Law Draft Focuses on Overcapacity and Price Wars

2 Min. Read Time

Key News

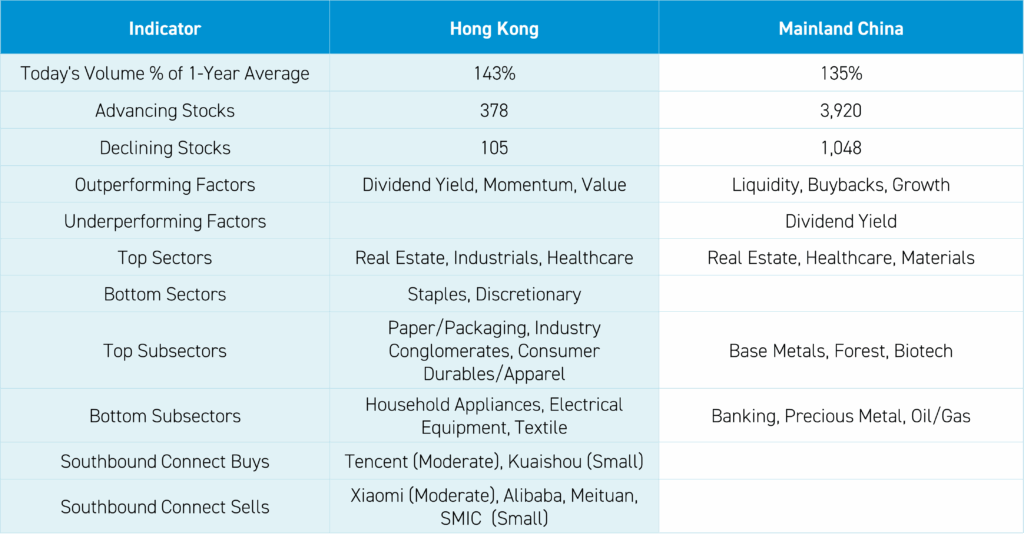

Asian equities were mixed overnight, as Japan and Mainland China outperformed.

