CPC Follows Up Monetary Stimulus With Fiscal Measures

3 Min. Read Time

President Xi presided over a meeting of the CPC Central Committee, the highest level of China’s government, with the objective being to “study the current economic situation and deploy the next step of economic work”. The release stated:

- Acknowled the economic challenges, stating “face up to difficulties

- What needs to be done? Note the emphasis on fiscal policy, which is a first: “to increase the countercyclical adjustment of fiscal and monetary policies, ensure necessary fiscal expenditures.”

- Reiterated monetary policy announced Tuesday: “Reduce the deposit reserve ratio and implement a strong rate cut.”

- Acknowledges the fall in real estate prices, which therefore requires policy support “to promote the stabilization and stabilization of the real estate market.”

- Acknowledges real estate policies are necessary to “respond to the concerns of the masses.”

- Pro-stock market support language “to boost the capital market” by allocating further funds to “social security, insurance, and wealth management entering the market. To support the mergers and acquisitions of listed companies.”

- Unemployment was addressed as there will be a “focus on key employment work for key groups such as fresh college graduates, migrant workers.”

Other measures announced:

- Bloomberg News reports that even after injecting RMB1 trillion of financial liquidity on Tuesday, “Beijing is considering pumping up to 1 trillion yuan into its biggest state banks to increase their capacity to support the struggling economy, primarily by issuing new special sovereign bonds.”

- In advance of next week’s national holiday, Reuters reports, “China will distribute a one-time allowance to disadvantaged people ahead of a national holiday next week, a government statement said.”

