Hong Kong & Mainland China Climb The Great Wall of Skepticism

3 Min. Read Time

Key News

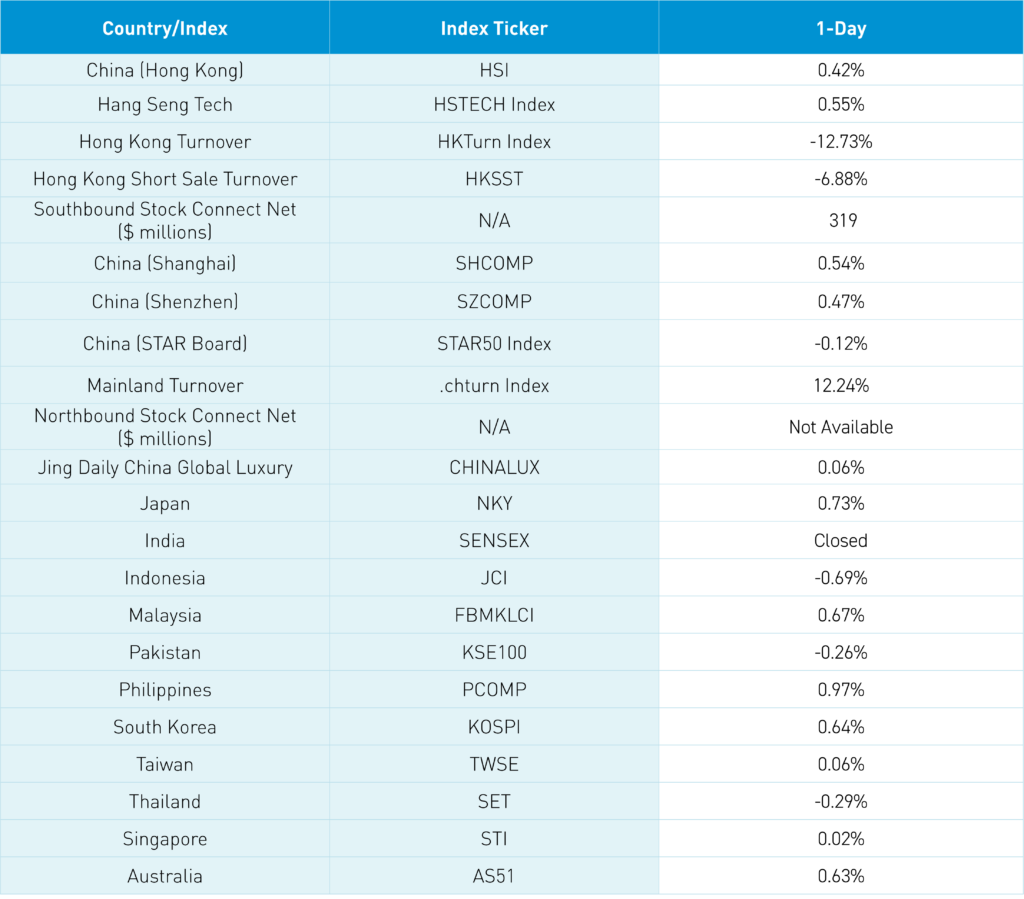

Asian equities were largely higher despite the US dollar’s strength overnight though India was on holiday for election day.