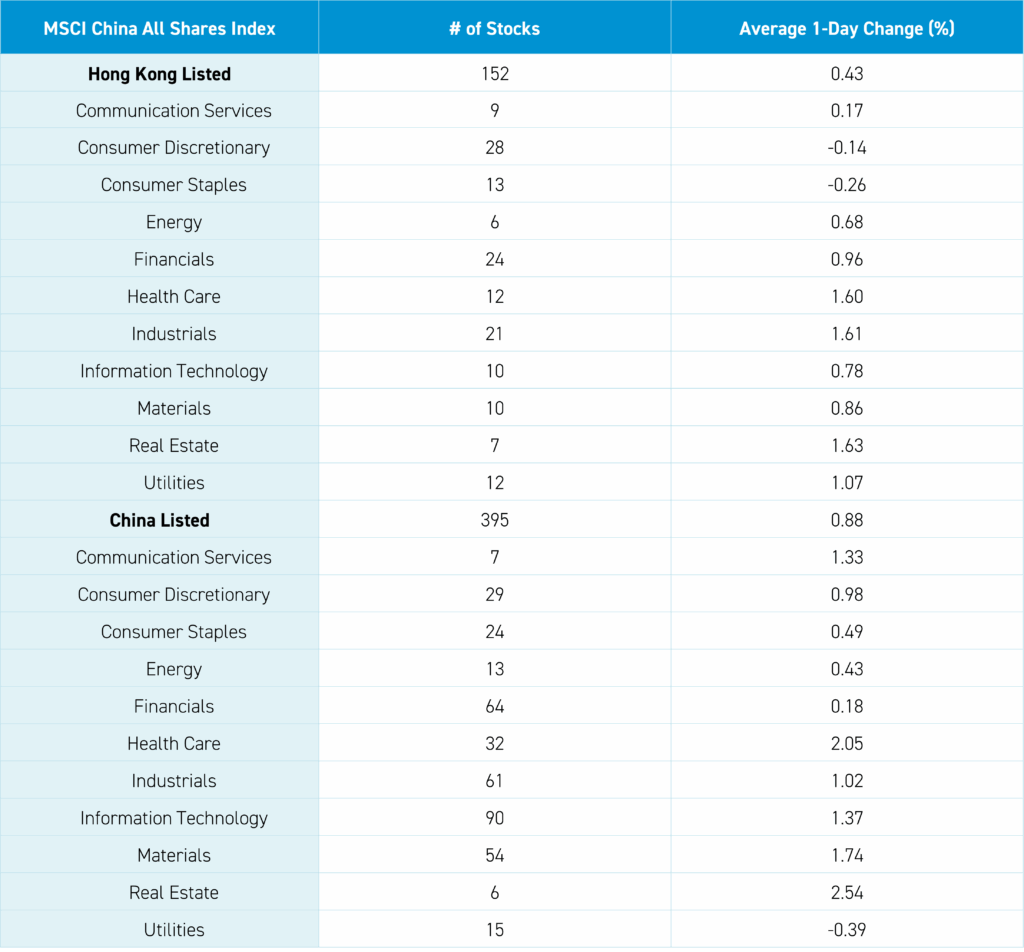

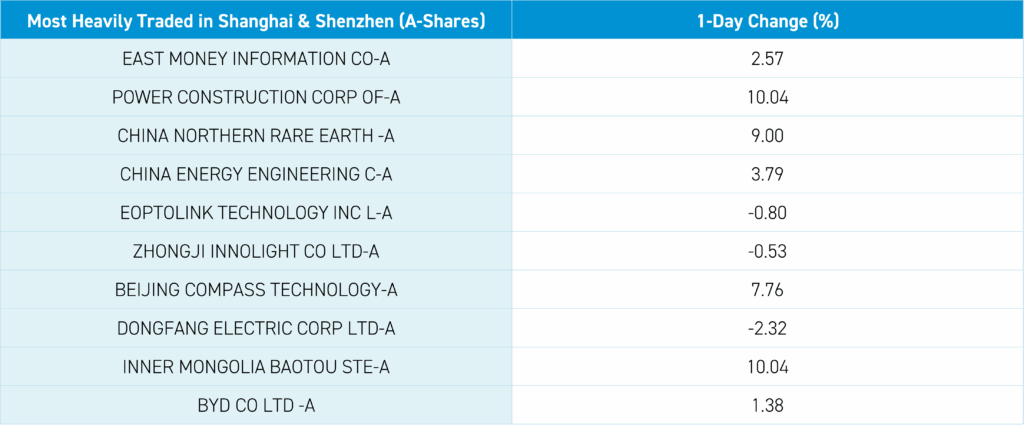

It was a relatively quiet night. Hong Kong and Mainland China-listed semiconductor stocks were higher on President Trump’s AI Action Plan. Mainland China had a very broad rally, led by Shenzhen-listed growth stocks, while mega-cap banks, oil, and telecom all lagged. Hong Kong and Mainland China were also led by healthcare and materials. Remember our thesis that foreign investors will always favor growth stocks when investing in China!

The biggest news item today was the announcement from the National Development and Reform Commission (NDRC) and State Administration for Market Regulation (SAMR) of a new price law amendment draft that included “criteria for identifying unfair price behavior”, including “identifying low-priced dumping”, “improving the identification standards of unfair price behaviors such as price collusion” and stated that industry leaders “shall not use their influence or dominant position in the industry to force or bundle sales of goods”.

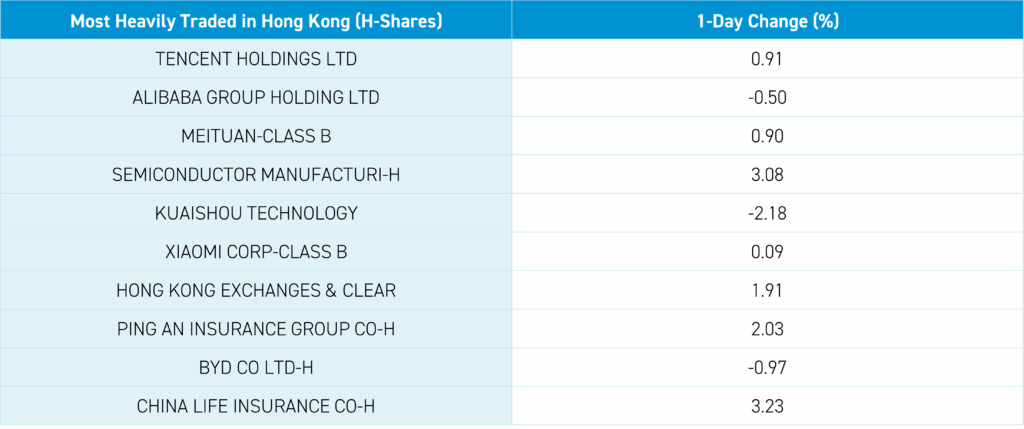

Reuters had a good article on rising commodity prices in China and the government’s overcapacity reduction campaign (I will put it on X/Twitter @ahern_brendan). Another thesis is that China’s deflationary days are over, in addition to China exporting deflation. Hopefully, the restaurant delivery war between Meituan, Alibaba, and JD.com will also end. Meituan gained +0.90%, as the company appeared to notice the writing on the wall. It held a symposium in Shanghai with participants in its ecosystem, including restaurant owners, who voiced their concerns that the current delivery price war is weighing on restaurant dining. Remember, we had Shanghai’s local SAMR meet with Meituan, JD.com, and Alibaba yesterday.

