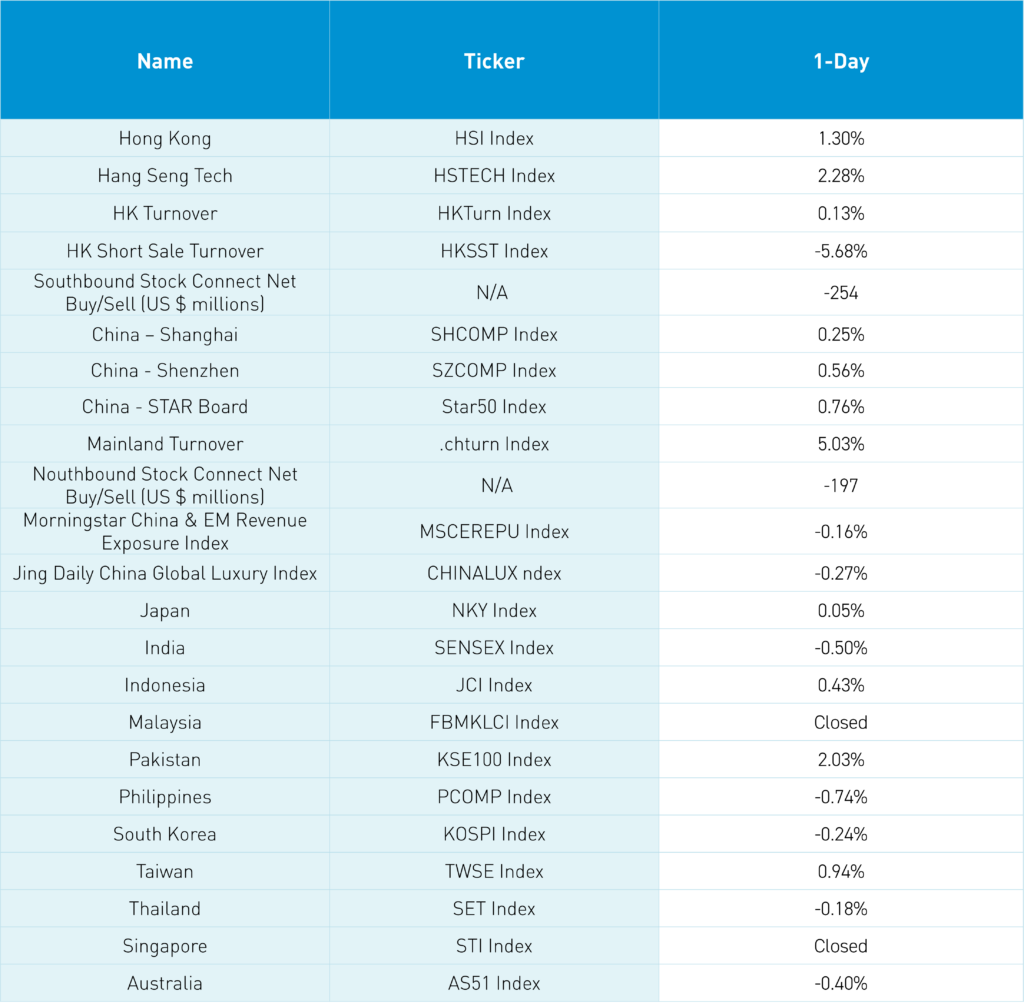

Asian equities were mixed as Hong Kong outperformed on a late-day rally as Singapore and Malaysia were closed for Diwali.

