$400 Million Of Alibaba Buying Today

3 Min. Read Time

Key News

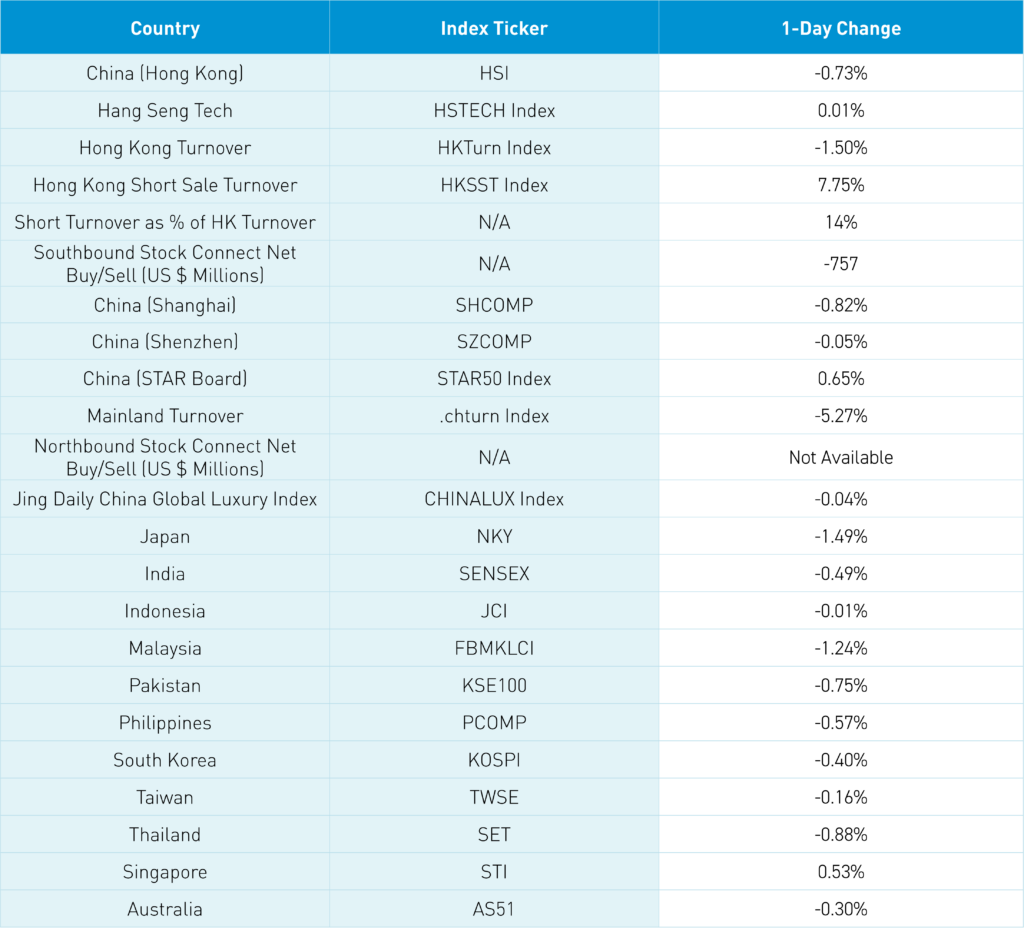

Asian equities had a rough night. Japan and Malaysia underperformed the region, and the US dollar weakened. Investors were likely occupied with the Trump-Harris debate last night.

The US dollar’s weakness was viewed as a sign of a Harris debate win, though neither candidate is fiscally responsible, in my opinion. There were fairly light volumes as investors wait for today’s US CPI print in advance of next week’s Fed 25 basis point or 50 basis point cut.

