Hong Kong & Mainland China Rally Rebounds on Trade Data & Home Buying Restrictions Cancelled

4 Min. Read Time

Key News

Asian equities were overall lower overnight as Mainland China and Hong Kong outperformed while South Korea, Australia, India, and the Philippines underperformed, falling by more than -1%. Meanwhile, Indonesia was closed for the Christian holiday Ascension Day.

April trade data was a catalyst, beating expectations with exports increasing by +1.5% versus an expected 1.3% and March’s -7.5%. Meanwhile, Imports increased by +8.4% versus expectations of +4.7% and March’s -1.9%. The data strongly indicates that the global economy is doing well, while the import data suggests China’s economy is recovering, albeit incrementally. The value of auto exports increased +24.9% to RMB 254 billion, though mobile phone export values fell -5.5% to RMB 266 billion.

Another catalyst was that major cities Xi’an (12.9 million residents, not including the Terracotta Army) and Hangzhou (11.9 million residents, GDP same size as Sweden) ending their housing purchase restrictions after the latter had them in place for eight years. The Xi’an government's release stated its decision was based on their desire to implement the State Council’s directive. We also saw similar moves last week, though we anticipate more to come.

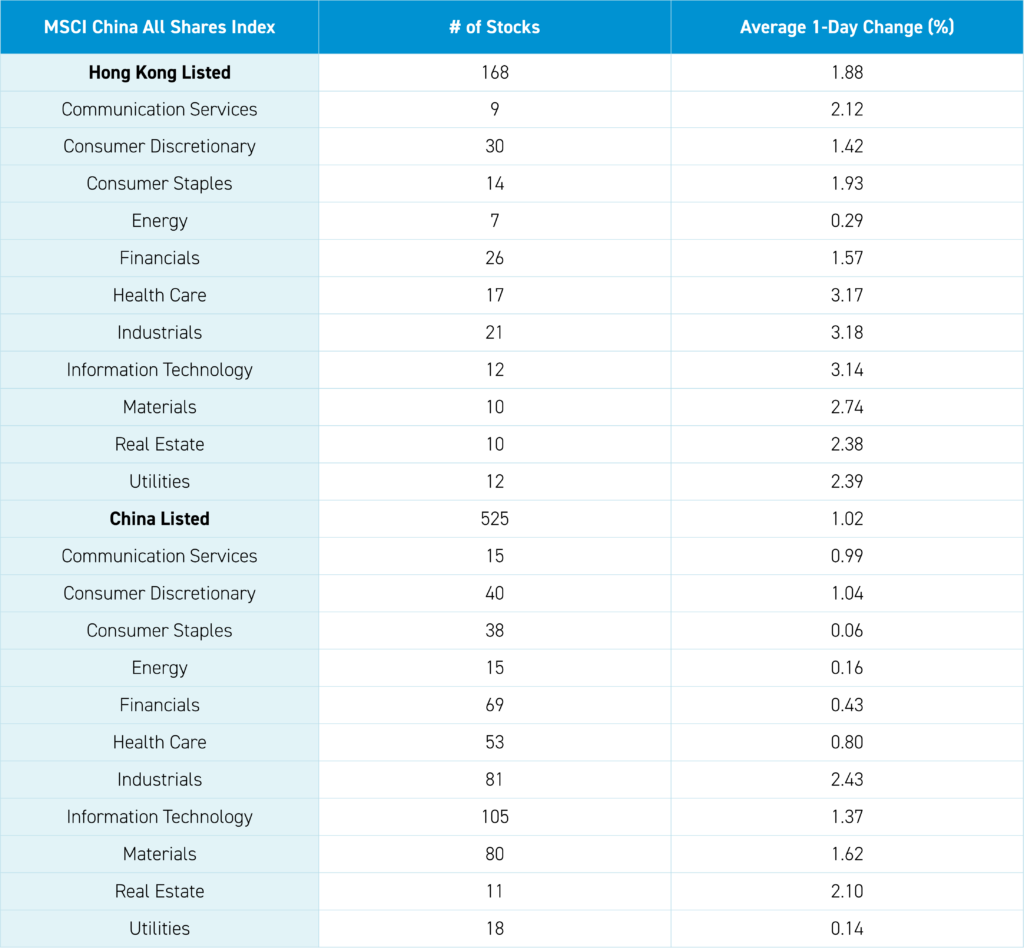

Real estate stocks gained +2.38% in Hong Kong and +2.1% in Mainland China, though the stocks trade like microcaps and are highly volatile and still at risk of dilution, which is why we prefer the bonds.

