Mainland Stocks Enter The Year of The Dragon Higher

3 Min. Read Time

Key News

Asian equities were higher on light volumes, with mainland China reopening higher on the first trading day since Thursday, February 9th, on strong volume, while Hong Kong was hit with profit-taking after last week’s rally.

Lunar (Chinese) New Year travel and consumption data were strong, as the government reported 474 million trips, which represents an increase of +34% year-over-year (YoY). Meanwhile, domestic tourism spending during the week-long holiday increased +47.3% YoY to approximately RMB 632 billion. Compared to pre-pandemic 2019, the number of trips increased +19% and spending increased +7.7%. The spin doctors (i.e., the nattering nabobs of negativity) are saying that the New Year’s vacation data is poor because, on a “per-capita” basis, it is less than 2019 levels. Give me a break.

Mainland-listed stocks entered the Year of the Dragon on a strong note, as several China ETFs saw high volumes, including by the National Team, which refers to institutional investors affiliated with the government. It was reported that the sovereign wealth fund Central Huijin, was supporting the market. As a parent, one often has the “I’m not asking you, I’m telling you” conversation with your children. The Chinese government is telling you to buy stocks, as they stabilize the market, which is exactly what they did in the summer of 2015. Garnering less attention are the 329 mainland companies that have announced buybacks, with another 829 implementing buybacks.

OpenAI’s announcement of their Sora text-to-video tool lifted AI names, though Apple suppliers were weak on an underwhelming response to the Vision Pro and increased competition.

As anticipated, the Medium-Term Lending Facility (MLF) rate, which is the rate at which banks borrow from the PBOC, was left unchanged at 2.50%. The Loan Prime Rate (LPR) will be announced overnight, though it is not expected to be cut, either. Many believe the PBOC will not cut these rates until the US Fed cuts to prevent an accelerated Renminbi (CNY) decline versus the US dollar. CNY has been very stable versus the US dollar lately.

The State Council meeting release overnight was focused on the economy and supportive policies, though it didn’t appear to be a market mover.

Secretary of State Blinken met with Foreign Minister Wang Yi at the Munich Security Conference on Friday.

