Tencent Beats While Alibaba Has Mixed Earnings, Though Stock Connect Is a Significant Catalyst

4 Min. Read Time

Tencent Earnings Review

Tencent’s earnings release for Q1 2024 was an outright beat on the big three metrics as online advertising rebounded +25% Year over year (YoY). Domestic China game revenue was down -2% YoY, though international games revenue was up by +34%, led by Supercell’s Brawl Stars. Hat tip to management for keeping expenses down, which drove an adjusted net income of +54% YoY and adjusted EPS of +57%. Chairman and CEO Ma “Pony” Huateng stated, “Executing on our commitment to return excess capital to shareholders, we stepped up our buyback plan and are on track to repurchase HKD100 billion of our shares in 2024, as well as paying an increased dividend…”. Almost $12.8B of shares to be bought in 2024 is impressive. I’ll have to find out what % of shares outstanding this equals. The company also stated investing in AI technology.

- Revenue increased by +6% YoY to RMB 159.5B ($22.5B) from RMB 149.9B, beating expectations of RMB 158B.

- Adjusted Net Income increased by +54% YoY to RMB 50.3B ($7.1B) from RMB 32.5B, beating expectations of RMB 42.8B.

- Adjusted EPS increased by +57% to RMB 5.26 from RMB 3.35, beating expectations of RMB 4.44

Alibaba Earnings Review

Alibaba’s earnings release was a topline revenue beat, though adjusted net income and adjusted EPS missed expectations. The income statement shows expenses rose incrementally YoY, but the bottom line miss culprit appears to be an “interest and investment income” swing from 2023’s RMB 10.496B to a loss of -RMB 5.702B. “Share of equity method investees” went from 2023’s RMB 446mm to a loss of -RMB 3.208B. I assume these are public and non-public investments that have fallen or are being written down. We’ll have to listen to the management call for further clarification. China E-commerce revenue increased by +4% YoY to RMB 93.216B ($12.91B), while international e-commerce gained +45% YoY to RMB 27.448B ($3.802B). Alibaba announced that it will file for Hong Kong to be its primary listing by August, paving the way for Southbound Stock Connect inclusion. This is a significant catalyst as Tencent has 9.3% of its shares held by Mainland investors via Southbound Stock Connect. I’ll have to do some analysis on the potential impact of Southbound Connect buying. The company announced it spent $4.8B buying 523mm Hong Kong shares (equivalent of 65mm ADRs), reducing their shares outstanding by 2.6%. Over the last year they reduced shares outstanding by 5.1% by spending $12.5B in buybacks. The company announced an annual dividend of $1 per ADR and a special one-time dividend of $0.66.

- Q4 2024 Revenue increased +7% YoY to RMB 221.874B ($30.729B) from RMB 208.2B, beating expectations of RMB 219B.

- Adjusted Net Income declined -11% to RMB 24.418B ($3.382B) from RMB 27.96B, missing expectations of RMB 26.237B.

- Adjusted EPS declined -5% to RMB 10.14 ($1.40) from RMB 10.71, missing expectations of RMB 10.43.

Key News

Asian equities were largely higher overnight.

Hong Kong and Mainland China were mixed despite the looming Biden tariffs on Chinese imports. The market’s resiliency is a good sign as that the Hang Seng Tech cleared recent resistance levels, similar to the Hang Seng Index recently. Concerning the EV tariff, 102.5% of 0% = 0%. The increased tariffs on semiconductors, cranes, batteries, steel, and aluminum should make inflation more sticky, which runs counterintuitively for a President trying to get reelected. My teenage daughter would remind Biden and team on tariffs and inflation with the Taylor Swift lyric: “It’s me, hi, I’m the problem, it's me”.

According to the New York Federal Reserve’s Liberty Street Economics blog post in May 2020, in 2017 US firms sold $376 billion worth of goods in China that were made in China and therefore don’t show up in export/import data, though those revenues flow back to the US. If you add those sales to US exports ($130B), there is no trade deficit!!! How do these people not know that? Apologies for the rant.

