The PBOC (“Big Momma”) Releases Real Estate Policy Bazooka, Week in Review

4 Min. Read Time

Week in Review

- Asian equities were sharply higher this week, led by Hong Kong, Indonesia, and Taiwan, though Mainland China markets were flat.

- This week was a busy one for internet earnings as Tencent and JD.com beat estimates handily while Alibaba and Baidu reported mixed results.

- Real estate was also in focus this week as news of a government effort to purchase unsold apartments to stabilize prices led to gains in developer stocks.

- Inflation reports were further impacting markets this week as China reported higher-than-expected growth in consumer prices, a good sign for its economy, and the US’ softer-than-expected CPI print contributed to a risk-on atmosphere globally.

Friday's Key News

Asia ended the week higher as Mainland China and Hong Kong outperformed while South Korea was off.

It was an interesting session overnight. Hong Kong and Mainland China bounced around the room before slipping following April economic releases. This is despite Vice Premier He Lifeng’s comments on real estate policy support. Then, markets went absolutely vertical after the People’s Bank of China (PBOC), China’s central bank, announced three policies to support the real estate market.

The PBOC’s real estate three-pronged stimulus package involves: (1) providing RMB 300 billion ($41.5 billion) worth of loans to local governments to buy unsold apartments (really RMB 500 billion, assuming it represents 60% of the loan principal) at an interest rate of 1.75%, (2) lowering the minimum down payment for first-time home buyers’ mortgages to 15% and to 25% for second homes, (3) lowering the mortgage rate for first-time home buyers for loans of 5-years or less by 0.25% to 2.35% and to 2.85% for longer-term loans (2.78% and 3.33% for second-time home buyers).

This is the closest to the policy bazooka we’ve seen in addressing the multiple facets of real estate’s impact on China’s economy. Multiple agencies including the Ministry of Finance, the Ministry of Housing and Urban Development, and the Ministry of Natural Resources released statements around these top-down policy changes. The facets of economic impact are (1) depressed property developers creating a financial crisis (i.e. China’s Lehman moment though no one believes the government would allow a financial crisis to unfold right in front of them), (2) the lack of property development, which means fewer jobs, (3) fewer new apartments, which means less demand for home appliances, furnishings, etc., and (4) lower property prices, which have been weighing on household wealth and thereby domestic consumption (60% of China’s household wealth is tied to housing). This is a real step-up in policy. Yes, it is not a magic bullet that will suddenly solve the above issues, but it will help.

April new home prices declined -0.58% from March and existing home prices fell -0.94% from March.

Did you notice all the “buts” in Western media reporting on this topic? Foreign investor confidence in China, especially amongst US investors, is low, which explains the skepticism. Why bother when the Magnificent 7 goes up every day? That is true, until it doesn’t.

In China they call the PBOC “Big Momma” because you don’t mess with the PBOC. Investors in China and Asia will recognize that when the government pivots, you should too!

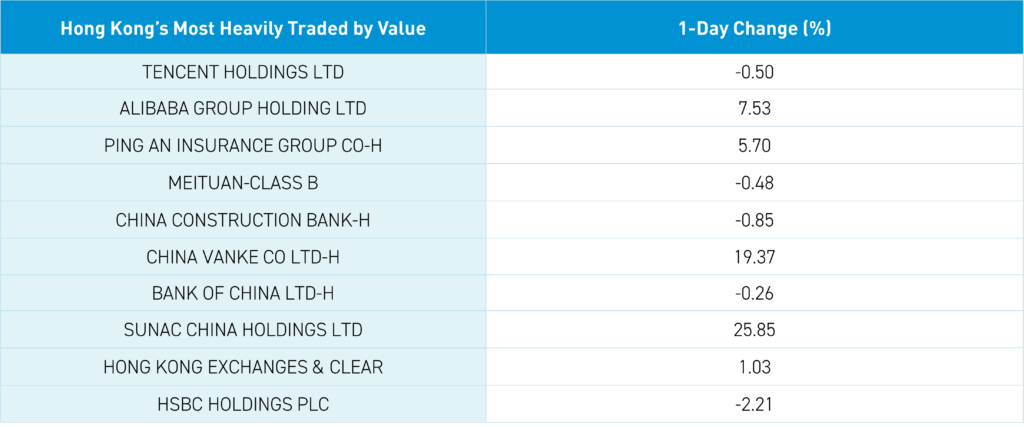

Real estate was the top-performing sector in Mainland China, where it gained +7.94%, and Hong Kong, where it gained +5.42%. Developer China Vanke gained +19.37% and Sunac gained +25.85%.