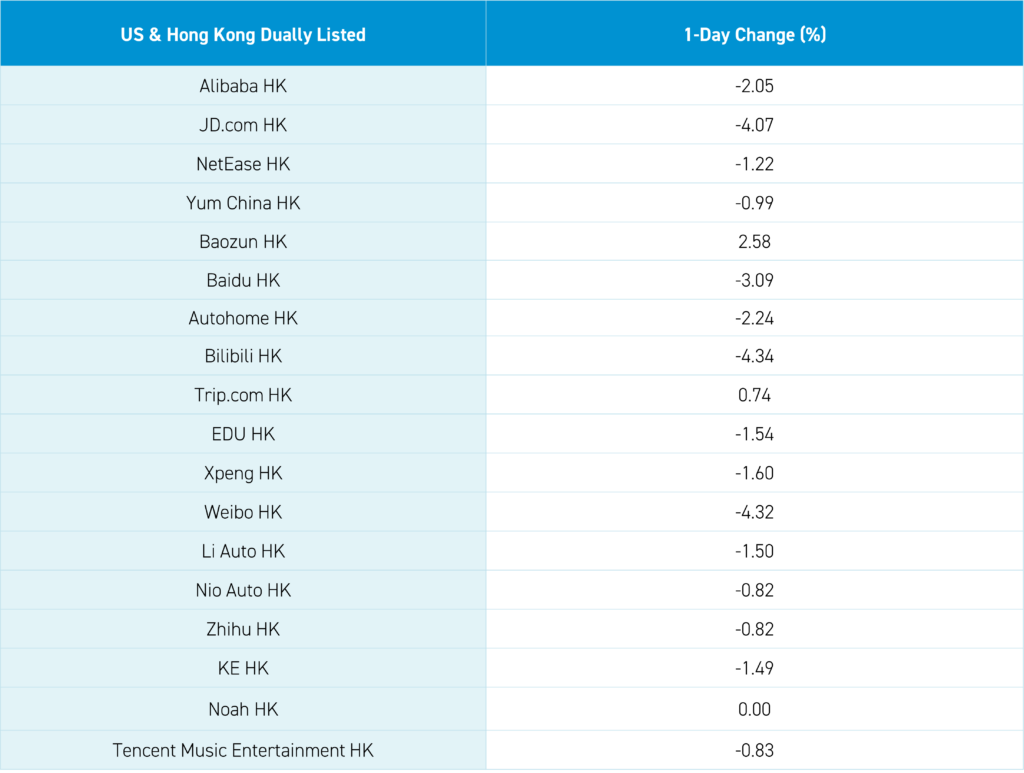

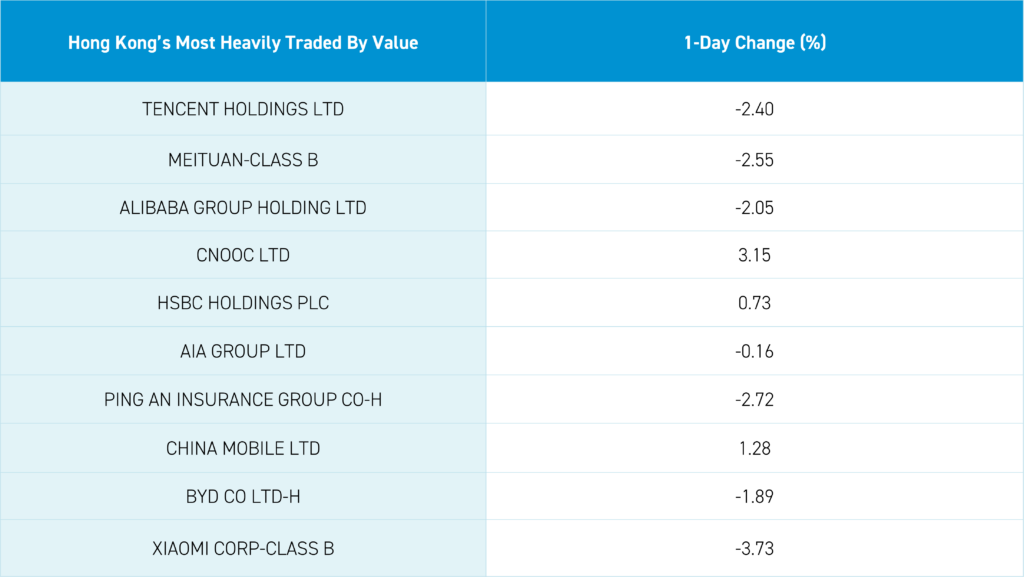

Hong Kong was off on profit-taking, as recently outperforming stocks and subsectors, including, travel, Macau casinos, and internet, were sold off. Hong Kong’s most heavily traded stocks by value were Tencent, which fell -2.40%, Meituan, which fell -2.55%, Alibaba, which fell -2.05% despite a prominent local manager’s filing of an ownership position with the SEC, energy giant CNOOC, which gained +3.15%, and HSBC, which gained +0.73%. Mainland investors bought the dip via Southbound Stock Connect. JD.com fell -4.07% on chatter that the company will buy UK electronic retailer Curry, in a true head-scratcher. Meanwhile, BYD fell -1.89%, and the EV ecosystem was off on price war fears after the company launched its Qin PLUS Honor at a price of RMB 70,000, despite it being worth 78,000.