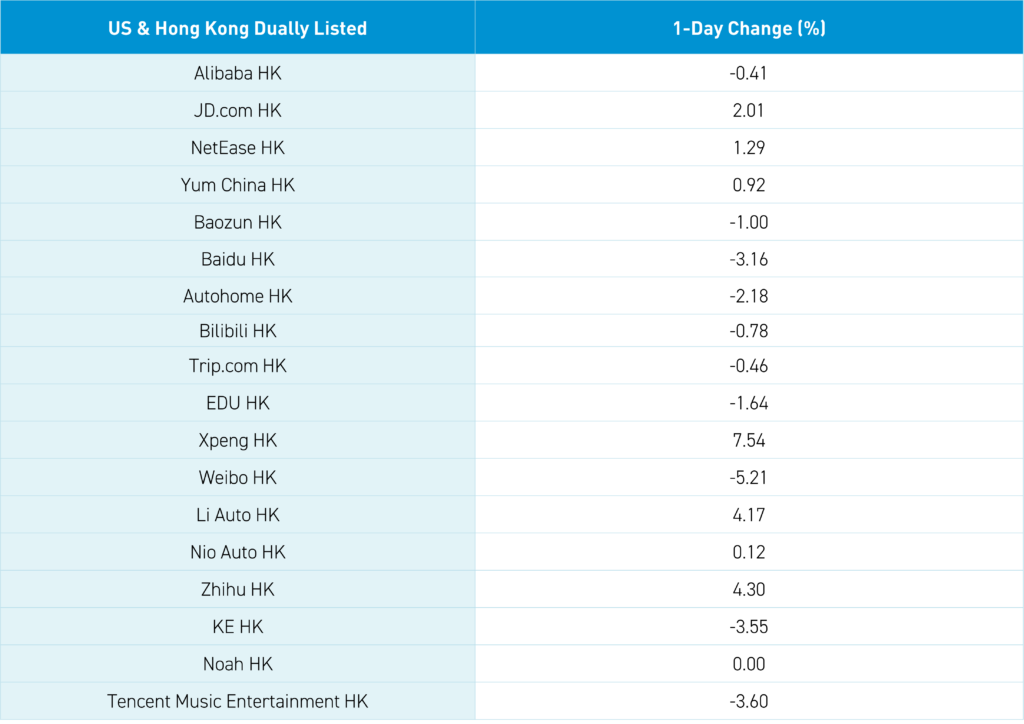

It was a fairly quiet night from a news perspective. Hong Kong grinded higher, Shanghai closed above the 3,150 level, and Shenzhen closed at just below the 1,800 level. Hong Kong did not rise as much as US-listed China stocks did on Friday, which could lead to a pullback today here in the US.

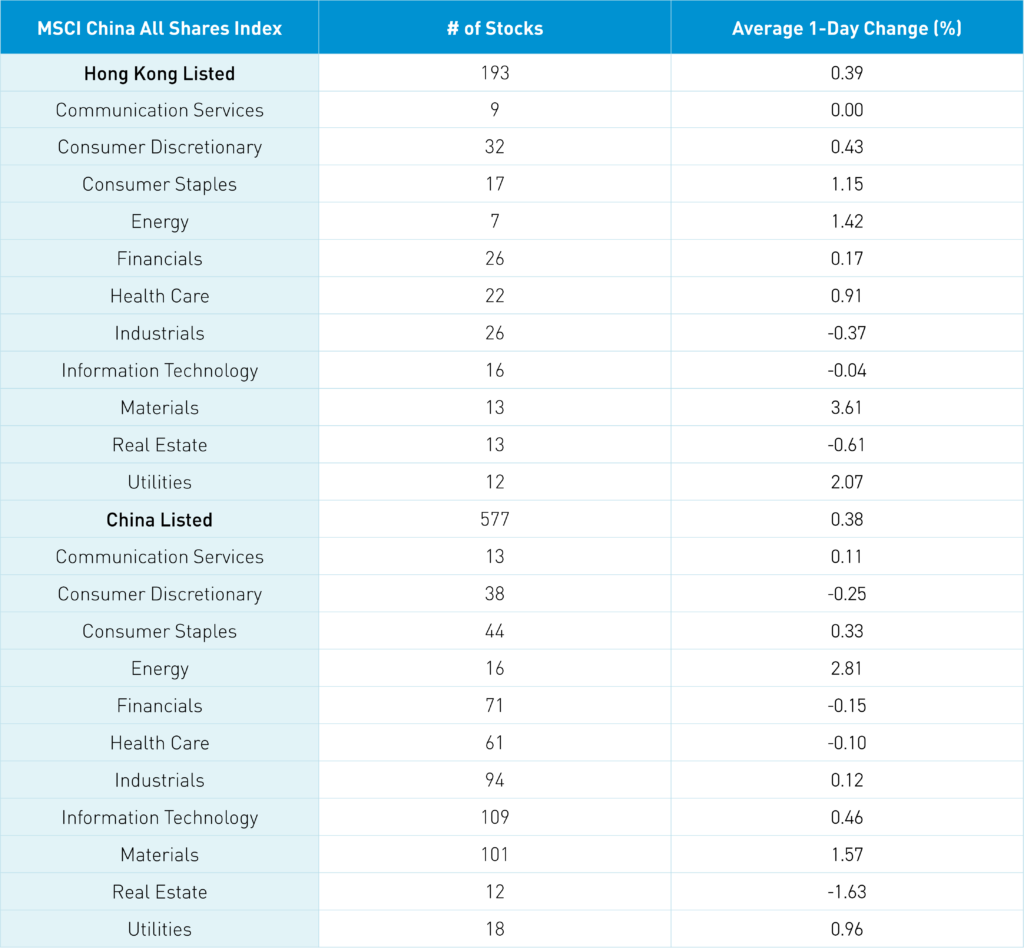

Real estate stocks were hit with profit-taking after Friday’s very strong performance The sector fell -1.64% in Mailand China and -0.63% in Hong Kong.

Have you noticed the skepticism around the new policies announced Friday? 100% of the policies do not unleash rainbows and unicorns, though the key point is the government’s awareness of the issue and ability to direct policies to support it, as this won’t be the last policy announcement. Chinese financial media noted Shenzhen’s government implementation of the new policies led to strong apartment sales over the weekend. Chinese media also noted that Beijing apartment sales were strong with more than 2,000 apartments sold.