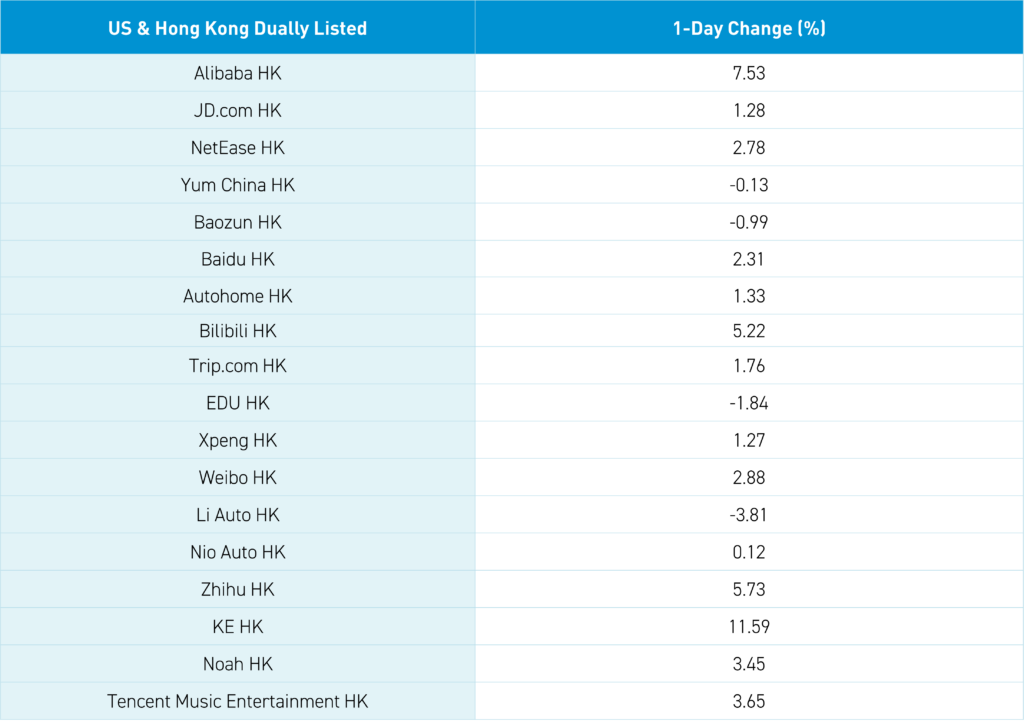

Knowing professional investors are underweight China, it is not surprising that trading desks were busy overnight. Think about all those emerging market funds that own Nvidia and Microsoft! Hong Kong trading volume was lower than yesterday, though still 178% of the 1-year average led by Tencent, which gained +0.36%, Alibaba, which gained +7.53% after short selling firm Citron re-recommended the stock, Ping An Insurance, which gained +5.7%, Meituan, which fell -0.48%, and China Construction Bank, which fell -0.85%. It is interesting that Tencent’s market capitalization is $476 billion versus Alibaba’s $213 billion, though I suspect that Alibaba will receive some TLC from mainland investors once added to Southbound Stock Connect this fall.