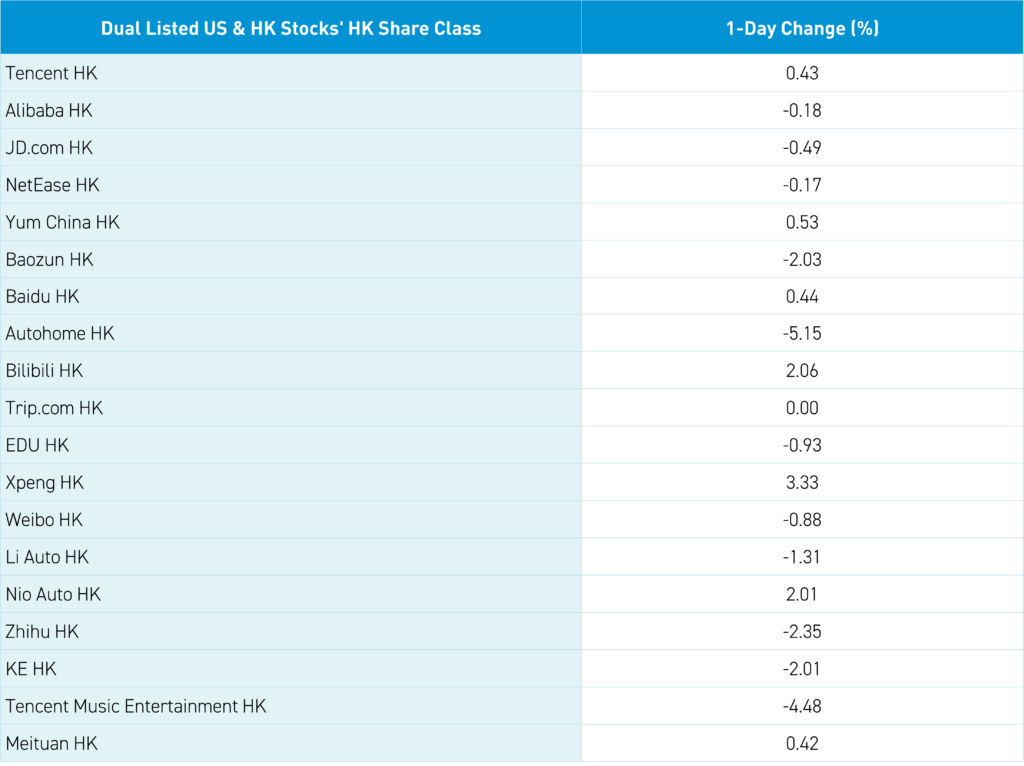

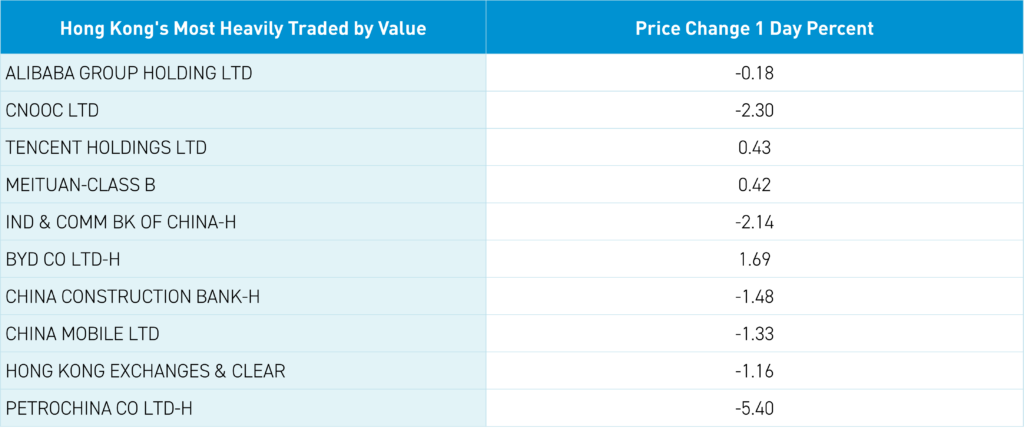

Growth stocks in both Hong Kong and Mainland China outperformed as Hong Kong internet, pharmaceuticals, and Hong Kong and Mainland China electric vehicles/automobiles outperformed while Hong Kong/Mainland China mega capitalization banks, telecommunications, insurance, and energy stocks were weak. Hong Kong was off, led by the most heavily traded stocks by value, which included Alibaba, falling -0.18% as Mainland investors bought a net $400 million worth of the stock today via Southbound Stock Connect versus yesterday’s $1.086 billion, energy giant CNOOC, which fell by -2.3%, Tencent, which gained +0.43% as the company bought back 2.72 million shares today, Meituan which gained +0.42%, ICBC which fell -2.14%, and BYD which gained +1.69%. It is worth noting Alibaba bought the equivalent of 719,500 US-listed ADRs yesterday, which means the buyback accounted for 4.7% of yesterday's ADR volume (15.327 million ADRs shares traded).

