Markets Show Resiliency

3 Min. Read Time

Key News

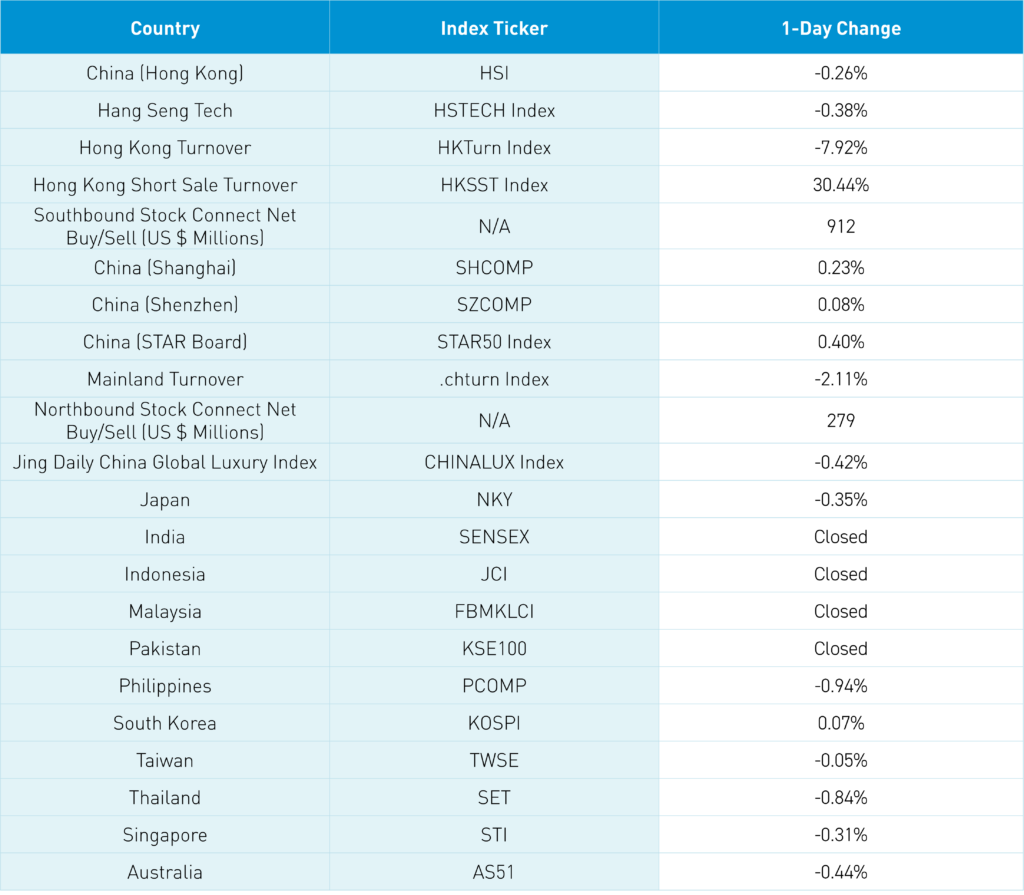

Asian equities were mixed overnight following a rough day in US stocks, which fell due to hot US inflation, providing further reinforcement to the higher-for-longer narrative. Meanwhile, India, Indonesia, Malaysia, and Pakistan were closed for Eid al-Fitr, which marks the end of Ramadan. The Asia Dollar Index fell -0.21% versus the US dollar overnight.

Unlike in the US, China’s March CPI was lower than expected. The index increased by +0.1% versus the estimate of 0.4% and February’s 0.7%. Based on prices from the Dalian exchange, hog futures were up +6.74% in March, which is why I had thought CPI would be higher. However, food, alcohol, and tobacco fell -1.4% along with transport/communications -1.3%. PPI was -2.8%, meeting expectations of -2.8% after February’s -2.7%. The bad news is good news narrative played out as investors expect more policy support in the face of weak domestic consumption and continued real estate concerns. In an indication the need for policy support is necessary, the Ministry of Commerce coordinated a meeting attended by multiple ministries on upgrades for consumer goods such as home appliances and vehicles.