Key News

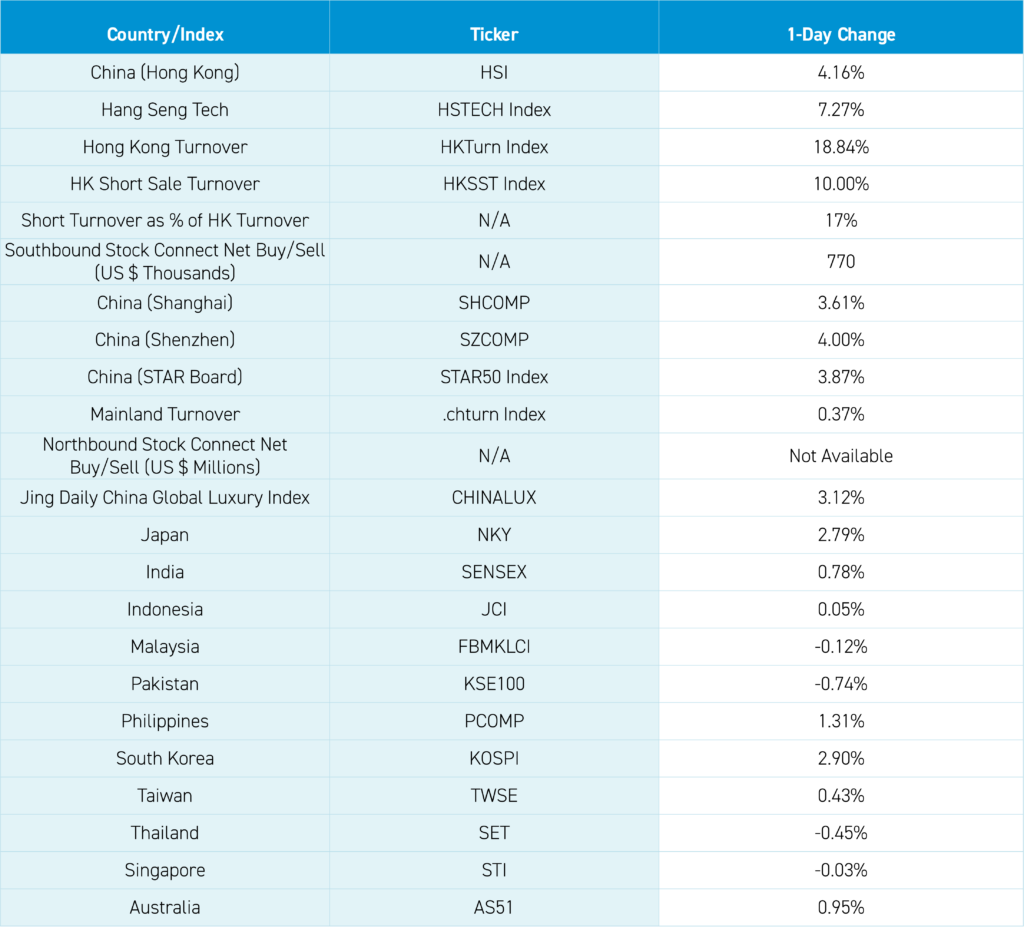

Asian equities were higher as Hong Kong and Mainland China ripped higher on very high volumes with Hong Kong at 290% of the 1-year average, Mainland China at 148% of the 1-year average, and very strong breadth driven by today’s announcement from the Chinese government’s fiscal policy support.