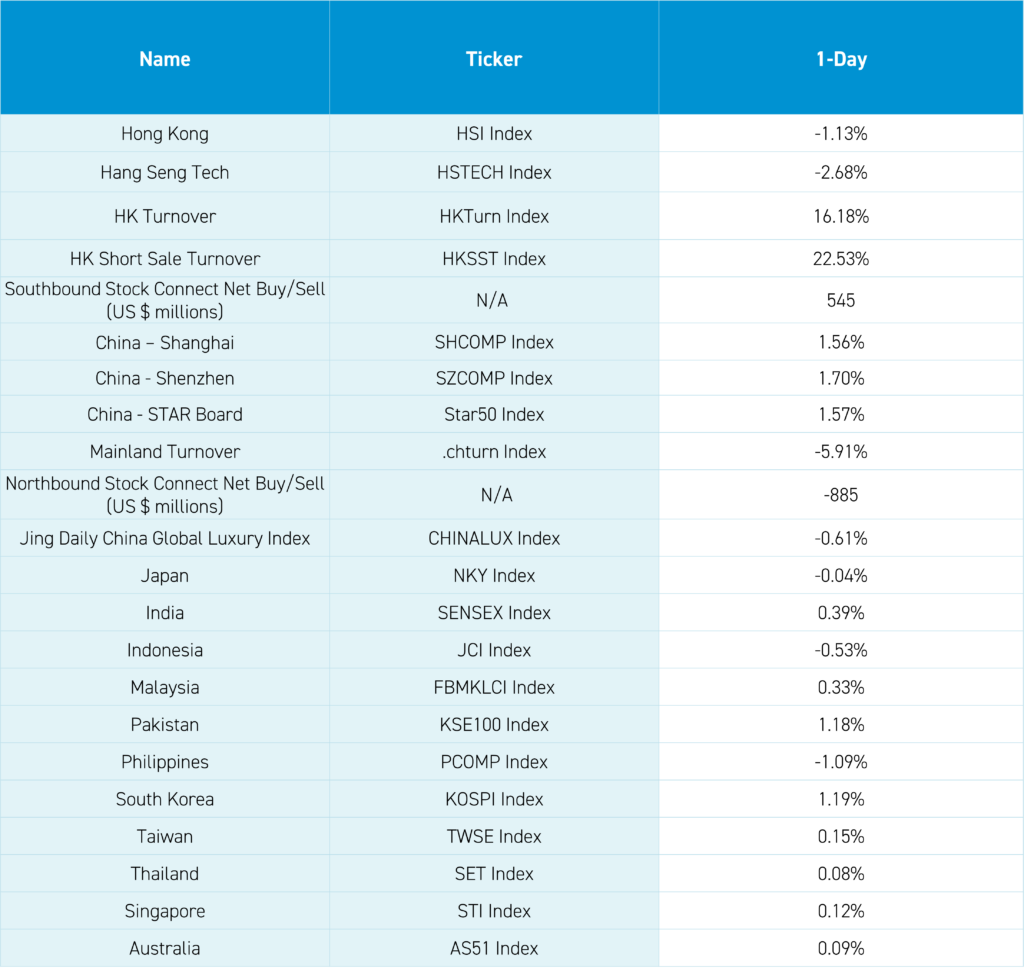

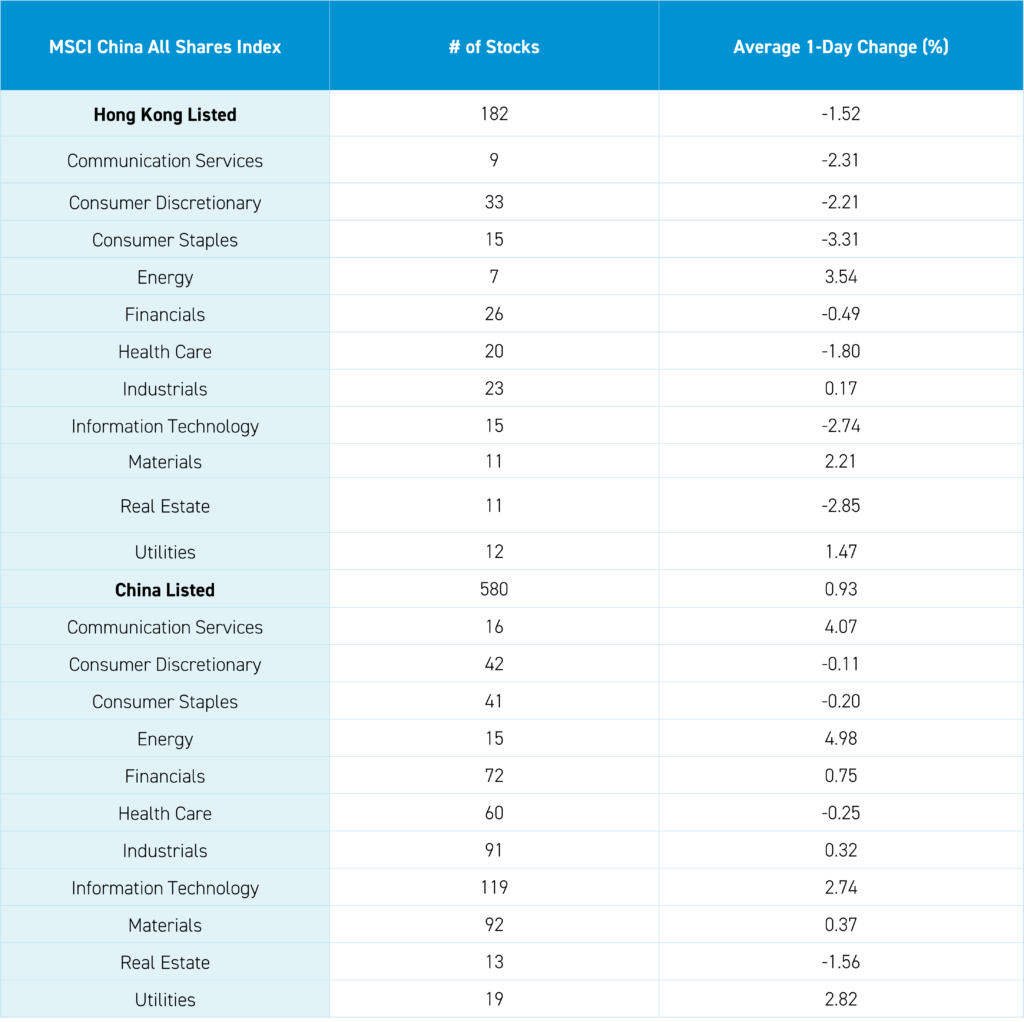

The Hang Seng and Hang Seng Tech indexes fell -1.13% and -2.68%, respectively, on volume that increased +16.27% from Friday, which is 83% of the 1-year average. 143 stocks advanced, while 351 declined. Main Board short turnover increased by +22.54% from Friday, which is 76% of the 1-year average, as 16% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). The value factor and large caps “outperformed” (i.e. fell less than) the growth factor and small caps. The top-performing sectors were Energy, which gained +3.55%, Materials, which gained +2.22%, and Utilities, which gained +1.48%. Meanwhile, Consumer Staples fell -3.3%, Real Estate fell -2.84%, and Technology fell -2.73%. The top-performing subsectors were energy, telecom, and materials. Meanwhile, food, beverages, and semiconductors were among the worst-performing subsectors. Southbound Stock Connect volumes were moderate/light as Mainland investors bought a net $545 million worth of Hong Kong-listed stocks and ETFs, including energy giant CNOOC, China Mobile, and China Telecom. Meanwhile, Semiconductor Manufacturing (SMIC), Tencent, and HSBC had very small net sales.