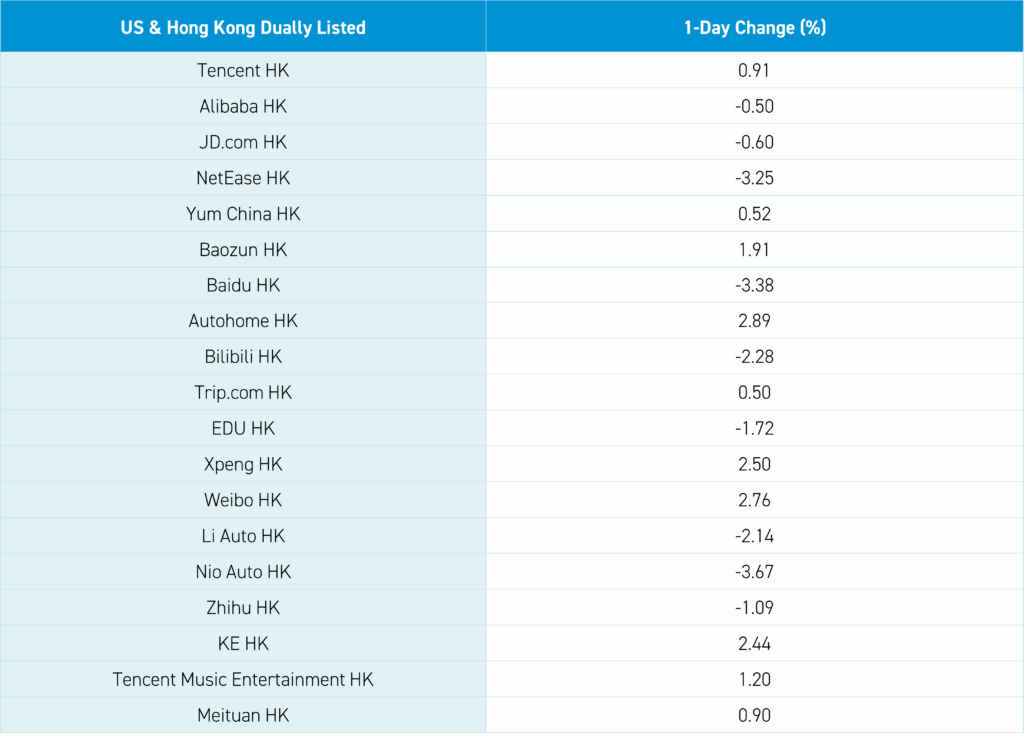

Hong Kong growth stocks were mixed, as Tencent gained +0.91%, NetEase fell -3.25%, CATL fell -1.24%, and Alibaba fell -0.50%. Biotech was led higher by Wuxi Biologics, which gained +3.83% after announcing that its first-half of 2025 revenue will increase ~16% year-over-year (YoY) and net income increased ~56% YoY. Mainland investors bought a net $473 million worth of Hong Kong-listed stocks and ETFs via Southbound Stock Connect.

The State-owned Assets Supervision and Administration Commission (SASAC) met with local SOEs in Beijing to discuss implementing reforms and becoming more efficient. President Xi met with European Commission President Ursula von der Leyen and European Council President Antonio Costa on EU-China relations. Premier Li met with EU Commission Chairman von der Leyen on trade. He will also give a speech at the opening of the 2025 World Artificial Intelligence Conference in Shanghai on July 26th.

The China equity rally is a sleeper of a trade (not just YTD, but also since January 2024), though the renminbi’s rally versus the US dollar is even more so. On April 9th, CNY per USD hit 7.34 versus today’s close of 7.15. Yes, the US dollar index is off nearly twice as much in percentage terms versus CNY’s gains.

Last Night's Performance

Last Night's Exchange Rates, Prices, & Yields

- CNY per USD 7.15 versus 7.16 yesterday

- CNY per EUR 8.40 versus 8.39 yesterday

- Yield on 10-Year Government Bond 1.74% versus 1.70% yesterday

- Yield on 10-Year China Development Bank Bond 1.83% versus 1.78% yesterday

- Copper Price +0.04%

- Steel Price -0.09%