Premier Li commented that the proceeds from the issuance of RMB 2 trillion long-term special national bonds will support “implementation of major national strategies”. Issuing very long maturity/50 year bonds makes sense at such low interest rate levels, something Yellen should have done, in my opinion.

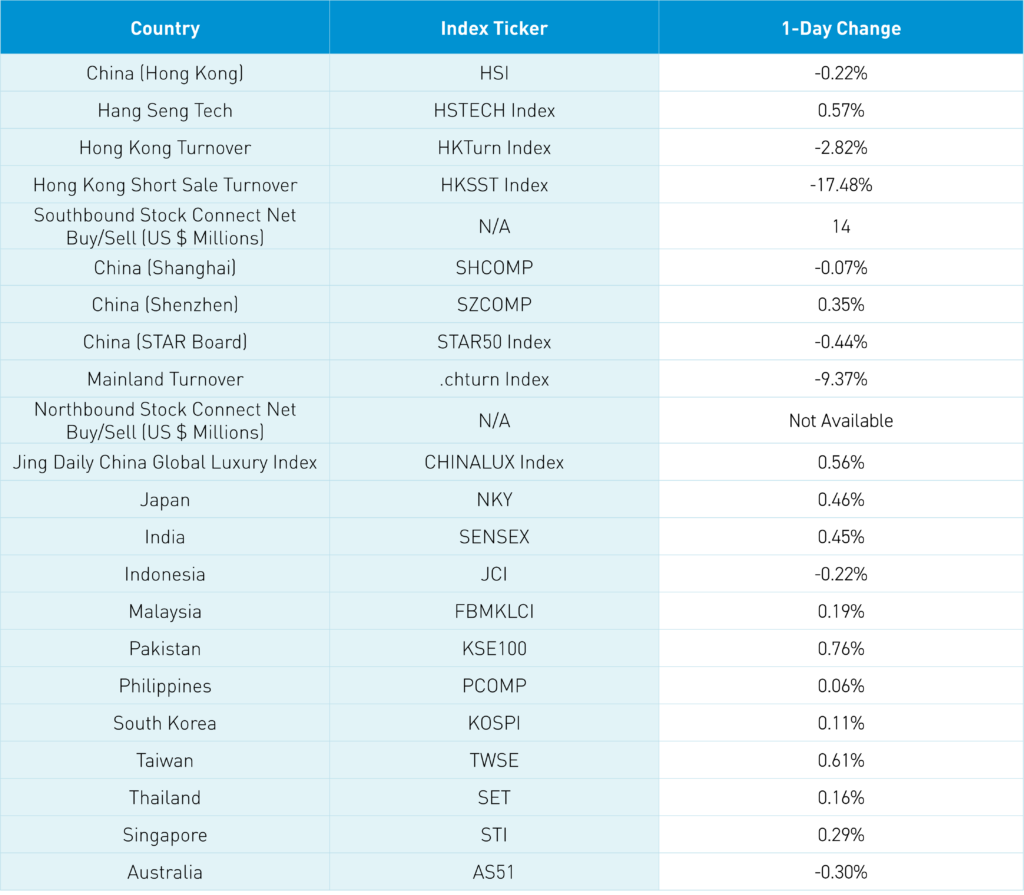

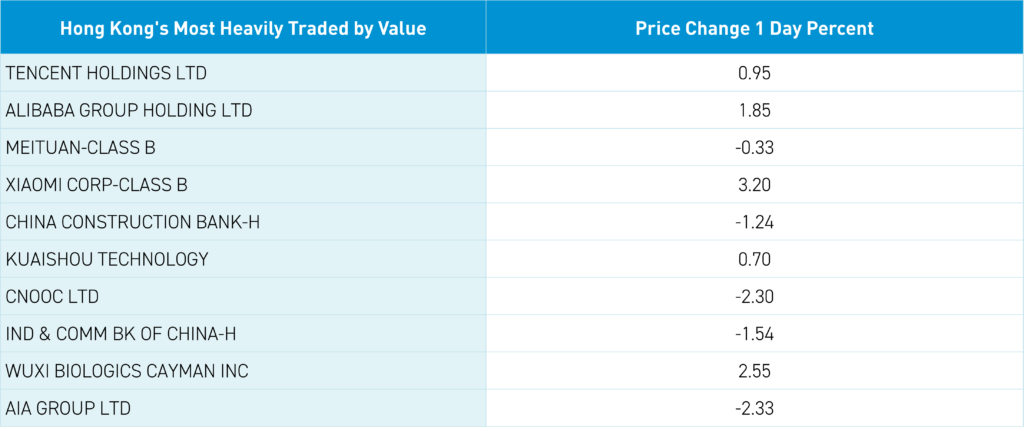

Hong Kong was quiet in advance of today’s Tencent and Alibaba financial results, as today’s most heavily traded stocks by value were Tencent, which gained +0.85%, Alibaba, which gained +1.85%, Meituan, which fell -0.33%, Xiaomi, which gained +3.2%, and China Construction Bank (CCB), which fell -1.25%. Southbound Stock Connect volume was very high, though net buying was only $14 million. Mainland China was mixed with growth names on the Shenzhen posting a small gain while Shanghai slipped. Northbound Stock Connect intra-day net buy/sell data is no longer available, though it is being disseminated after the close. Mainland investors appeared to be watching what foreign investors were doing and copying them. That could be a good thing or a bad thing based on their mood. The change has created a problem for my Excel data download. For the time being I can’t report on Northbound Flow data unfortunately. Apologies! Hong Kong is closed tomorrow for the Buddha’s birthday.

