Politburo Meeting Focuses On Foreign Investment, Week in Review

2 Min. Read Time

Week in Review

- Asian equities had another mixed week as South Asia outperformed North Asia, and the Yen strengthened on speculation of another adjustment to the Bank of Japan’s yield curve control policy.

- Contract medical research giant WuXi Biologics saw steep declines this week on a negative medium-term growth outlook primarily due to the fading of COVID windfalls and less funding for global biotechs in a higher interest rate environment.

- Moody’s downgraded its outlook for China following a similar downgrade for the US from Fitch despite China’s sovereign debt-to-GDP ratio of 50% compared to the US’ 121%.

- In China, increased corporate buybacks and better-than-expected trade data failed to lift markets, though we did see strong buying in Hong Kong from Mainland investors.

Friday’s Key News

Asian equities were mixed overnight as Mainland China outperformed Hong Kong. A US jobs report that came in below 2023’s average for November gave more confidence that the Fed could be finished hiking interest rates.

China’s Politburo met today, and President Xi made it clear that attracting foreign capital was a top priority, in a statement. The top policymaking committee also discussed prioritizing “sustainable economic growth.” The meeting is in preparation for the Central Economic Work Conference (CEWC), which will be held later this month and will outline economic policy priorities for the coming year. Will this mean another big stimulus announcement? Not necessarily, but policy is expected to remain accommodative.

The Caixin Services PMI was released on Monday, showing a reading of 51.5, which is expansionary territory, versus an estimated 50.7. This was only a slight beat, but is still an indication that China’s economic data may have bottomed out.

Tencent unveiled a new console game overnight: The Last Sentinel. Console games are a new field for the technology giant. Reportedly, the company is working with former Rockstar Games developers on the project.

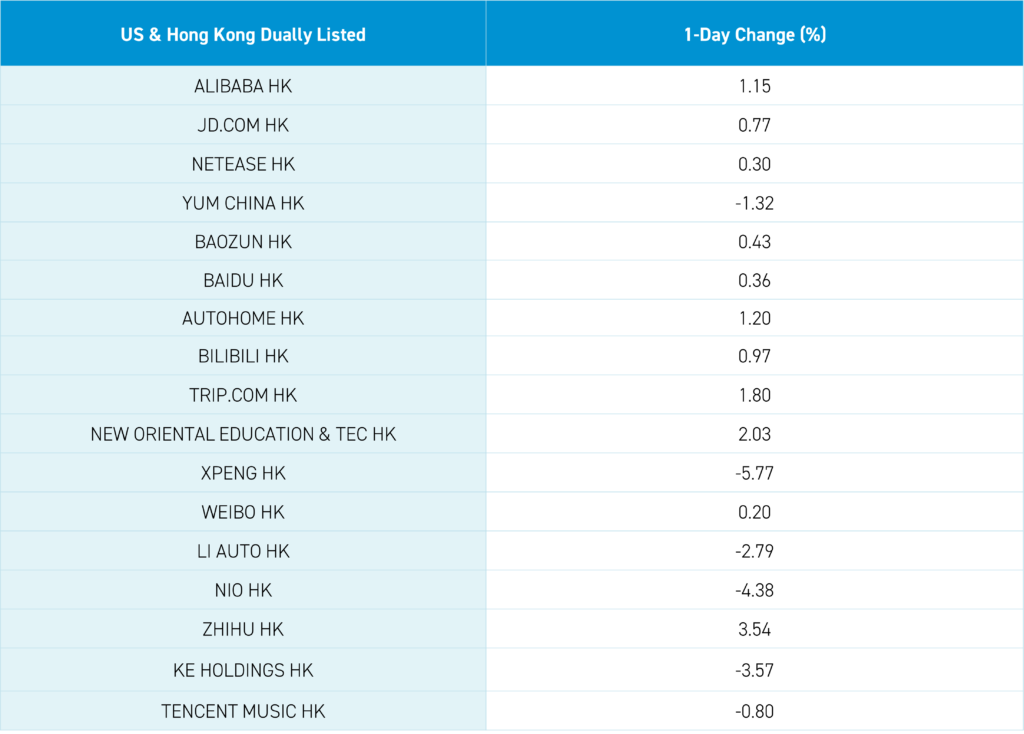

The electric vehicle ecosystem was mostly lower overnight. NIO said it would be laying off about 10% of its workforce in a push to cut costs in the face of increasing competition.

Health care stocks were higher in Mainland China. Evidently, investors in Mainland China are not as pessimistic about the industry as their Hong Kong counterparts.

