Offshore Goes Risk Off As Exports Beat, Week in Review

2 Min. Read Time

Week in Review

- Asian equities had a choppy week of trading on better-than-expected economic data coming out of China and, at the same time, more perceived geopolitical risks from the US.

- The Caixin Manufacturing and Services PMIs both beat estimates for May while China reported better-than-expected export growth year-over-year.

- E-Commerce and local services giant Meituan beat estimates on its top and bottom lines in the fourth quarter, according to its earnings report this week.

- Alibaba's 6.18 shopping festival kicked off this week as 28 brands did $14 million in promotional sales in the first days of the festival.

Key News

Asian equities were mixed overnight as Mainland China markets were up slightly while Hong Kong was lower. Markets were awaiting US non-farm payrolls, which were higher than expected, causing the increased hopes of rate cuts to lose steam.

There were some consternations about congressional proposals to limit purchases of batteries from CATL, the world’s largest battery maker. This weighed on the electric vehicle ecosystem. We believe this is mostly bark, with little bite to come. Ford uses CATL’s battery technology already in many of its new electric models. The political power of Detroit automakers will likely keep any resulting, actual legislation relatively light.

China’s exports increased +7.6% versus an expected +5.7% year over year in May. However, this beat failed to lift markets overnight. I can say that being in China currently and riding around in many beautiful BYD-made cars makes me understand the attractiveness of China’s vehicle exports. Nonetheless, domestic consumption needs to rise alongside exports.

Regional banks in Guangdong and Guangxi provinces are said to have significantly lowered the mortgage rates on offer to help bolster demand for real estate.

The clean energy ecosystem was higher on news that several government agencies, including the National Reform & Development Commission (NDRC) will conduct new research on wind and solar power. Notably, these new research efforts are focusing on more remote provinces, such as Inner Mongolia, expanding the breadth of China's industrial planning around renewable energy.

Indian markets sold off this week as the ruling, reform-focused, and market-friendly BJP party failed to retain its majority in the legislature. Emerging Markets (EM) investors may start to take profits in India and rotate into other EMs. China could be a beneficiary of this rotation, as we have mentioned previously. The political headwind only adds pressure on Indian stocks that are already highly valued, relative to their history. We shall see where the flows end up!

Meituan was lower overnight, likely on profit taking after a solid earnings beat yesterday.

Value factors outpaced growth factors by wide margins in both Hong Kong and Mainland China overnight.