Bloomberg News reported that the 20% dividend tax paid by Chinese investors in Hong Kong could be waived by year-end, which would be another catalyst for Hong Kong stocks as Mainland banks' deposit rate is less than 2%.

It is worth noting that both Mainland China and Hong Kong were unaffected by some geopolitical saber rattling following the US Commerce Department’s ban on Nvidia and Qualcomm selling chips to Huawei and a US Senator calling to ban any China-made electric vehicles or parts. The latter is funny as the US auto industry depends highly on China's auto parts and inputs in US-made cars.

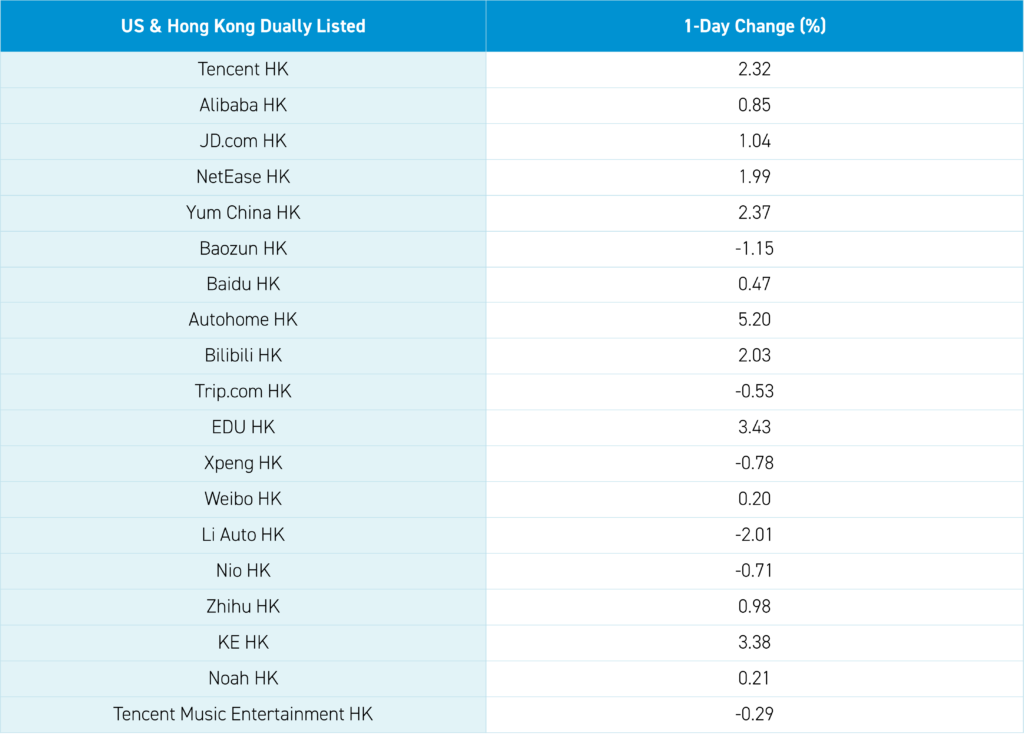

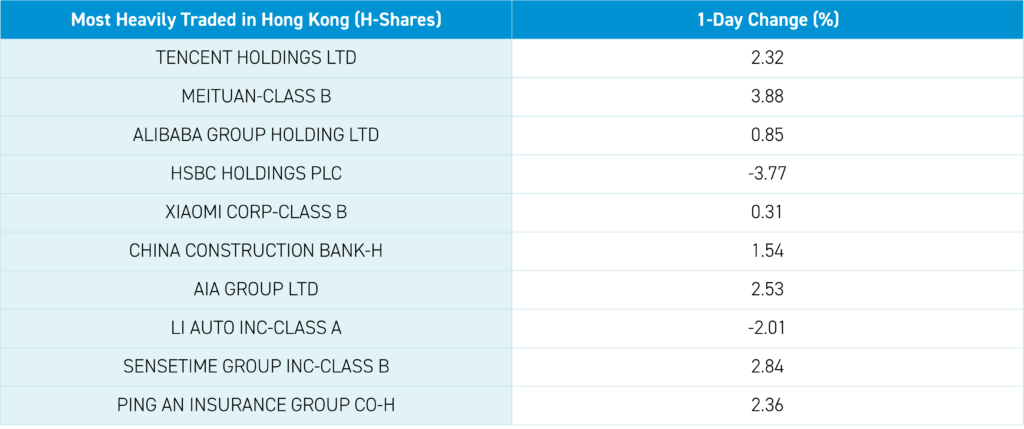

Hong Kong’s rally was extensive as advancers outnumbered decliners by 10 to 1 on good volume, though they were off from yesterday as both the Hang Seng and Hang Seng Tech indexes almost returned to their Monday levels following the vicious profit taking the last two days. Hong Kong’s most heavily traded stocks by value were Tencent, which gained +2.43%, Meituan, which gained +3.88%, Alibaba, which gained +0.85%, HSBC, which fell -0.44%, and Xiaomi, which gained +0.31%. The Hong Kong Tracker ETF was sold via Southbound Stock Connect in size, which is strange considering the dividend tax elimination news.

Shanghai and Shenzhen had a good day, with the former closing above Monday’s high in a positive sign—another very broad rally with advancers outpacing decliners 4 to 1 on good volumes. Foreign investors bought a healthy $1.109B of Mainland stocks via Northbound Stock Connect, bringing the year to date to $11.867B. Strong sign!

Did you notice any media attention around the US Chamber of Commerce’s 14th Annual China Business Conference in Washington, D.C., the last two days? Me neither.

I understand the skepticism about the China rally, having lived every down day since the market peaked in February 2021. Trust me when I say that writing this note was sometimes emotionally damaging! Following the strong Q1 GDP print, the export/import data indicates China’s economy is improving. Next week is significant, with Alibaba and Tencent reporting on Tuesday morning and JD.com and Baidu on Thursday morning. One naysayer's argument is driven by the growth in assets of EM Ex China ETFs versus EM ETFs, which include China.

