Balloon Pops Blinken’s Visit, For Now

3 Min. Read Time

Key News

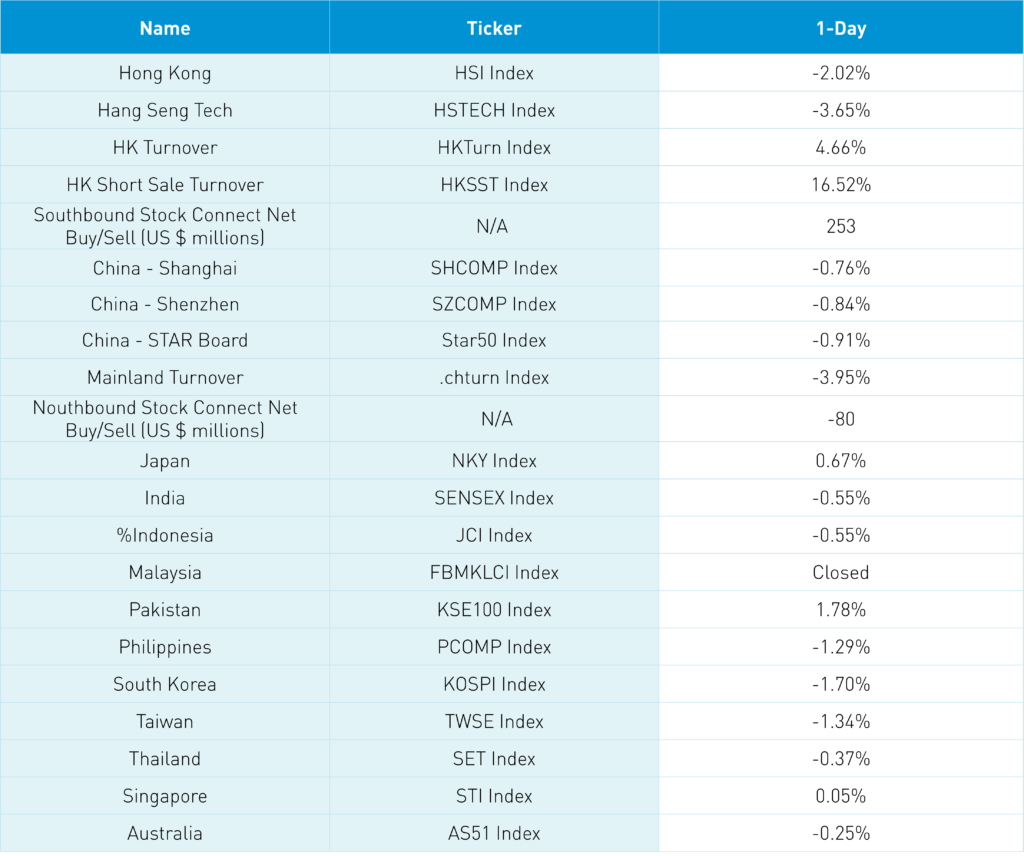

Asian equities were largely lower after Friday’s unexpectedly strong US nonfarm payroll release that potentially pauses the Fed pivot, which is weighing on US equities today. The potential for more Fed hikes fueled a very strong US dollar, hitting the Asia dollar index, which fell -0.9% on Friday, followed by -0.1% today as CNY fell -0.99% on Friday.

I started with payroll as it was the primary culprit for Friday’s weakness in US-listed China stocks and today’s follow-through down move in Hong Kong. Yes, the balloon was also a contributor, though the die had been cast. The balloon’s timing is most unfortunate as Secretary of State Blinken’s trip was postponed. He would have been the most senior US official to visit China since 2018. Politico had an interesting article saying he will likely rebook the trip as the balloon incident provides him significant leverage.