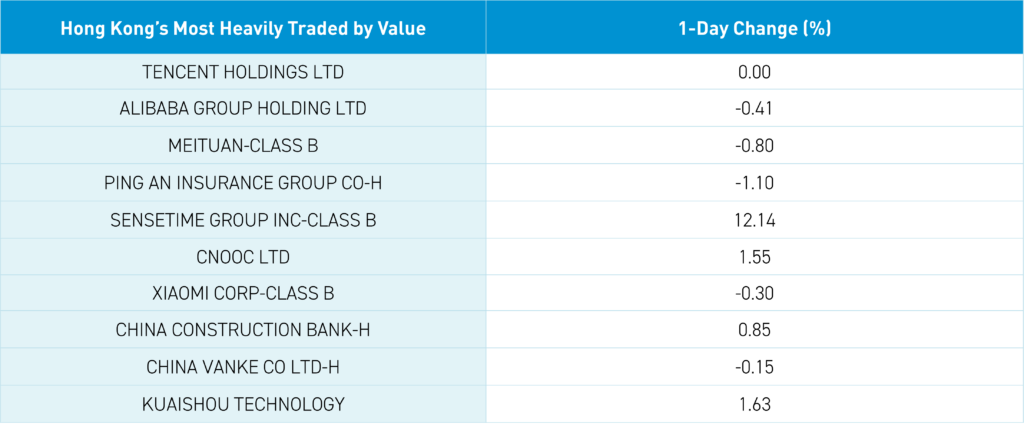

Hong Kong’s most heavily traded stocks by value were Tencent, which was flat, Alibaba, which fell -0.41%, Meituan, which fell -0.8%, Ping An Insurance, which fell -1.1%, and Sense Time, which gained +12.14%. Mainland investors bought a net $319 million worth of Mainland stocks today via Southbound Stock Connect, bringing the year-to-date total to $31.4 billion versus 2023’s $40 billion worth of net buying.

The 1 and 5-Year Loan Prime Rates were left unchanged at 3.45% and 3.95%, respectively.

Didi will eliminate the role of President. President Jean Liu will step down from the role and board, though intends to remain with the company.

All told, the market continues to climb the “Great Wall of Skepticism” …

Tariffs have become the new buzz word with politicians! The last time tariffs were this popular in Washington, DC was 1929. That really makes you think. The similarities between the 1920s and the 2020s are a little eerie: A pandemic, the “Roaring Twenties”, a strong stock market, and a rise in protectionism and isolationism. Let’s hope history does not repeat itself so precisely!

The Hang Seng and Hang Seng Tech indexes gained +0.42% and +0.55%, respectively, on volume that declined -12.73% from Friday, which is 155% of the 1-year average. 293 stocks advanced while 188 declined. Main Board short turnover declined -6.88% from Friday, which is 129% of the 1-year average, as 15% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). All factors were positive as growth and small caps outperformed value and large caps. The top-performing sectors were Materials, which gained +3.61%, Utilities, which gained +2.06%, and Energy, which gained +1.42%. Meanwhile, the worst-performing sectors were Real Estate, which fell -0.61%, Industrials, which fell fell -0.38%, and Technology, which fell -0.04%. The top-performing subsectors were materials and autos & transportation. Meanwhile, media, food & beverage, and telecom were among the worst-performing subsectors. Southbound Stock Connect volumes were very high, at 1.5X the 1-year average, as Mainland investors bought a net $319 million worth of Hong Kong-listed stocks and ETFs, including the Bank of China and Sunac, which were moderate net buys, and China Construction Bank, which was a small net buy. Meanwhile, Xiaomi was a moderate net sell and China Mobile was a moderate/light net sell.

Shanghai, Shenzhen, and the STAR Board diverged to close +0.54%, +0.47%, and -0.12%, respectively, on volume that increased +12.24% from Friday, which is 117% of the 1-year average. 2,610 stocks advanced while 2,262 declined. All factors were positive as growth and large caps outpaced value and small caps. The top-performing sectors were Energy, which gained +2.81%, Materials, which gained +1.57%, and Utilities, which gained +0.96% Meanwhile, the worst-performing sectors were Real Estate, which fell -1.63%, Consumer Discretionary, which fell -0.25%, and Financials, which fell -0.16%. The top-performing subsectors were precious metals, energy equipment, and coal. Meanwhile, household products, forest industry, and household appliances were among the worst-performing. Northbound Stock Connect volumes were moderate as CATL, Wuliangye, and CITS were moderate net buys. Meanwhile, Nari-Tech was a moderate net sell along with Zijin Mining and TFC. CNY and the Asia Dollar Index were lower versus the US dollar. Treasury bonds fell. Copper ripped higher while steel posted a small gain.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.23 versus 7.22 Friday

- CNY per EUR 7.86 versus 7.86 Friday

- Yield on 1-Day Government Bond 1.30% versus 1.35% Friday

- Yield on 10-Year Government Bond 2.32% versus 2.31% Friday

- Yield on 10-Year China Development Bank Bond 2.41% versus 2.41% Friday

- Copper Price +4.14%

- Steel Price +0.54%