I respectfully disagree with this analysis as the particular EM ETF that they chose for the comparison is in secular decline due to its expense ratio versus the three largest EM ETFs by AUM. Yes, EM Ex China AUM ETFs have grown, but they are still tiny compared to the AUM of the three biggest EM ETFs that include China. The three biggest EM ETFs have all seen shares outstanding continue to grow over the past five years. If China rallies, aren’t the owners of EM ex-China ETFs buyers of China at some point? Maybe they should be buying now!

The Hang Seng and the Hang Seng Tech indexes gained +1.22% and +1.95%, respectively, on volume that decreased -3.86% from yesterday, which is 124% of the 1-year average. 448 stocks advanced, while 46 declined. Main Board short turnover declined -22.07% from yesterday, which is 91% of the 1-year average, as 13% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). All factors were positive, as the growth factor and small caps outperformed. All sectors were positive, including Industrials, which gained +3.18%, Health Care, which gained +3.17%, and Technology, which gained +3.14%. The top-performing subsectors were semiconductors, transportation, and technical hardware. Meanwhile, food & beverage was the only negative subsector. Southbound Stock Connect volumes were light as Mainland investors sold a healthy -$533 million worth of Hong Kong stocks and ETFs, including China Mobile, ICBC, and Xiaomi, which were small net buys, while the Hong Kong Tracker ETF was a very large net sell, HSBC was a moderate net sell, and CNOOC was a small net sell.

Shanghai, Shenzhen, and the STAR Board gained +0.83%, +1.34%, and +2.26%, respectively, on volume that increased +4.12% from yesterday, which is 106% of the 1-year average. 4,097 stocks advanced, while 853 declined. All factors were positive, with the growth factor and small caps outperforming. All sectors were positive, as Industrials gained +2.42%, Real Estate gained +2.1%, and Materials gained +1.62%. The top-performing subsectors were marine industry, shipping, construction, and motorcycles. Meanwhile, telecom, oil & gas, and coal were among the worst-performing subsectors. Northbound Stock Connect volumes were moderate as foreign investors bought a healthy net $1.109B of Mainland stocks, including SANY, Wuxi AppTec, and CATL, which were small net buys. Meanwhile, Midea, Wanhua Chemical, and Yili were small net sells. CNY and the Asia Dollar Index were off slightly versus the US dollar. Treasury bond prices fell. Copper and steel were lower.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.22 versus 7.22 yesterday

- CNY per EUR 7.75 versus 7.76 yesterday

- Yield on 10-Year Government Bond 2.31% versus 2.29% yesterday

- Yield on 10-Year China Development Bank Bond 2.42% versus 2.39% yesterday

- Copper Price -0.51%

- Steel Price -0.76%