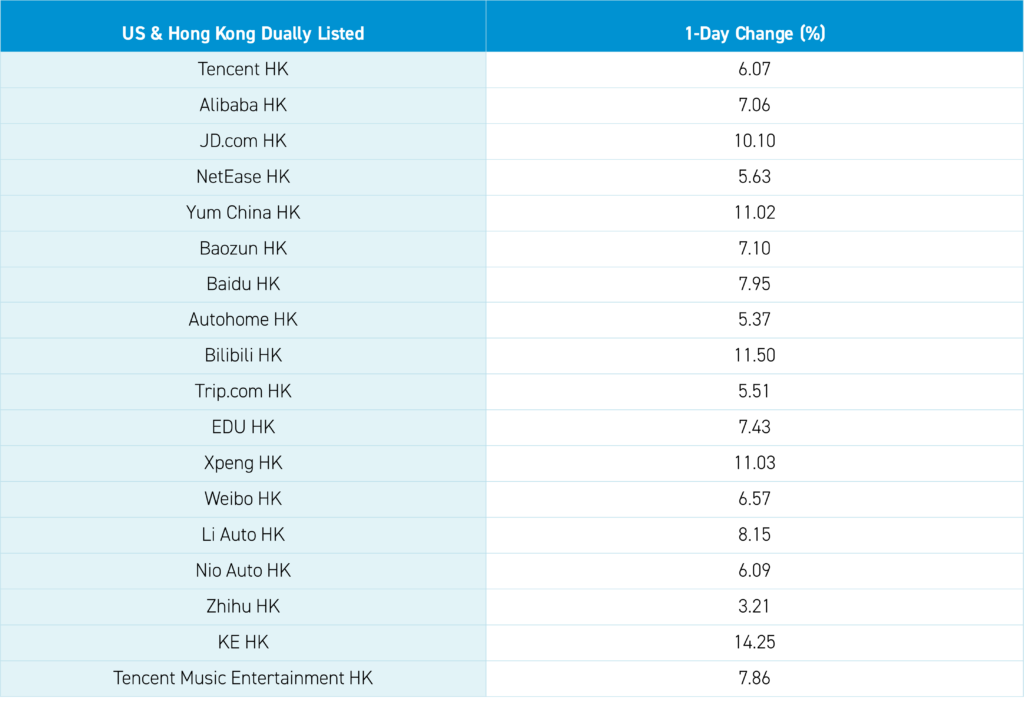

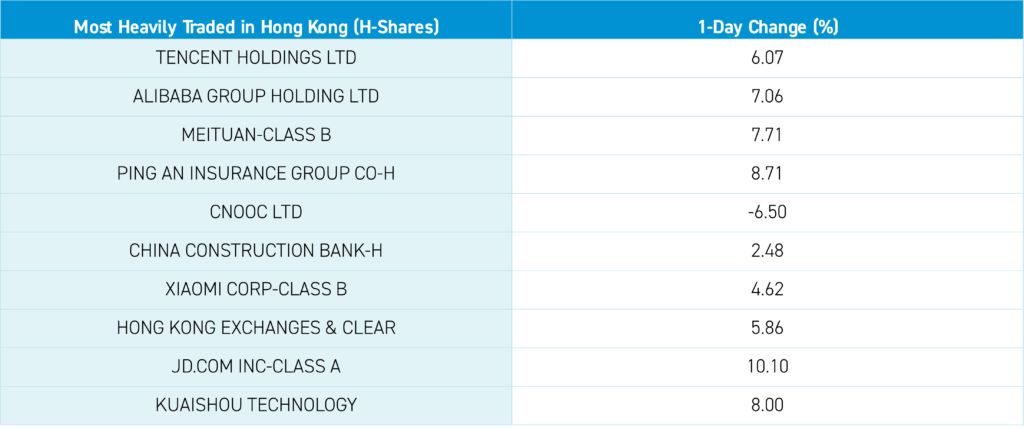

Virtually every stock was up except for energy stocks in both markets. Northbound Stock Connect volumes, i.e., foreign buying, were the highest I’ve ever seen, while Mainland investors bought a healthy $770 million worth of Hong Kong-listed stocks, including buying a healthy $884 million worth of Alibaba. The numbers speak for themselves. The skeptics said the Chinese government wouldn’t do anything before the US election. That didn’t pan out. Following Tuesday’s monetary policy support, today’s fiscal policy addresses the demand side of the equation, which has long been argued to be the issue driven by weak real estate prices. The real estate super tanker won’t turn on a dime, but we are seeing a course correction. More important is the fiscal policy direction. With significant underweights to China, significant dry powder can come back into the market. Game on!