Electric vehicle and lithium miner stocks had a good day, helped by chatter that CATL, which gained +2.98%, is curtailing lithium production at a mine, as the solution for low prices is less supply! Reports that Spain is reconsidering its support for EU China EV tariffs after Prime Minister Sanchez met with President Xi yesterday also helped electric vehicle/automobile stocks.

Wuxi AppTec gained +6.83% after the company announced a RMB 1 billion buyback following the US House passage of the Biosecure Act, which sent shares lower despite skepticism that the bill will pass in the Senate. The House’s “China week” has garnered little news, with more than two dozen bills up for a vote. Mainland China was off, though mid and small-capitalization stocks had a good day versus mega-capitalization stocks, with some chatter about small-capitalization equity ETFs experiencing mysterious volume pick-ups at the market’s close. Is the National Team broadening its support beyond mega-caps? It's hard to tell as there is no definitive evidence at this point. The State Council met yesterday to discuss raising the retirement age, which makes sense. Demographics also explain the elimination of foreign baby adoption.

The Hang Seng and Hang Seng Tech diverged by -0.73% and +0.01%, respectively, on volume down -1.5% from yesterday, which is 102% of the 1-year average. 132 stocks advanced, while 353 declined. Main Board short turnover increased by +7.75% from yesterday, which is 87% of the 1-year average, as 14% of turnover was short turnover (Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). Growth stocks were down less than value stocks, though large and small capitalization stocks were down the same. The top-performing sectors were healthcare, up +3.07%, technology, up +0.71%, and communication services, up +0.32%, while utilities fell -3.14%, energy fell -1.78%, and financials fell -1.51%. The top sub-sectors were pharmaceuticals, automobiles, and materials, while food/consumer staples, media, and utilities were the worst. Southbound Stock Connect volumes were moderate/light as Mainland investors sold a narrow body -$757 million of Hong Kong stocks and ETFs with Alibaba a large net buy, China Mobile a moderate net buy, the Hong Kong Tracker a large net sell, Hong Kong Exchanges, Tencent, and the Hang Sang China Enterprise ETF were moderate/large net sells.

Shanghai, Shenzhen, and the STAR Board diverged to close -0.82%, -0.05%, and +0.65%, respectively, on volume down -5.27% from yesterday, which is 64% of the 1-year average. 1,409 stocks advanced, while 3,510 declined. Growth and small capitalization stocks outpaced value and large capitalization stocks. The top sectors were consumer discretionary, which gained +1.82%, industrials, up +0.96%, and real estate, up +0.95%, while utilities fell -3.81%, energy fell -2.09%, and financials fell -1.32%. The top sub-sectors were motorcycles, power generation equipment, and electric power grid, while highways, power, and ports were the worst. Northbound Stock Connect volumes were light. CNY and the Asia dollar index gained versus the US dollar. Treasury bonds rallied. Copper fell while steel gained.

RIP to my friend and classmate Beth Quigley, who lost her life as it was just beginning twenty-three years ago today in the World Trade Center, to all those families still suffering, our condolences.

Last Night's Performance

Last Night's Exchange Rates, Prices, & Yields

- CNY per USD 7.11 versus 7.11 yesterday

- CNY per EUR 7.85 versus 7.85 yesterday

- Yield on 10-Year China Government Bond 2.10% versus 2.11% yesterday

- Yield on 10-Year China Development Bank Bond 2.20% versus 2.22% yesterday

- Copper Price -0.16%

- Steel Price +0.06%