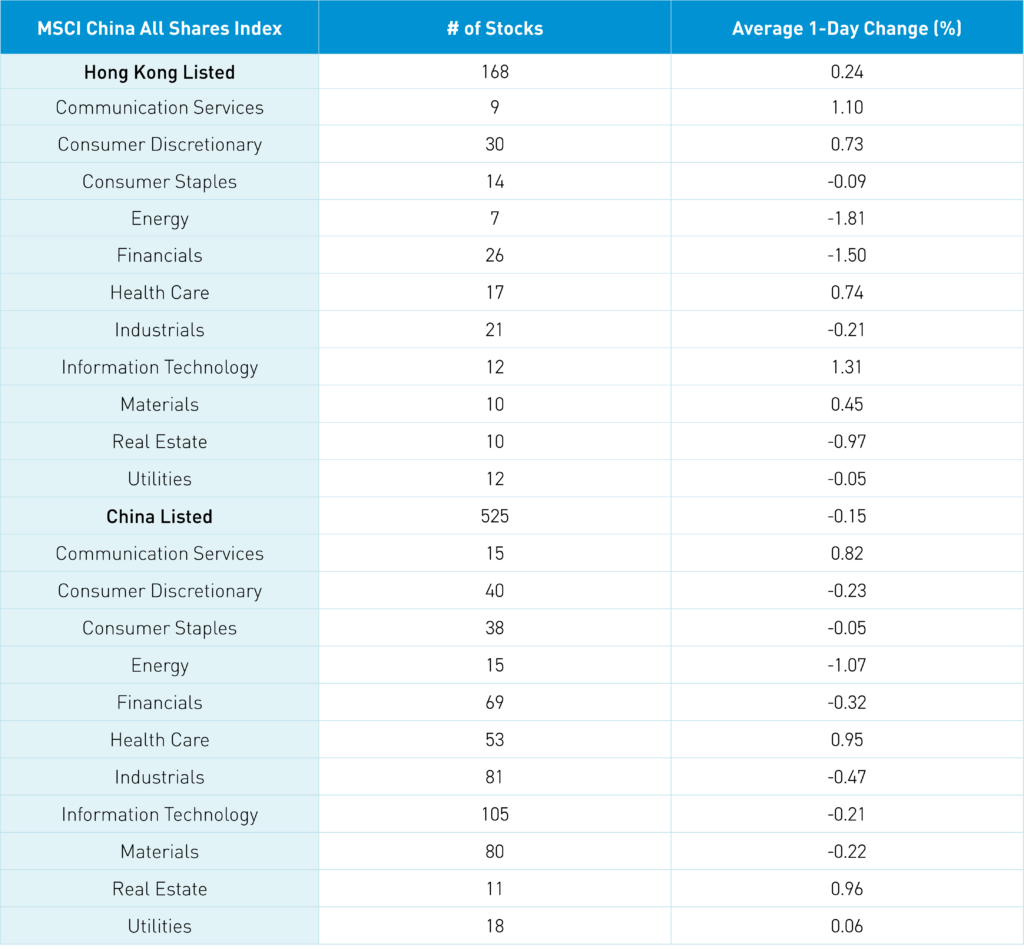

The Hang Seng and Hang Seng Tech indexes diverged to close -0.22% and +0.57%, respectively, on volume -2.82% from yesterday, which is 143% of the1-year average. 199 stocks advanced while 290 declined. Main Board short turnover fell -17.48% from yesterday, which is 110% of the 1-year average as 14% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). The value factor and large caps outperformed the growth factor and small caps. The top sectors were tech +1.31%, communication +1% and healthcare +0.74%, while energy -1.82%, financials -1.51%, and real estate -0.98% were the worst. The top sub-sectors were media, healthcare equipment, and technical hardware, while insurance, energy, and consumer services were the worst. Southbound Stock Connect volumes were very high as Mainland investors bought $14mm of Hong Kong stocks and ETFs

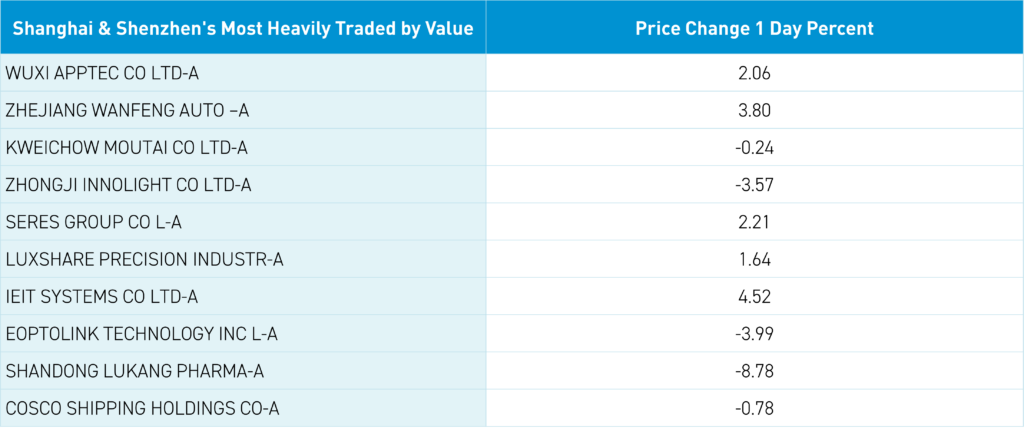

Shanghai, Shenzhen, and the STAR Board diverged to close -0.07%, +0.35%, and -0.44%, respectively, on volume that decreased -9.37% from yesterday, which is 97% of the 1-year average. 3,432 stocks advanced while 1,448 declined. The growth factor and small caps outpaced the value factor and large caps. The top-performing sectors were Real Estate, which gained +0.97%, Health Care, which gained +0.97%, and Communication Services, which gained +0.83%. Meanwhile, Energy fell -1.06%, Industrials fell -0.46%, and Financials fell -0.31%. The top-performing subsectors were motorcycles, education, and internet. Meanwhile, construction machinery, coal, and household appliances were among the worst-performing. Northbound Stock Connect volumes were moderate as foreign investors were net buyers. CNY and the Asia dollar index were off small versus the US dollar. The Treasury curve steepened. Copper gained while steel fell.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.23 versus 7.23 yesterday

- CNY per EUR 7.80 versus 7.81 yesterday

- Yield on 10-Year Government Bond 2.29% versus 2.29% yesterday

- Yield on 10-Year China Development Bank Bond 2.39% versus 2.39% yesterday

- Copper Price +1.45%

- Steel Price -0.16%