Consumer discretionary was the only positive sector in Hong Kong, helped by Alibaba, which gained +1% and was one of Hong Kong’s most traded stocks. The internet sector overall was higher overnight. Google’s successful launch of its Gemini AI model could provide some positive momentum for Baidu.

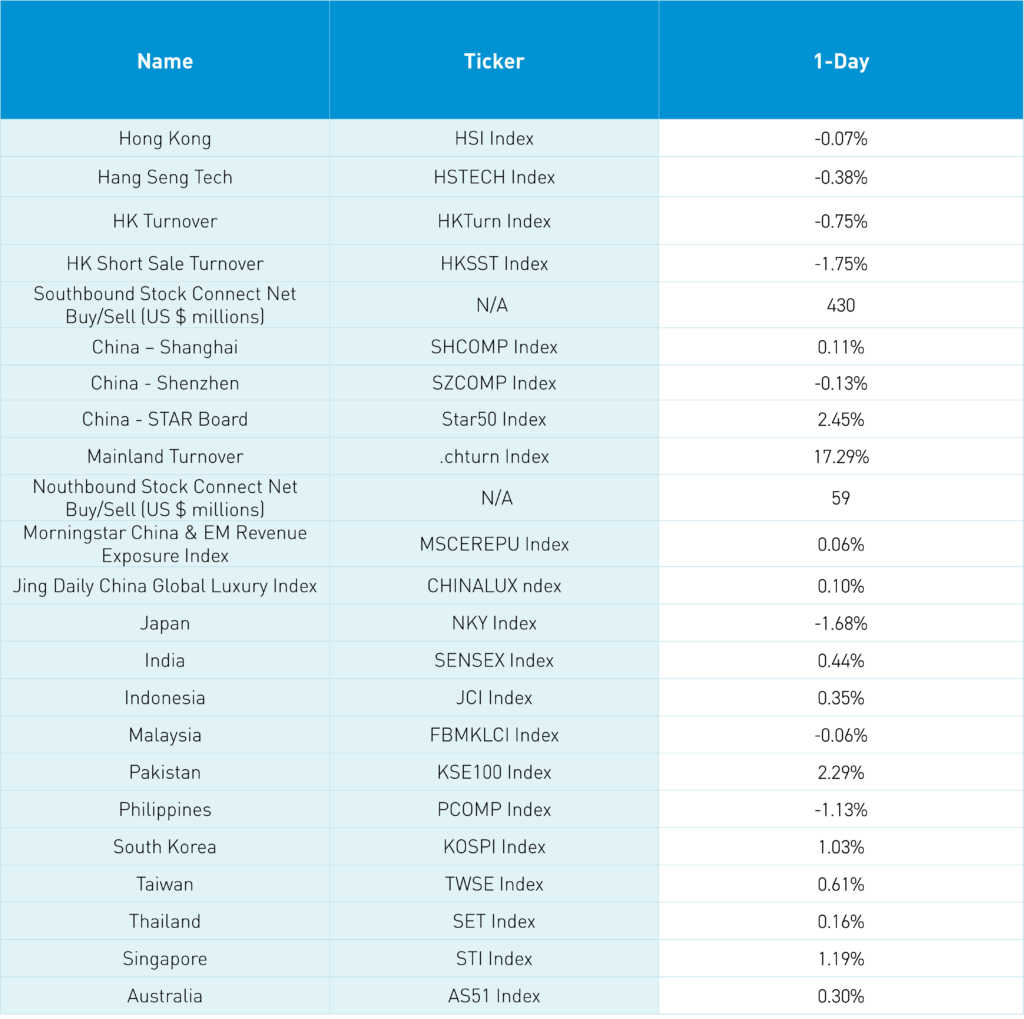

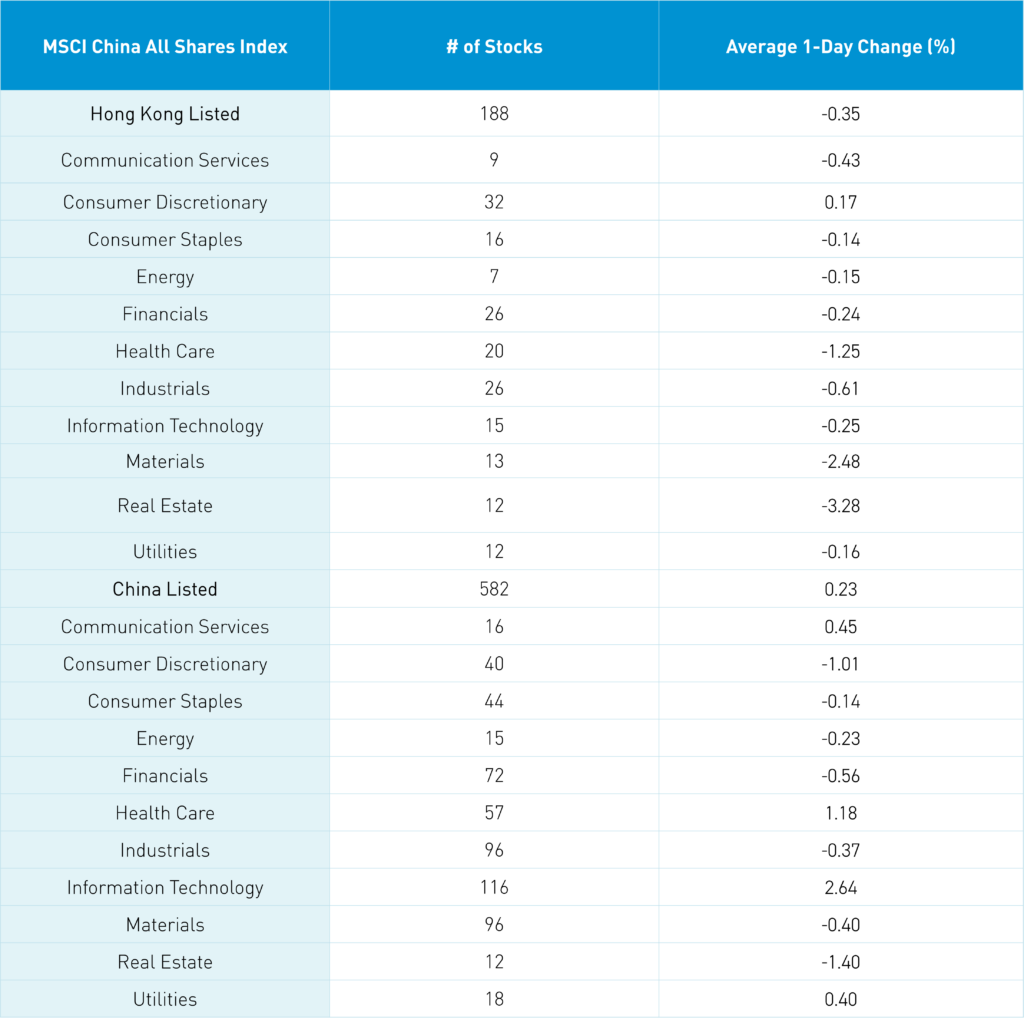

The Hang Seng and Hang Seng Tech indexes both closed slightly lower by -0.07% and -0.38%, respectively, on volume that decreased -2% from yesterday. Mainland investors bought a net $430 million worth of Hong Kong stocks overnight via Southbound Stock Connect. The top-performing sectors overnight were Consumer Discretionary, which gained +0.17%, Consumer Staples, which fell -0.14%, and Energy, which fell -0.15%. Meanwhile, the worst-performing sectors were Real Estate, which fell -3.28%, Materials, which fell -2.48%, and Health Care, which fell -1.25%.

Shanghai, Shenzhen, and the STAR Board diverged to close 0.11%, -0.13%, and 2.45%, respectively, on volume that increased +17% from yesterday. Foreign investors bought a net $59 million worth of Mainland stocks via Northbound Stock Connect. The top-performing sectors overnight were Information Technology, which gained +2.64%, Health Care, which gained +1.18%, and Communication Services, which gained +0.45%. Meanwhile, the worst-performing sectors were Real Estate, which fell -1.40%, Consumer Discretionary, which fell -1.01 %, and Financials, which fell -0.56%. CNY depreciated slightly versus the US dollar, government bonds were flat, and copper and steel were both higher.

Last Night’s Performance

Last Night's Exchange Rates, Prices, & Yields

- CNY per USD 7.17 versus 7.15 yesterday

- CNY Per EUR 7.71 versus 7.72 yesterday

- Yield on 1-Day Government Bond 1.22% versus 1.20% yesterday

- Yield on 10-Year Government Bond 2.66% versus 2.66% yesterday

- Yield on 10-Year China Development Bank Bond 2.78% versus 2.78% yesterday

- Copper Price +1.30%

- Steel Price +0.30%