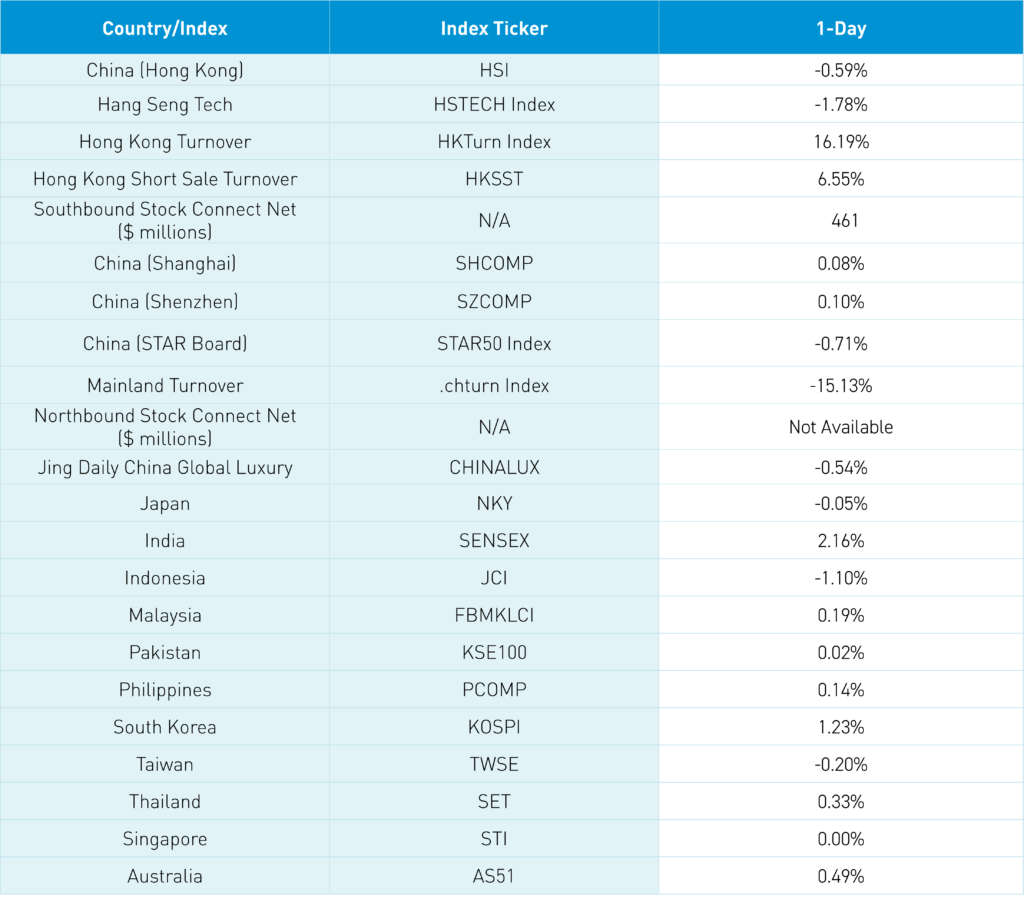

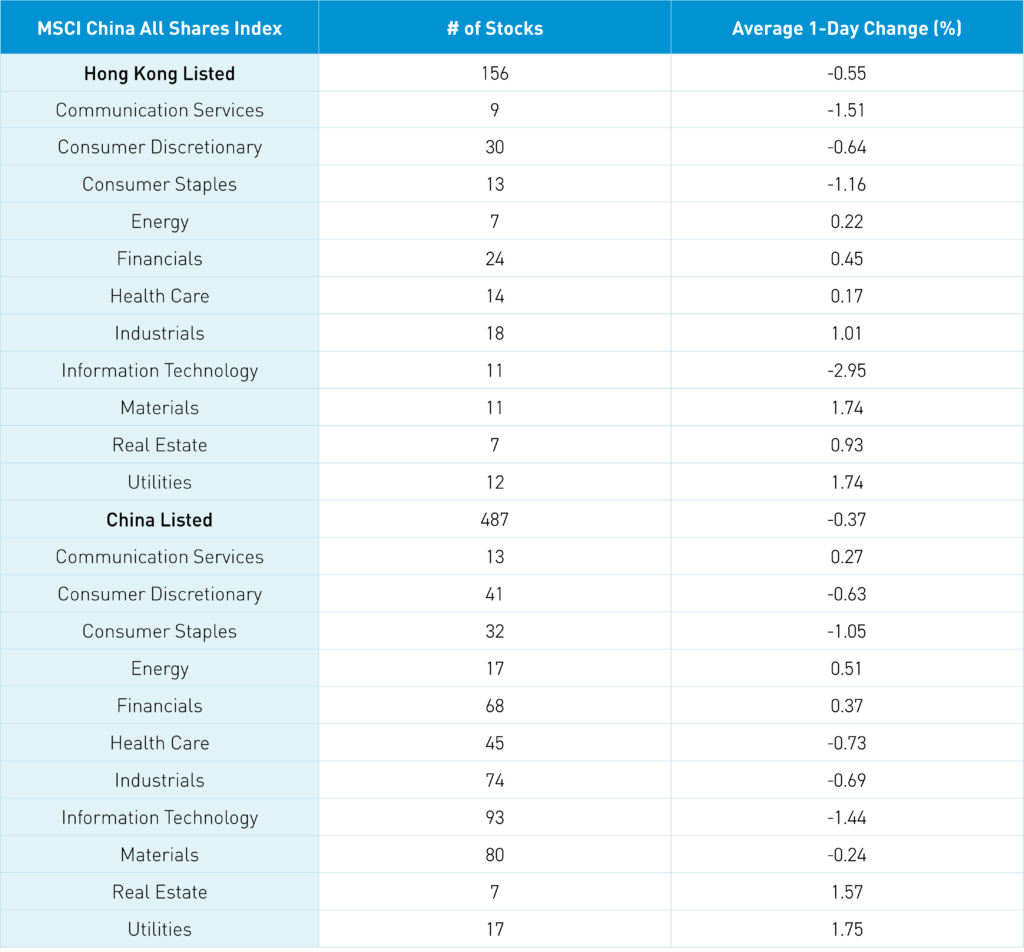

The Hang Seng and Hang Seng Tech indexes both closed lower by -0.59% and -1.78%, respectively, on volume that increased +16% from yesterday. Mainland investors bought a net $461 million worth of Hong Kong-listed stocks and ETFs overnight. The top-performing sectors were Materials, which gained +1.74%, Utilities, which also gained +1.74%, and Industrials, which gained +1.01%. Meanwhile, the worst-performing sectors were Information Technology, which fell -2.95%, Communication Services, which fell -1.51%, and Consumer Staples, which fell -1.16%.

Shanghai, Shenzhen, and the STAR Board diverged to close 0.08%, 0.10%, and -0.71%, respectively, on volume that decreased -15% from yesterday. The top-performing sectors were Utilities, which gained +1.75%, Real Estate, which gained +1.57%, and Energy, which gained +0.51%. Meanwhile, the worst-performing sectors were Information Technology, which fell -1.44%, Consumer Staples, which fell -1.05%, and Health Care, which fell -0.73%.

Last Night's Performance

Last Night's Exchange Rates, Prices, & Yields

- CNY per USD 7.25 versus 7.25 yesterday

- CNY per EUR 7.84 versus 7.89 yesterday

- Yield on 1-Day Government Bond 1.30% versus 1.30% yesterday

- Yield on 10-Year Government Bond 2.28% versus 2.28% yesterday

- Yield on 10-Year China Development Bank Bond 2.39% versus 2.39% yesterday

- Copper Price +0.75%

- Steel Price +0.36%