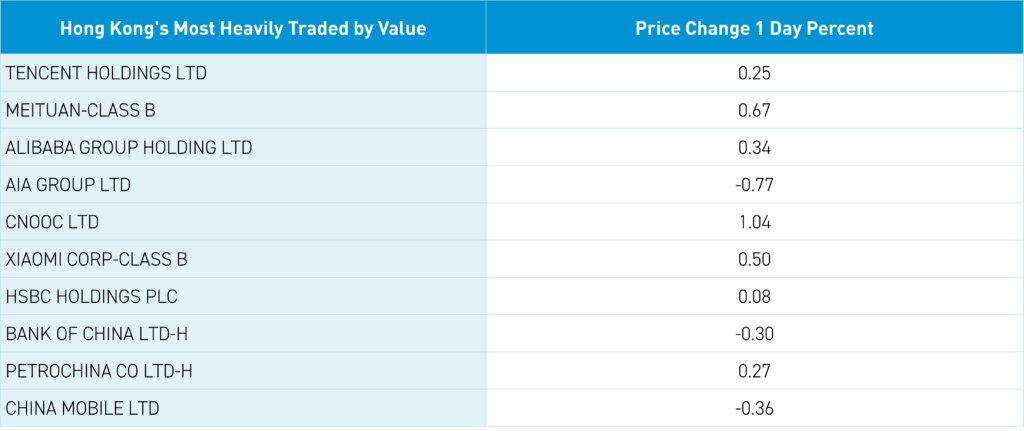

The Hang Seng Index, Shanghai, and Shenzhen all opened lower but managed to climb from intra-day lows in a positive sign. The Hang Seng and Hang Seng Tech indexes opened lower by -1.65% and -2.02%, respectively, but grinded higher to close only slightly lower. Hong Kong’s most heavily traded stocks by value were Tencent, which gained +0.25% after buying back 3.2 million shares today, Meituan, which gained +0.67% after buying back 3.85 million shares today, Alibaba, which gained +0.34% following Jack Ma’s pep talk message to employees, AIA, which fell -0.77%, and CNOOC, which gained +1.04%. Mainland investors bought a very healthy $912 million worth of Hong Kong-listed stocks and ETFs today as the Hong Kong Tracker ETF seeing a big inflow

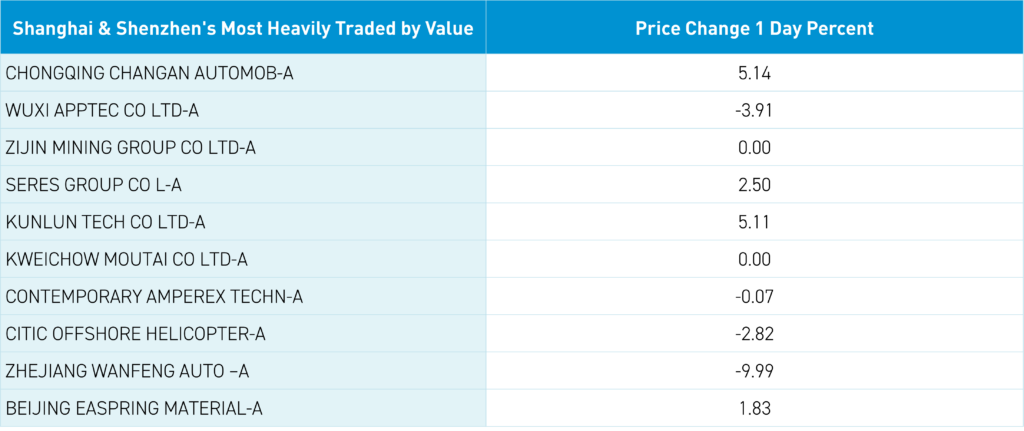

Shanghai and Shenzhen opened -0.45% and -0.73%, respectively, but grinded higher to close higher by +0.23% and +0.08%. The Mainland’s most heavily traded stock by value was Changan Automobile, which gained +5.14% on strong March auto sales.

The PBOC is clearly defending CNY versus the strong US dollar. Against a decent headwind, today’s market action is constructive as there were several negative headlines that historically would have weighed on sentiment. Real estate was off as SOE developer Vanke was downgraded to junk while a general manager was arrested.

The US government added six more companies to an entity list. Meanwhile headlines on US and Japan cooperation, the TikTok sale extension, and Taiwan’s former President meeting President Xi could be lumped in the negative bucket by some. However, as our trader friend Dave says, “market no care, you no care.”