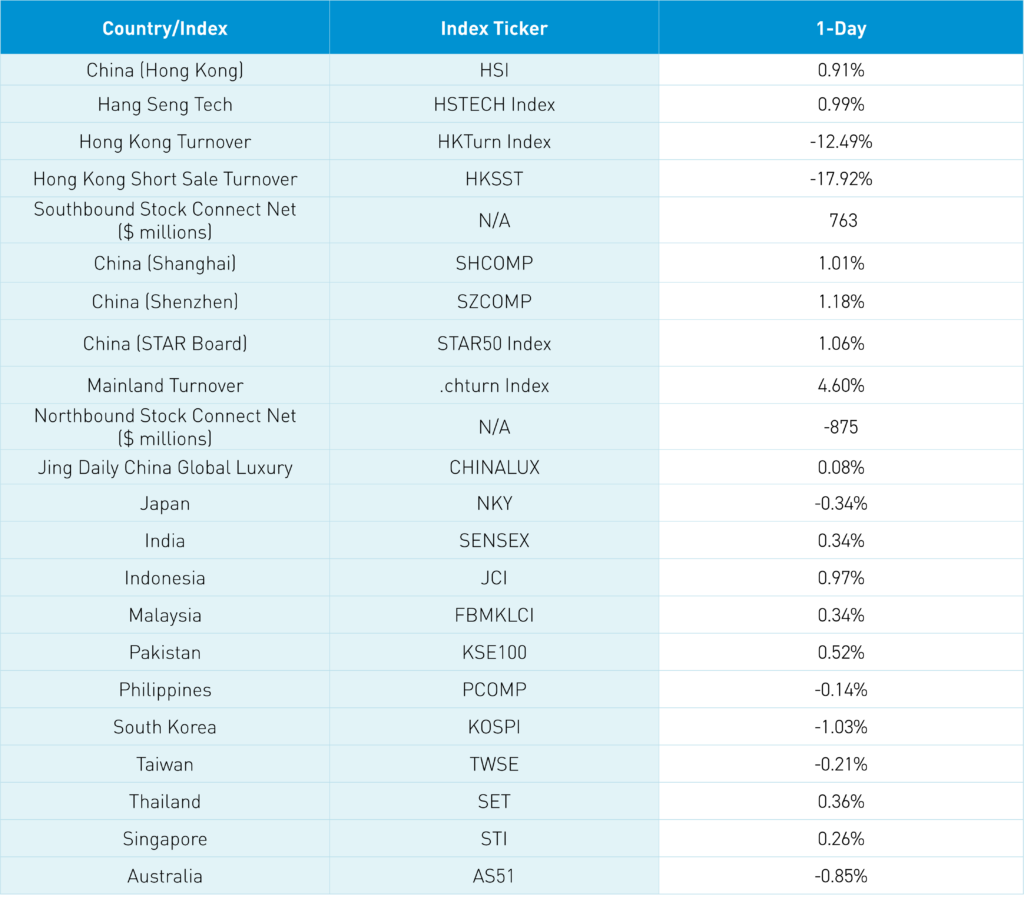

The Hang Seng closed above 19,500 as Mainland China outperformed Hong Kong.

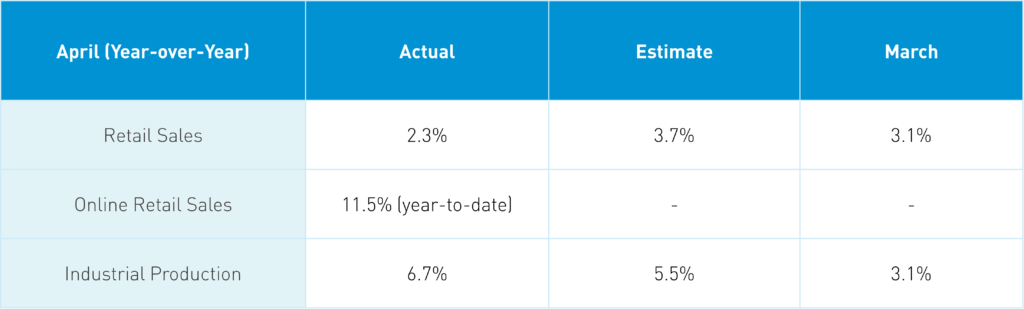

In last night’s economic release, industrial production was stronger-than-expected though retail sales surprisingly came in lower. Meanwhile, online retail sales were relatively strong. Property investment was unsurprisingly lower, along with property sales. Remember our trading buddy Dave’s saying – “if market no care, you no care”.

I recommend checking out Charlie Munger’s interview on the Acquired podcast. He had interesting comments on investing in China, including a discussion of Berkshire Hathaway’s BYD investment.

