Apple’s Alibaba 618 Sales Off to a Strong Start

2 Min. Read Time

Key News

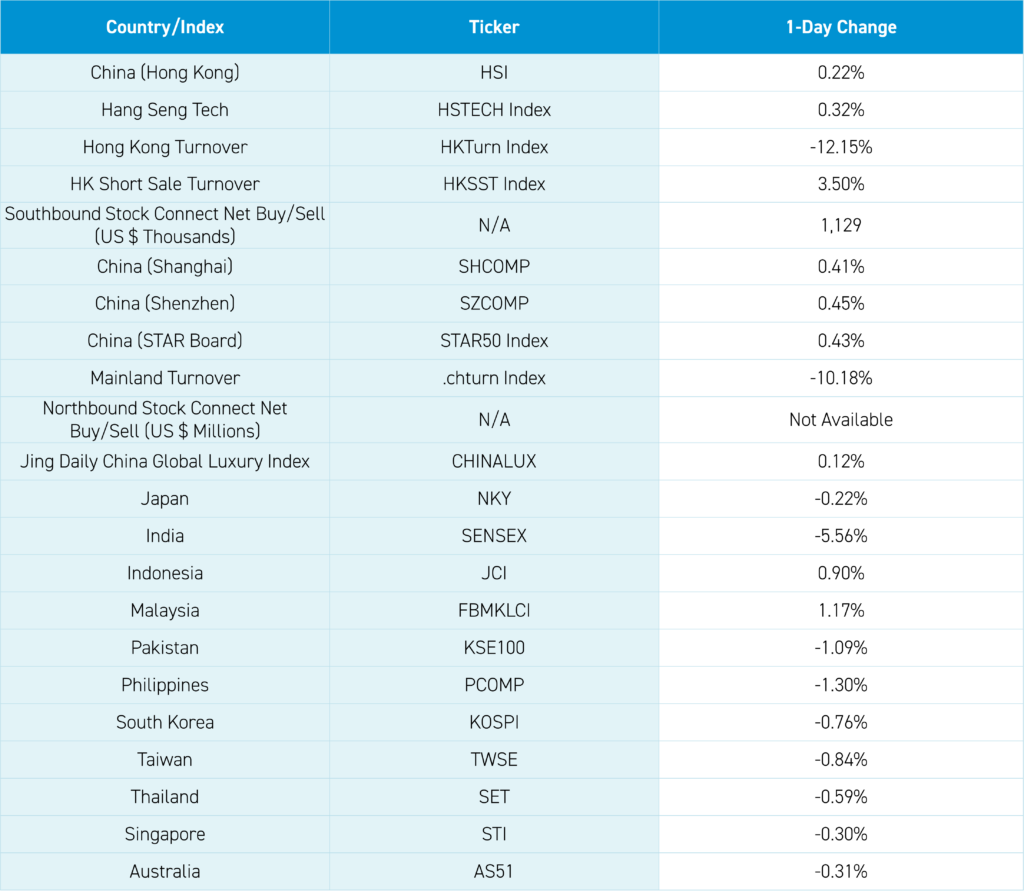

Asian equities were mixed as India was off, sliding -6% as President Modi did not achieve the landslide win that was expected. Hong Kong and China rewarded my visit with another day, which may require extending my stay.

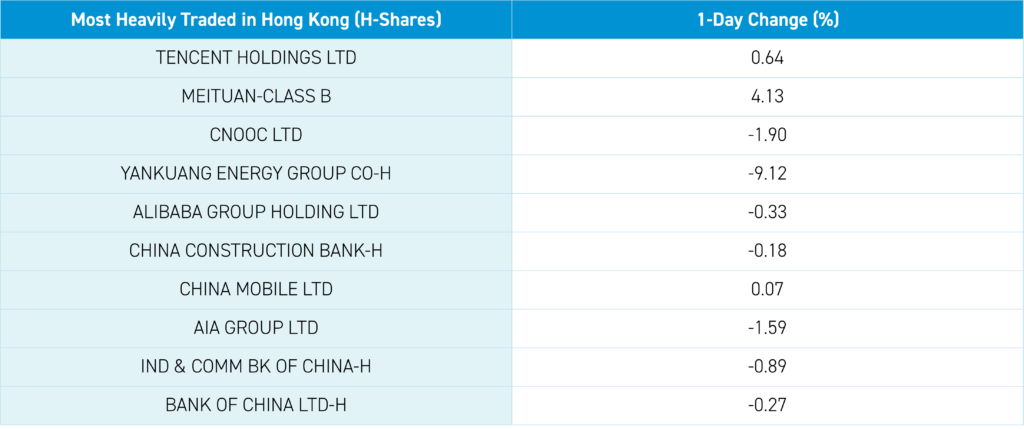

Hong Kong bounced around the room, led by the most heavily traded by value, Tencent +0.64%, Meituan +4.13%, CNOOC -1.9%, Yankuang Energy -9.12% after issuing more shares, Alibaba HK -0.33% despite initial solid results from the start of the 618 sales event. In the first hour of sales, Alibaba announced that 28 brands on Tmall sold more than RMB 100m ($13.8mm) of goods with Apple doing more than $200mm. Trip.com announced it will issue a $1.3B convertible to fund a $400mm share buyback with other proceeds to grow the company. Huge net buy via Southbound Stock, with Mainland investors buying a healthy $1.129B of stock.

