No Policy Lift In Hong Kong With Mainland Closed, Week in Review

2 Min. Read Time

Week in Review

- Asian equities were mixed but mostly higher this week as Mainland China outperformed with a gain of +3.43% for Shanghai, +2.57% for Shenzhen, and +8.91% for the STAR Board.

- On Monday, Hong Kong reversed an intra-day decline thanks to new rules around institutional investors’ ability to sell stock short. This market support measure was followed by Huijin central Investment, a state-linked investor, stating its intention to increase holdings of stocks and ETFs, the confirmation of the establishment of a stabilization fund, and Xi Jinping’s meeting with the China Securities Regulatory Commission (CSRC), China’s SEC.

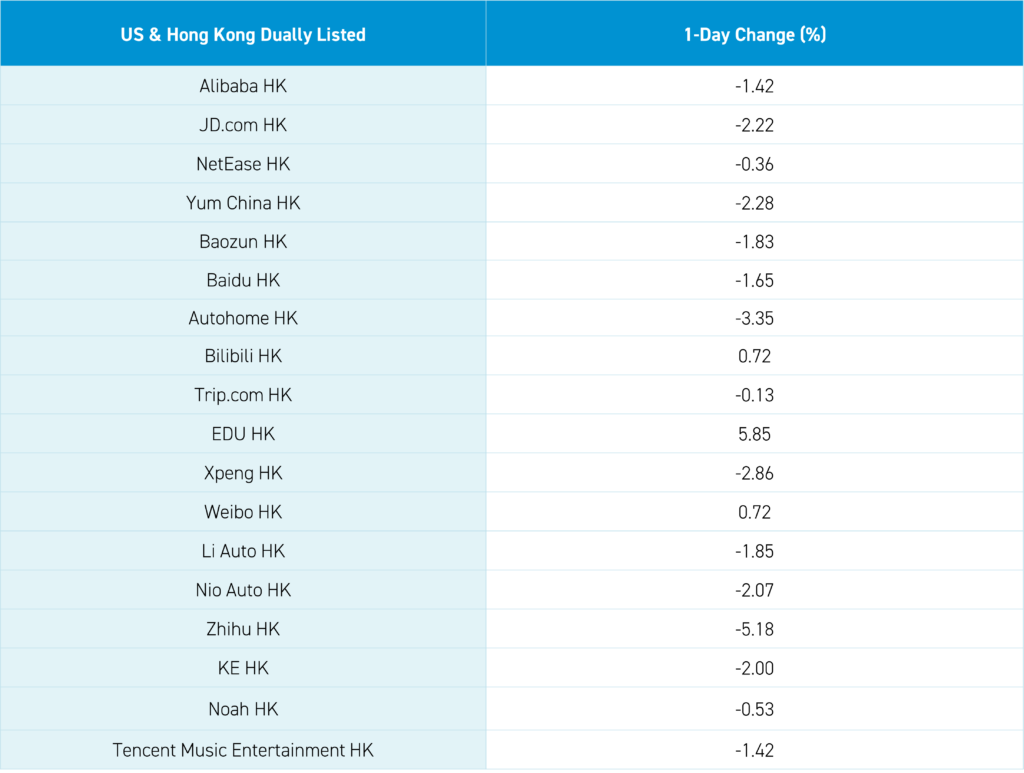

- Alibaba reported earnings on Wednesday, beating on its bottom line but missing on top line revenue and increasing its share buybacks. The stock sold off on concerns about new listings, which the company said were on hold until market conditions improve, and increased expenses to defend its market share from the likes of Pinduoduo.

- China’s inflation rate in January, reported Thursday, was -0.80% while the producer price index was also negative, at –2.5%, though higher than the expected -2.6%.

Friday’s Key News

Asian equities were mixed but mostly higher overnight though Hong Kong closed lower in a half-day session and Mainland China was closed for the Lunar (Chinese) New Year holiday.

At a Lunar New Year event, President Xi stated that China must build on its economic recovery progress. However, this pro-equity statement failed to lift Hong Kong-listed stocks, which were not helped by the Mainland market being closed. Policy statements tend to impact Mainland markets more than the mostly foreign-owned Hong Kong market. We will have to wait a week to see how the positivity from China’s leader will impact Mainland (Onshore, A share) stocks, as the Shanghai and Shenzhen stock exchanges will be closed all next week.