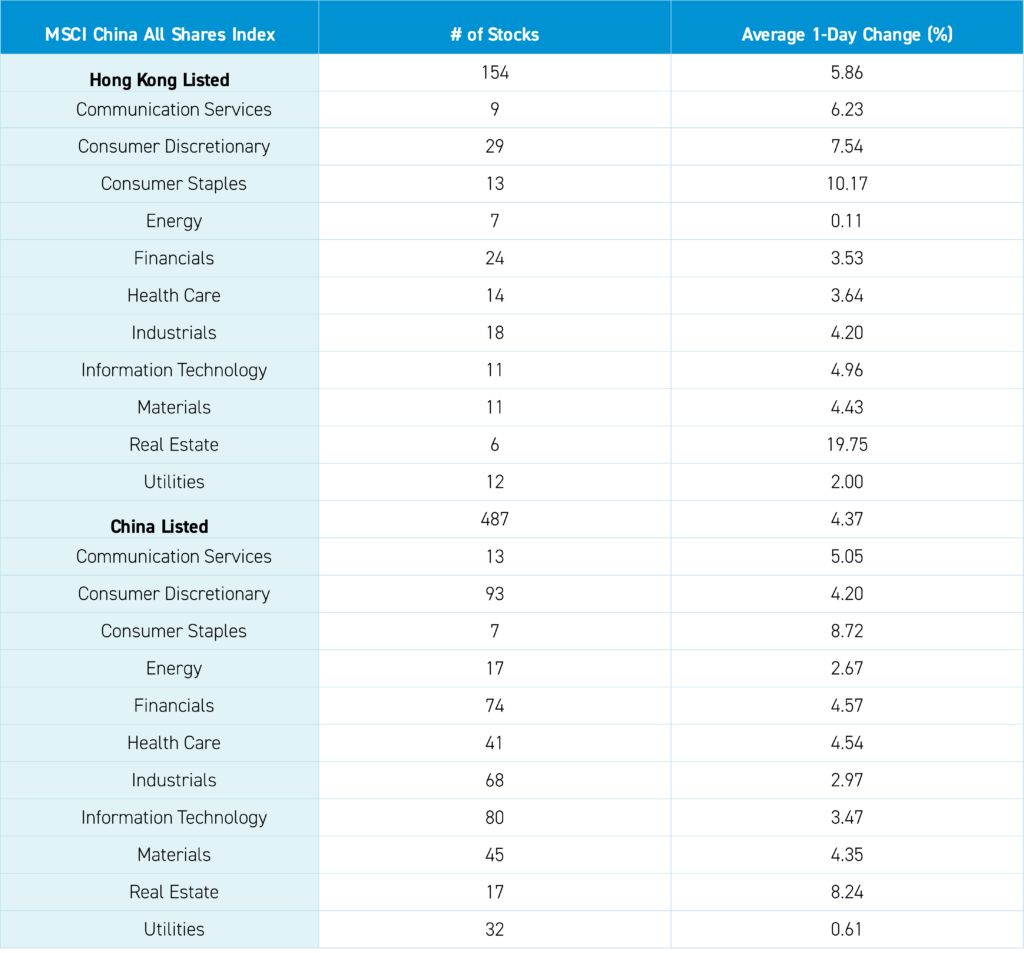

The Hang Seng and Hang Seng Tech indexes gained +4.16% and +7.27%, respectively, on volume that increased +18.84% from yesterday, which is 290% of the 1-year average. 468 stocks advanced, while 41 declined. Main Board short turnover increased 10% from yesterday, which is 294% of the 1-year average, as 17% of turnover was short turnover (Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). Growth and small caps outperformed value and large caps. All sectors were positive, with real estate +19.74%, staples +10.17%, and discretionary +7.54%. The top-performing subsectors were consumer services, food/beverages, and real estate, while telecom services and energy were among the worst-performing. Southbound Stock Connect volumes were exceedingly high/3X the average as Mainland investors bought $770 million worth of Hong Kong-listed stocks and ETFs, including Alibaba, which was a very large net buy, and China Mobile, which was a moderate net sell.

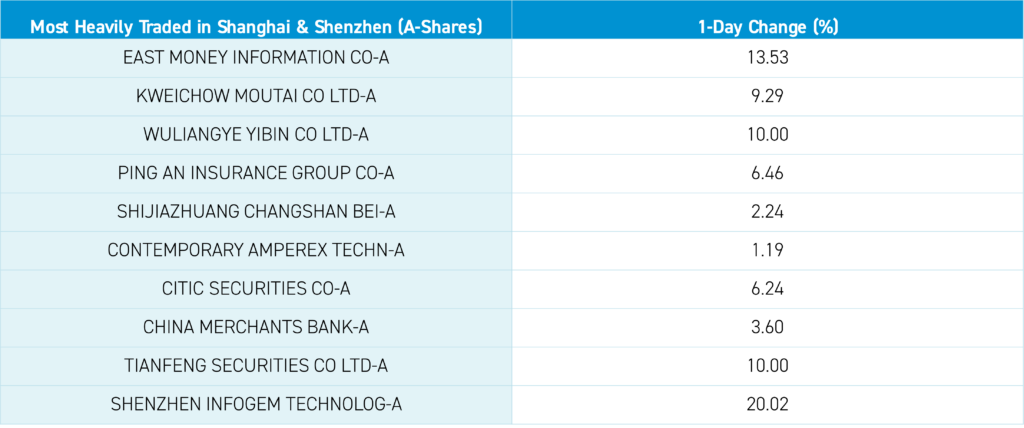

Shanghai, Shenzhen, and the STAR Board gained +3.61%, +4.00%, and +3.87%, respectively, on volume that increased +0.37% from yesterday, which is 148% of the 1-year average. 4,742 stocks advanced, while 308 declined. Growth and small caps outperformed value and large caps. All sectors were positive, including Consumer Staples, which gained +8.73%, Real Estate, which gained +8.24%, and Communication Services, which gained +5.05%. All subsectors were positive, led higher by liquor, real estate and catering. Northbound Stock Connect volumes were exceedingly high. CNY and the Asia dollar index gained versus the US dollar. Treasury bonds fell. Copper fell while steel gained.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.01 versus 7.02 yesterday

- CNY per EUR 7.82 versus 7.87 yesterday

- Yield on 10-Year Government Bond 2.07% versus 2.04% yesterday

- Yield on 10-Year China Development Bank Bond 2.16% versus 2.12% yesterday

- Copper Price -0.04%

- Steel Price +0.31%