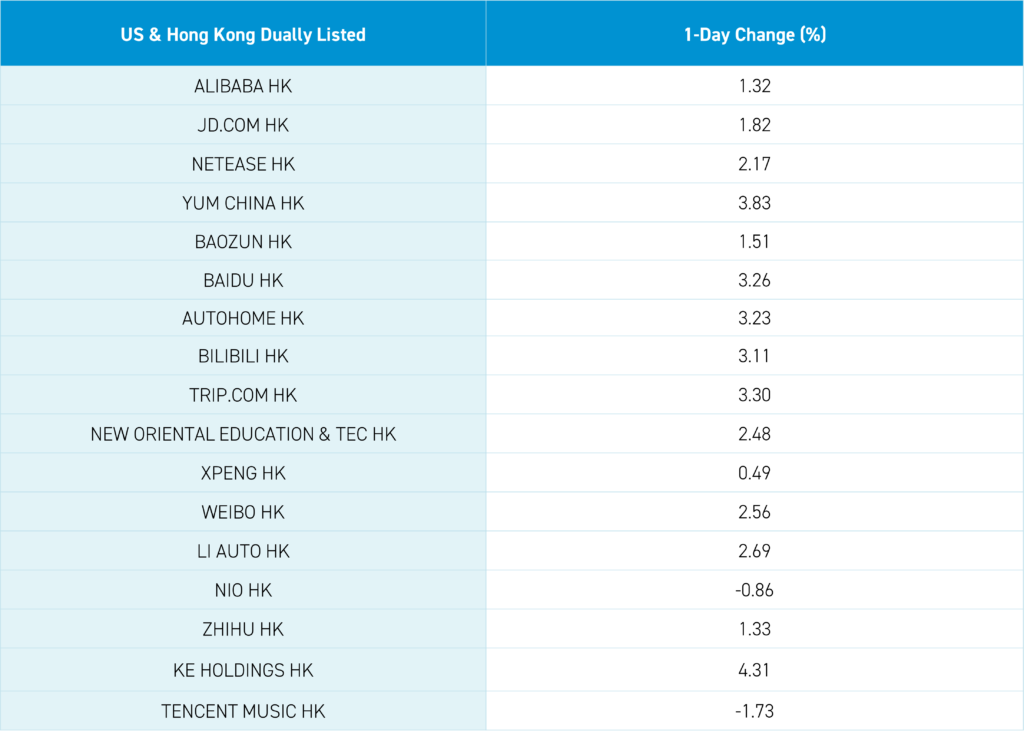

Singles Day, the Super Bowl of Shopping, occurred on Saturday. Overnight, Alibaba gained +1.32%, JD.com gained +1.82%, and Kuiashou gained +4.85%, respectively, as the companies reported a year-over-year increase in sales, though exact amounts were not released. Alibaba announced 402 brands sold more than RMB 100 million worth of gross merchandise value (GMV) “while 38,000 brands achieved over 100% year-on-year growth in GMV.”

Hong Kong had a strong day, though volumes were a touch light. Mainland investors sold several Hong Kong-listed ETFs via Southbound Stock Connect after buying them last week. It was a quiet weekend that included the Asia Pacific Economic Cooperation (APEC) Conference kicking off in San Francisco. Presidents Biden and Xi are expected to meet later in the week. Chinese media coverage of the US has taken a positive tone over the last few weeks, a marked departure from recent coverage as both sides have used one another to distract from domestic issues.

Mainland China grinded higher led by growth stocks/sectors despite foreign investors selling via Northbound Stock Connect. After the close, October aggregate financing came in at RMB 1.85 trillion, which missed expectations of RMB 1.95 trillion and September’s RMB 4.12 trillion. Meanwhile, new loans of RMB 738 billion came in ahead of an expected RMB 655 billion and September’s RMB 2.31 trillion. The money supply (M2) increased year-over-year by +10.3%. October industrial production and retail sales will be released on Wednesday.

It is shaping up to be a busy week for Q3 financial results as Meituan reports tomorrow, Tencent and JD.com report on Wednesday, and Alibaba reports Thursday.