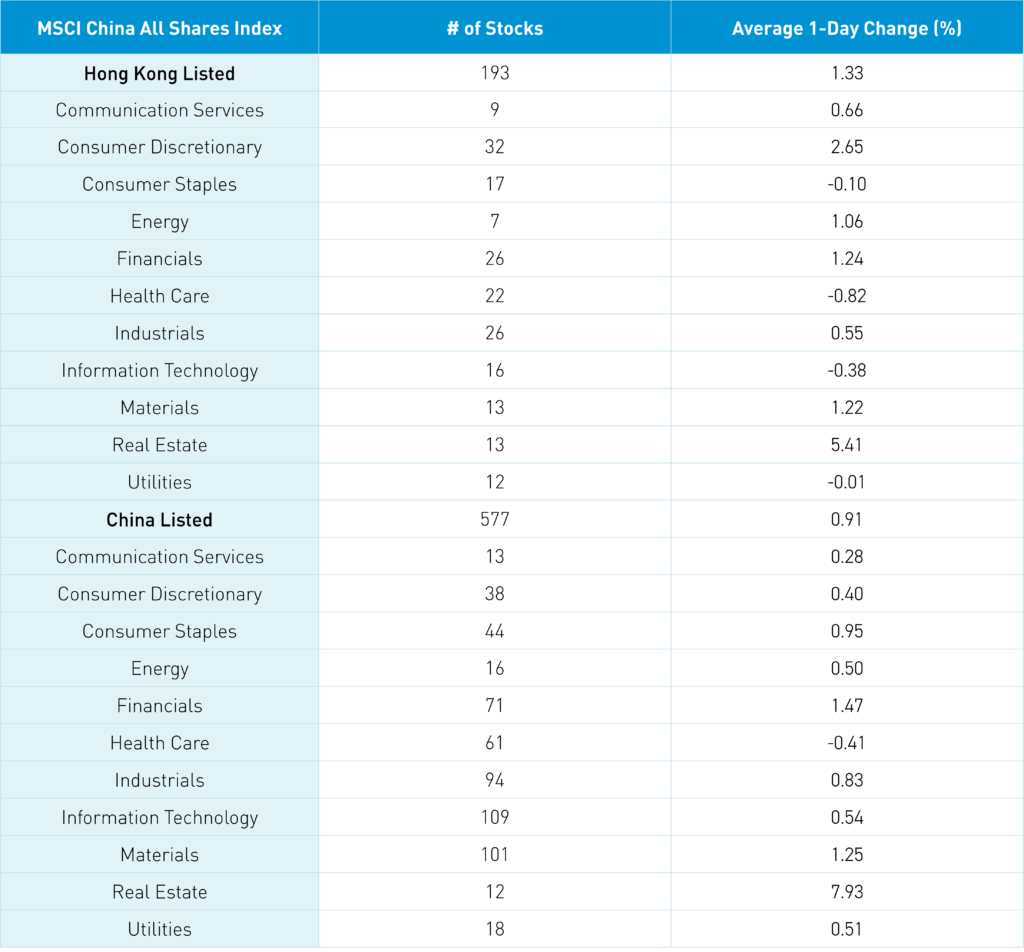

The Hang Seng and Hang Seng Tech indexes gained +0.91% and Wayne Gretzky +0.99%, respectively, on volume that decreased -12.49% from yesterday, which is 178% of the 1-year average. 333 stocks advanced while 150 declined. Main Board short turnover declined -17.92% from yesterday, which is 139% of the 1-year average, as 14% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ hedging). All factors were positive as value and large caps outperformed. The top-performing sectors were Real Estate, which gained +5.41%, Consumer Discretionary, which gained +2.65%, and Financials, which gained +1.24%. Meanwhile, Health Care fell -0.82%, Technology fell -0.38%, and Consumer Staples fell -0.1%. The top-performing subsectors were real estate services, insurance, and retail. Meanwhile household/personal products, semiconductors, and pharmaceuticals were among the worst-performing. Southbound Stock Connect volumes were high, almost twice the 1-year average as Mainland investors bought a net $763 million worth of Hong Kong-listed stocks and ETFs, including Bank of China, which was a large net buy, Tencent, and China Construction Bank.

Shanghai, Shenzhen, and the STAR Board gained +1.01%, +1.18%, and +1.06%, respectively, on volume that increased +4.6% from yesterday, which is 104% of the 1-year average. 3,295 stocks advanced while 1,585 stocks declined. All factors were positive as value and large caps outperformed. The top-performing sectors were Real Estate, which gained +7.93%, Financials, which gained +1.48%, and Materials, which gained +1.26%. Meanwhile, Health Care was the only negative sector, falling -0.41%. The top-performing subsectors were real estate, insurance, and chemical fibers, while motorcycles, power generation equipment, and household appliances were among the worst-performing subsectors. Northbound Stock Connect volumes were average as foreign investors sold a net -$875 million worth of Mainland stocks. CNY was flat and the Asia Dollar Index was lower versus the US dollar. Treasury bonds rallied. Copper and steel were both up 1.17%, which I have never seen before.

Last Night’s Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.22 versus 7.22 yesterday

- CNY per EUR 7.85 versus 7.85 yesterday

- Yield on 1-Day Government Bond 1.35% versus 1.36% yesterday

- Yield on 10-Year Government Bond 2.31% versus 2.31% yesterday

- Yield on 10-Year China Development Bank Bond 2.41% versus 2.42% yesterday

- Copper Price +1.17%

- Steel Price +1.17%