Shanghai, Shenzhen, and STAR Board gained +1.56%, +1.7%, and +1.57%, respectively, on volume that declined -5.91% from Thursday, February 9th, which is 111% of the 1-year average. 3,928 stocks advanced, while 1,028 declined. All factors were positive with the value and large cap outperforming growth and small caps. The top-performing sectors were Energy, which gained +4.98%, Communication Services, which gained +4.07%, and Utilities, which gained +2.82%. Meanwhile, Real Estate fell -1.56%, Health Care fell -0.25%, and Consumer Staples fell -0.20%. The top-performing subsectors were computer hardware, education, and internet. Meanwhile, securities, agriculture, and airports were among the worst-performing. Northbound Stock Connect volumes were elevated as foreign investors sold a net -$885 million worth of Mainland stocks, as Kweichow Moutai was a large net buy, and Midea Group and CMB were moderate net buy. Meanwhile, Wuxi AppTec was a large net sell, and Foxconn and Zhongli Innolight were small net sales. CNY was slightly lower than the US dollar. Treasury bonds were sold small, copper gained, and steel was off.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.20 versus 7.19 on Friday, February 9th

- CNY per EUR 7.75 versus 7.70 on Friday, February 9th

- Yield on 1-Day Government Bond 1.47% versus 1.57% on Friday, February 9th

- Yield on 10-Year Government Bond 2.43% versus 2.43% on Friday, February 9th

- Yield on 10-Year China Development Bank Bond 2.60% versus 2.62% on Friday, February 9th

- Copper Price +0.84%

- Steel Price -0.36%