It's relatively quiet from a news perspective, with real estate having a good day, +3.08% in Hong Kong and +2% in China on improved Shanghai sales figures. The CSRC announced their next capital market policy and reform update will take place on June 19th and 20th during the Lujiazui Forum. The National Energy Association announced plans for further solar projects, including in the Gobi Desert, leading to a good day in green tech, including EV, EV battery, and solar names. Mainland China grinded higher as 15 of the 17 top stocks by value traded higher—no sign of the National Team based on normal volumes in their favorite ETFs.

As mentioned yesterday, local Hong Kong sentiment has improved compared to my December 2023 and January Singapore trips. While there is a healthy dose of interest in US semis and AI here, there is awareness of government policy support for real estate. With US stocks in full FOMO mode, many global investors are likely unaware of improvements to China’s economy and corporate shareholder-friendly moves. For example, I recently received a US-based strategist’s market update. I was surprised at the little commentary on the post-January China rally. After searching the eleven-page PDF, the word “China” was mentioned three times, compared to “India” 10 times and “Japan” 29 times! China's pain trade is higher, IMO!

The Hang Seng and Hang Seng Tech gained +0.22% and +032% on volume -12.15% from yesterday, 114% of the 1-year average. 336 stocks advanced, while 147 declined. Main Board short turnover increased +3.5% from yesterday, 93% of the 1-year average, as 14% of turnover was short turnover (Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). Value and small caps outpaced growth and large caps. The top sectors were healthcare +3.47%, real estate +3.08%, and utilities +1.53%, while energy -2.05% and tech -0.26%. The top sub-sectors were pharmaceuticals, consumer durables, and real estate, while energy, media, and auto were the worst. Southbound Stock Connect volumes were moderate/high as Mainland investors bought a healthy $1.129B of Hong Kong stocks and ETFs with Tencent and China Mobile moderate/large net buys.

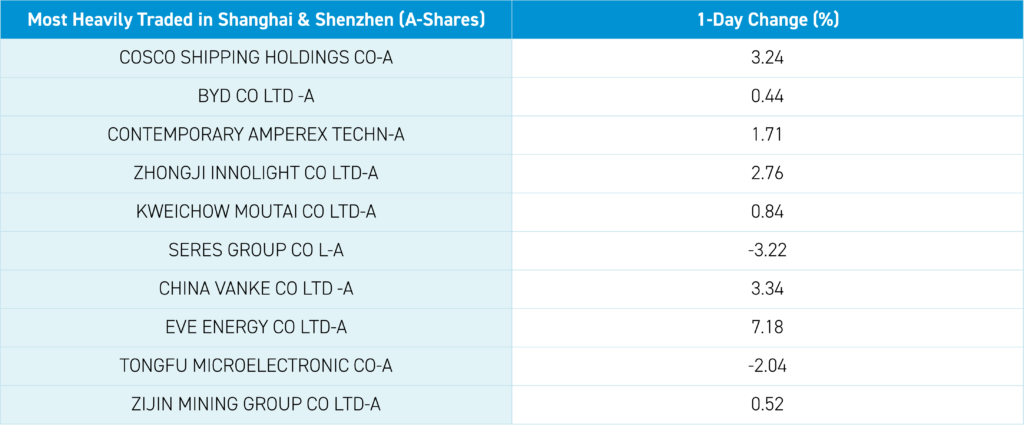

Shanghai, Shenzhen, and STAR Board gained +0.41%, +0.45%, and +0.43% on volume -10.18% from yesterday, 88% of the 1-year average. 1,665 stocks advanced while 3,283 declined. All factors were positive with growth and small caps outpacing value and large caps. Top sectors were real estate +2%, industrials +1.94% and healthcare +1.64% while energy -1.55%. Top sub-sectors were power generation equipment, office supplies, and catering/tourism while education, coal and leisure products were the worst. Northbound Stock Connect volumes were moderate with BYD, CATL and Cits small net buys while Cosco Shipping, Midea and Inovance were small net sells. CNY and the Asia dollar index were off very small versus the US dollar. Treasuries were flat. Copper gained while steel fell.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.24 versus 7.24 yesterday

- CNY per EUR 7.87 versus 7.85 yesterday

- Yield on 10-Year Government Bond 2.28% versus 2.28% yesterday

- Yield on 10-Year China Development Bank Bond 2.40% versus 2.40% yesterday

- Copper Price +0.40%

- Steel Price -0.60%