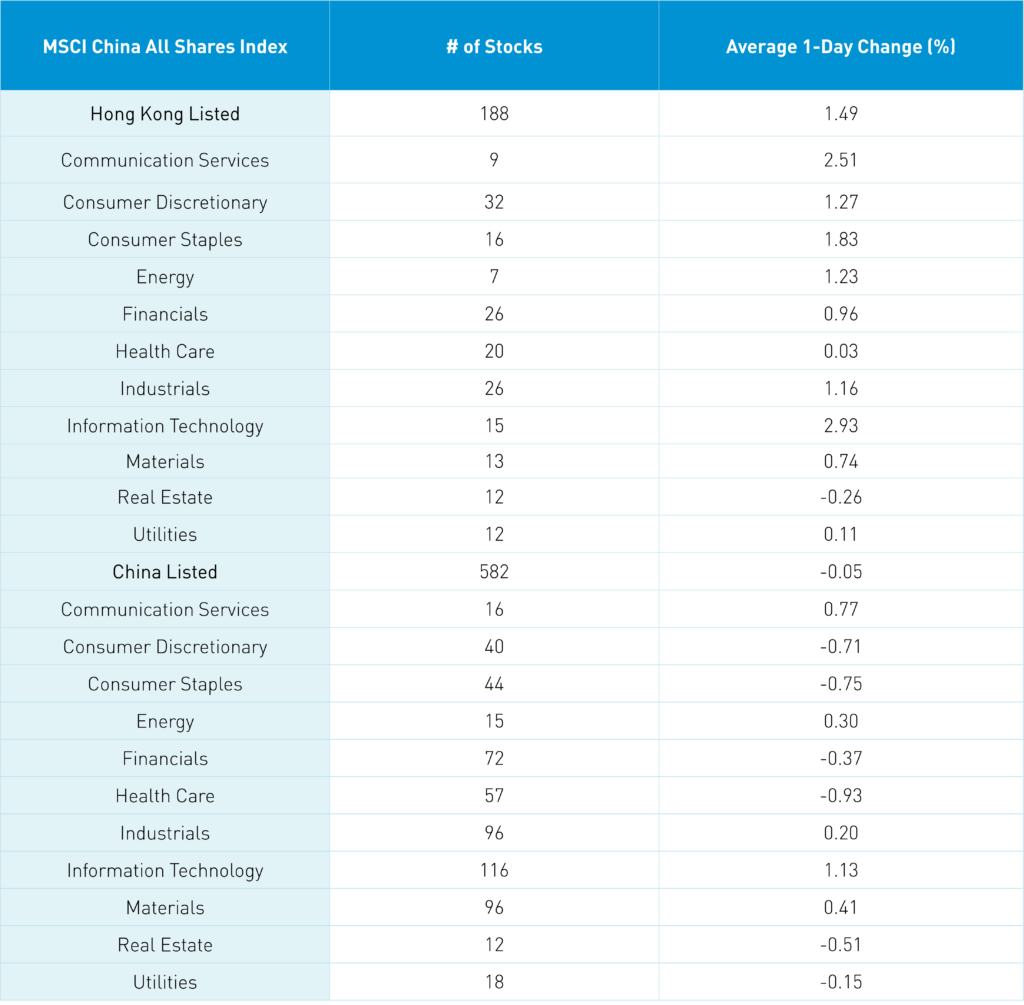

The Hang Seng and Hang Seng Tech indexes gained +1.30% and +2.28%, respectively, on volume that increased +0.13% from Friday, which is 68% of the 1-year average. 341 stocks advanced while 139 declined. Main Board short sale turnover declined -5.64% from Friday, which is 76% of the 1-year average (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). Value and growth factors were mixed while small caps outperformed large caps. The top-performing sectors were technology, which gained +2.94%, communication services, which gained +2.52%, and consumer staples, which gained +1.84%. Meanwhile, real estate was the only negative sector, falling by -0.25%. All subsectors were positive as semiconductors, software, and household products outperformed. Southbound Stock Connect volumes were light/moderate as mainland investors sold a net -$254 million worth of Hong Kong-listed stocks and ETFs, including Kuaishou, which was a small net buy, the Hong Kong Tracker ETF, which was a moderate/large net sell, Meituan and the H Share ETF, which were both small net sells.

Shanghai, Shenzhen, and the STAR Board gained +0.25%, +0.56%, and +0.76%, respectively, on volume that increased +5.03% from Friday, which is 99% of the 1-year average. 3,686 stocks advanced while 1,158 declined. The growth factor outperformed the value factor while small caps outpaced large caps. The top-performing sectors were technology, which gained +1.13%, communication services, which gained +0.77%, and materials, which gained +0.41%. Meanwhile, healthcare fell -0.92%, consumer staples, which fell -0.75%, and consumer discretionary, which fell -0.71%, were the worst-performing. The top-performing subsectors were aerospace/military, education, and software. Meanwhile, household products, chemicals, and liquor were among the worst-performing. Northbound Stock Connect volumes were moderate as foreign investors sold a net -$197 million worth of Mainland stocks overnight with HR, Mindray, and IFLYTEK among the small net buys. Meanwhile, Ping An, Sunway, and BYD were all small net sells. CNY and the Asia Dollar Index fell slightly versus the US dollar. The Treasury curve steepened while copper was off, and steel gained.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.29 versus 7.29 Friday

- CNY per EUR 7.79 versus 7.79 Friday

- Yield on 1-Day Government Bond 1.40% versus 1.40% Friday

- Yield on 10-Year Government Bond 2.65% versus 2.64% Friday

- Yield on 10-Year China Development Bank Bond 2.71% versus 2.71% Friday

- Copper Price -0.38% overnight

- Steel Price +0.21% overnight