The People’s Bank of China (PBOC) released its monetary policy report overnight. In the report, China’s central bank stated that it intends to ensure stable and abundant liquidity in the markets. At the same time, a state-run media outlet reported that China’s inflation rate is expected to grow at a “moderate” clip in 2024, in contrast to the deflation indicated by the January consumer price index (CPI). This can only happen with more rate cuts and stimulus.

Long-time CSRC Chair Yi Huiman has been relieved of his post and he will be replaced by Wu Qing, deputy party secretary of Shanghai. This is further evidence of top leadership’s disappointment in the markets chief’s ability to stabilize stock markets and attract foreign investment. Stock markets have become a political priority for Beijing, which is a significant change from its past posture.

Education stocks gained overnight on further clarification of the private tutoring policy. Real estate gave back some of its gains from earlier this week. Shipping names were lower after Maersk issued a negative guidance for the year, excluding the increase in rates due to Red Sea conflicts. Automakers broadly were lower on decreased overall car sales in 2023, though electric vehicle sales increased to over 9 million compared to 6 million in 2022.

Hong Kong will be closed on Monday and Tuesday and Mainland markets will be closed all next week. As such, China Last Night will resume reporting on Wednesday, February 14th (Valentines’ Day).

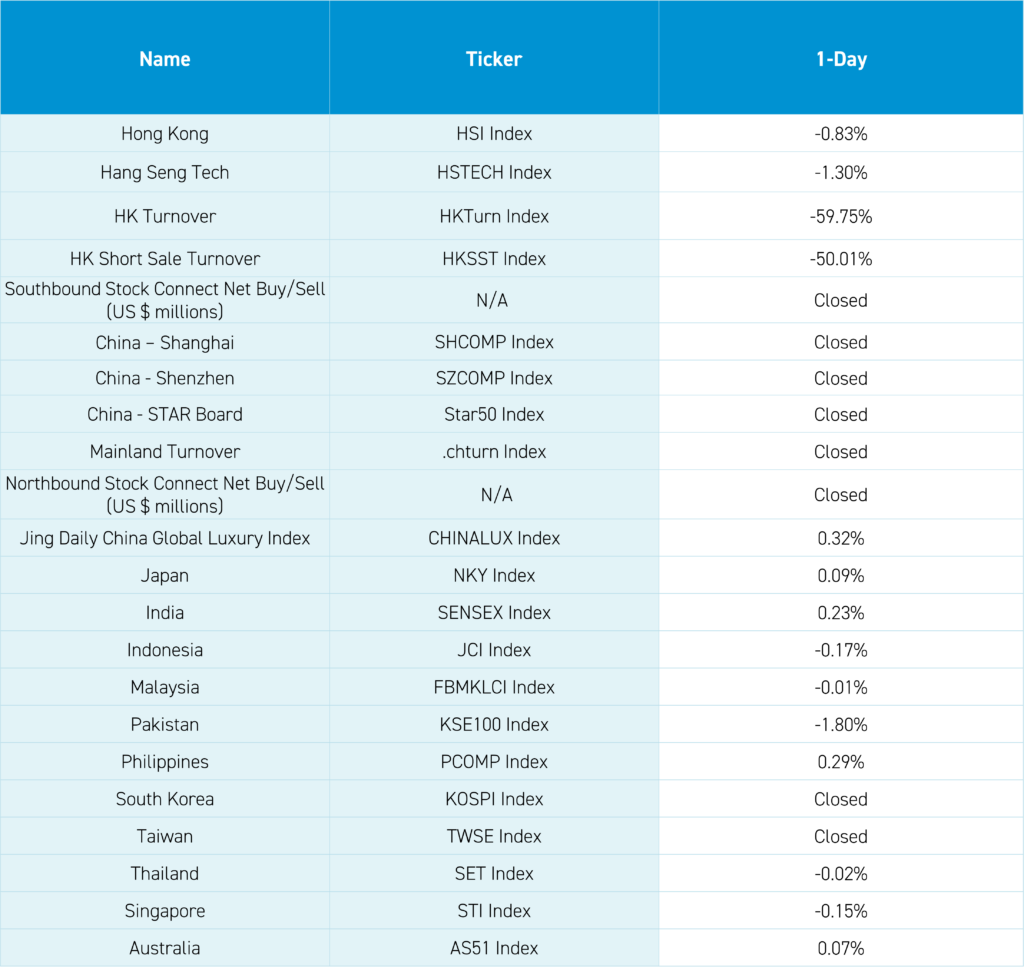

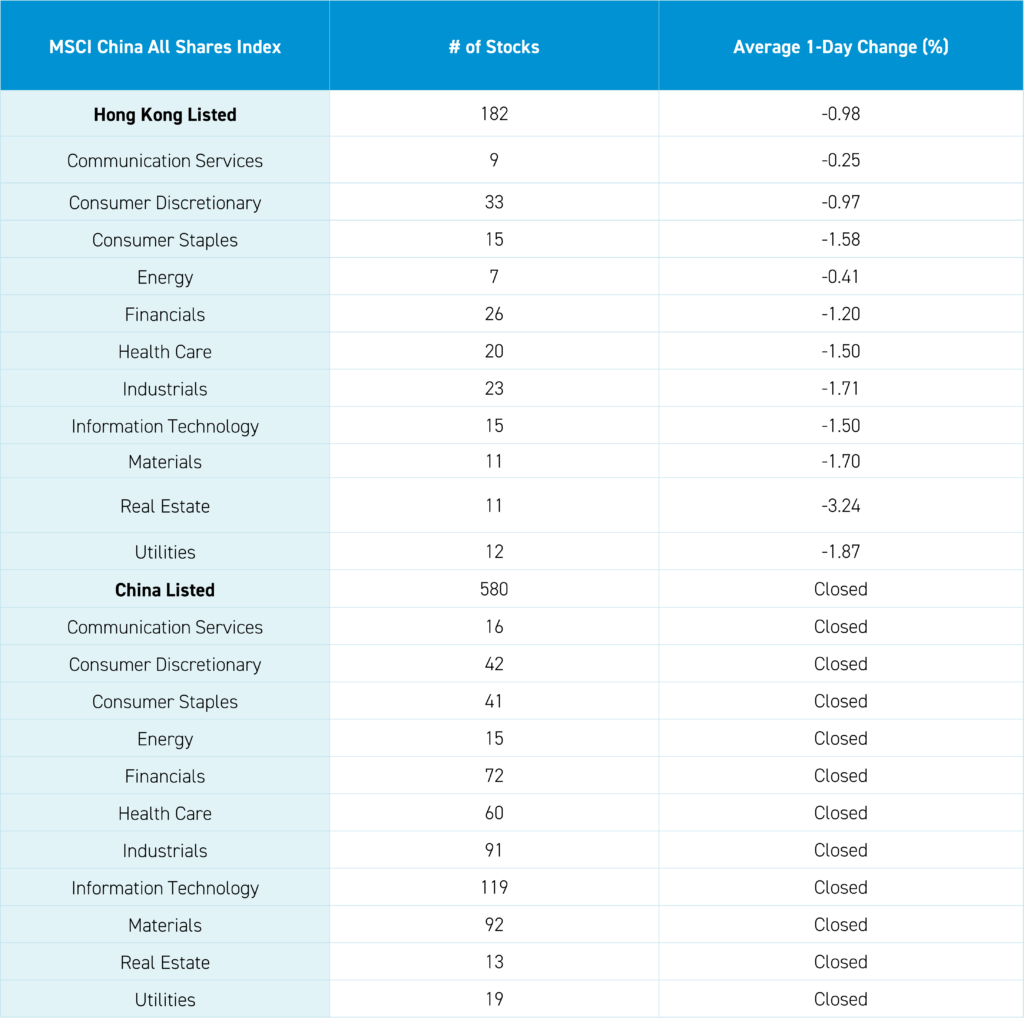

The Hang Seng and Hang Seng Tech indexes both closed lower by -0.83% and -1.30%, respectively, on volume that decreased -60% from yesterday. Southbound Stock Connect was closed. The top-performing sectors were Communication Services, which fell -0.25%, Energy, which fell -0.41%, and Consumer Discretionary, which fell -0.97%. Meanwhile, the worst-performing sectors were Real Estate, which fell -3.24%, Utilities, which fell -1.87%, and Industrials, which fell -1.71%.

Last Night’s Performance

Last Night’s Exchange Rates, Prices, & Yields

Mainland fixed income and currency markets were closed overnight.