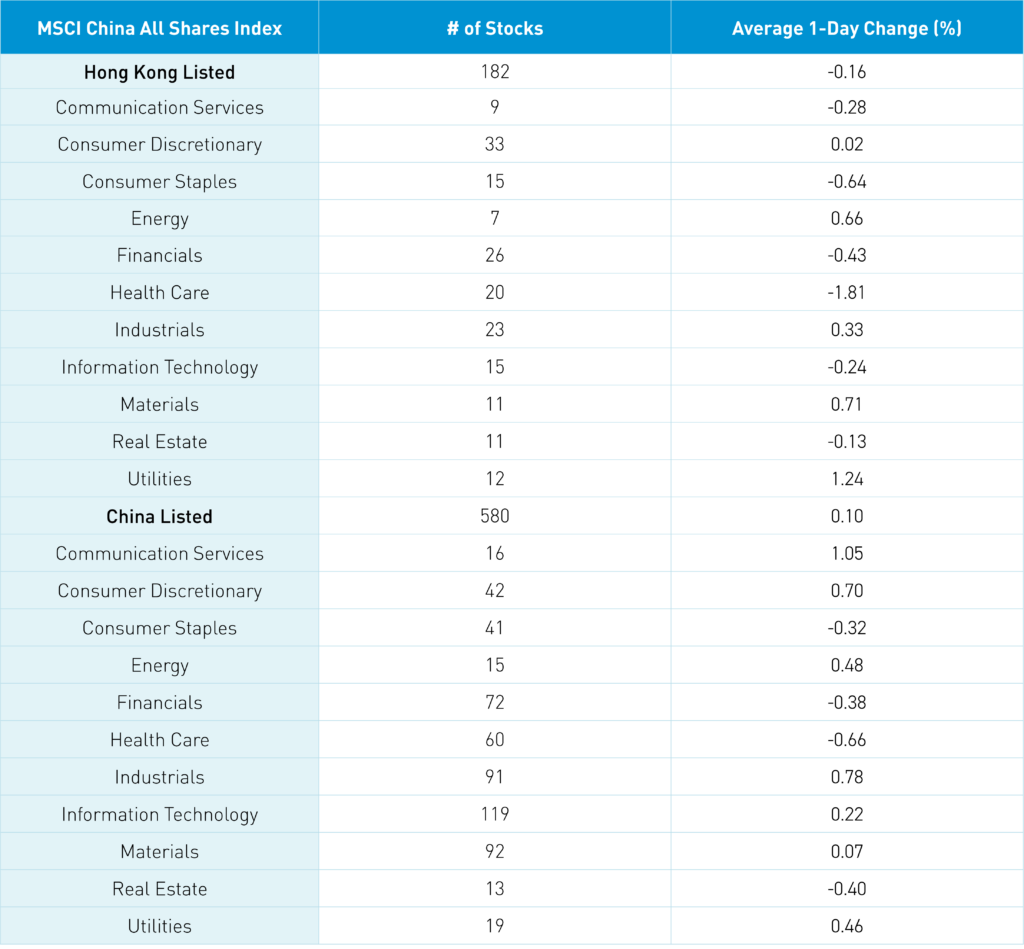

The Hang Seng and Hang Seng Tech fell -0.28% and -0.38%, respectively, on volume that decreased -7.92% from yesterday, which is 101% of the 1-year average. 187 stocks advanced, while 277 declined. Main Board short turnover increased by +30.44% from yesterday, which is 120% of the 1-year average, as 21% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). All factors were negative, as large caps and value stocks “outperformed” (i.e. fell less than) small caps and growth stocks. The top-performing sectors were Utilities, which gained +1.24%, Materials, which gained +0.71, and energy giant Phillips, which gained +0.66%. Meanwhile, Health Care fell -1.81%, Consumer Staples fell -0.64%, and Financials fell -0.43%. The top-performing subsectors were power equipment, cement, and new materials. Meanwhile, food/staples, semiconductors, and pharmaceuticals were among the worst-performing. Southbound Stock Connect volumes were moderate as Mainland investors bought a healthy $912 million worth of Hong Kong-listed stocks and ETFs, including the Hong Kong Tracker ETF, which saw a large net inflow, the Bank of China, and Meituan, which saw moderate inflows. Meanwhile, Semiconductor Manufacturing International (SMIC), Xiaomi, and Zhaojin Mining were small net sells.

Shanghai, Shenzhen, and STAR Board gained +0.23%, +0.08%, and +0.4% on volume that decreased -2.11% from yesterday, which is 94% of the 1-year average. 3,026 stocks advanced, while 1,836 declined. The value factor and small caps outperformed the growth factor and large caps. The top-performing sectors were Communication Services, which gained +1.05%, Industrials, which gained +0.79%, and Consumer Discretionary, which gained +0.7%. Meanwhile, Health Care fell -0.66%, Real Estate fell -0.39%, and Financials fell -0.37%. The top-performing subsectors were construction machinery, heavy machinery, and cultural media. Meanwhile, office supplies, agricultural products, and biotech were among the worst-performing. Northbound Stock Connect volumes were moderate as foreign investors bought a net $279 million worth of Mainland stocks, including Midea, a small net buy, Changan Automobile, and Gigadevice. Meanwhile, Kweichow Moutai, Foxconn, and CATL were net sells. CNY and the Asia Dollar Index were off versus the US dollar. Copper fell while steel gained.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.23 versus 7.23 yesterday

- CNY per EUR 7.76 versus 7.80 yesterday

- Yield on 10-Year Government Bond 2.29% versus 2.30% yesterday

- Yield on 10-Year China Development Bank Bond 2.42% versus 2.42% yesterday

- Copper Price -0.41%

- Steel Price +0.22%