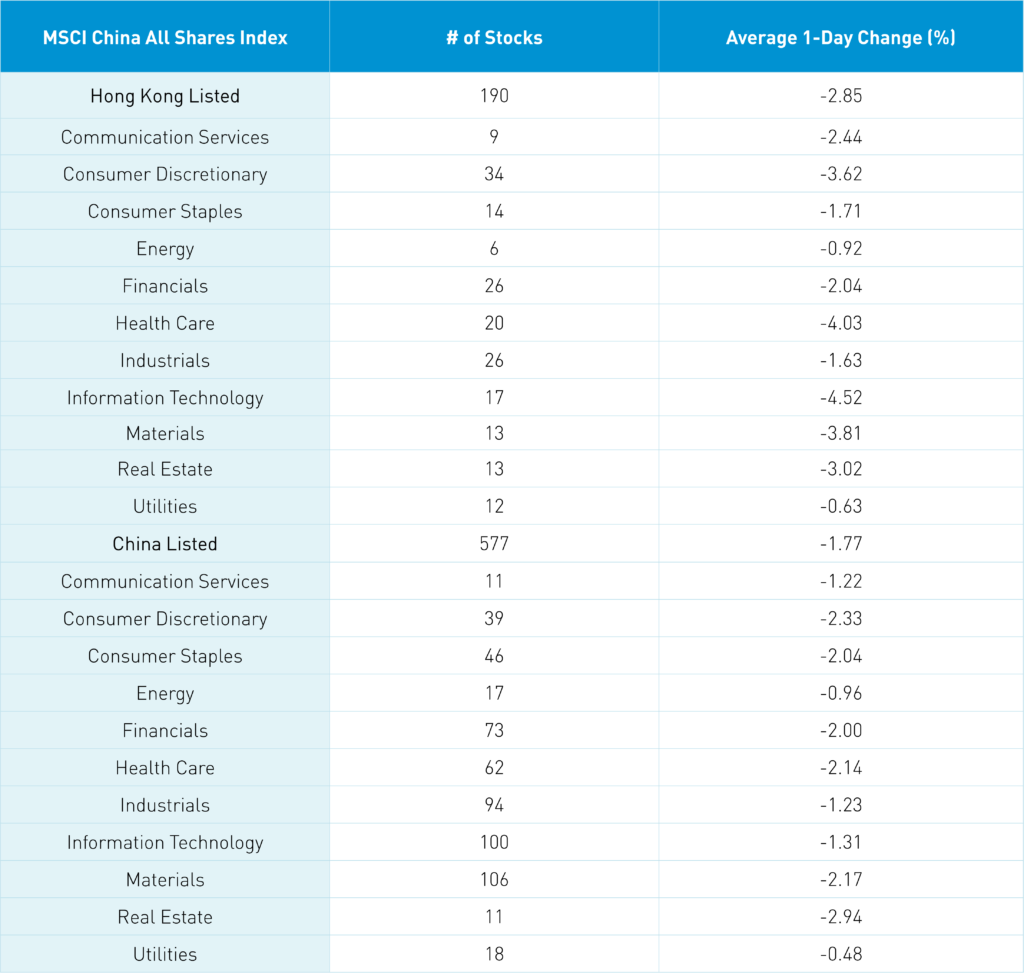

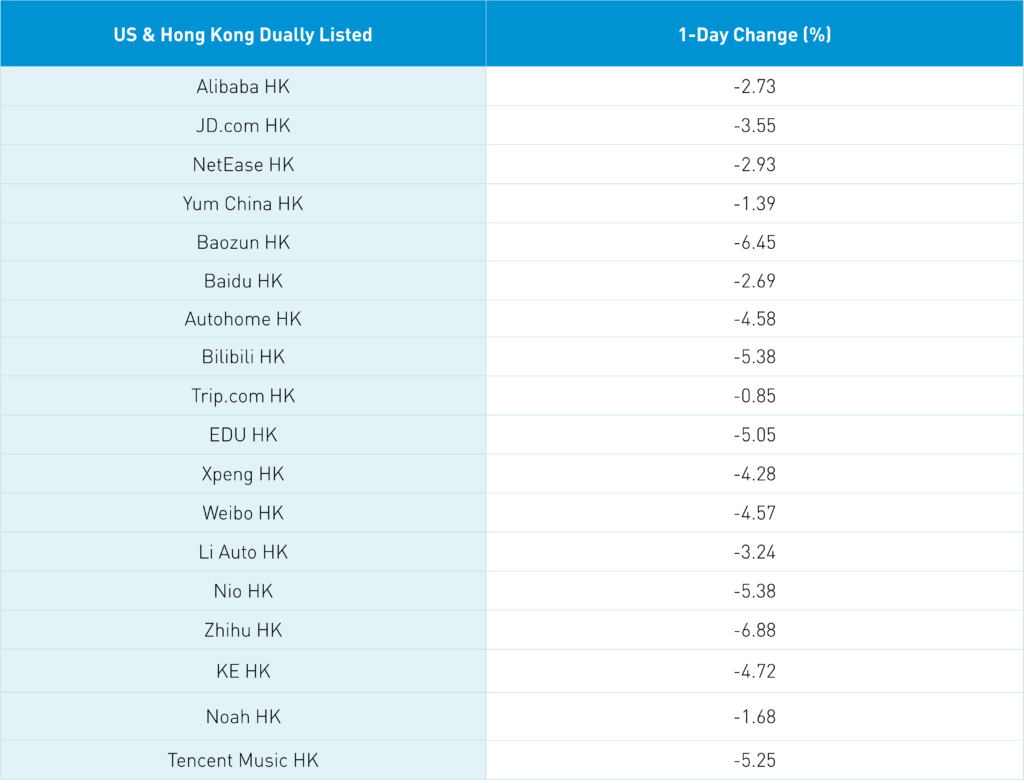

Hong Kong and US-listed China stocks represent foreign sentiment regarding China, which was off, while Shanghai and Shenzhen represent what Chinese investors think about China. This produced a significant disparity overnight as foreign sentiment proved to be volatile. Hong Kong’s most heavily traded stocks by value were Tencent, which fell -2.13%, Meituan, which fell -5.03%, and Alibaba, which fell -2.73%, as breadth was very poor, with only 35 positive stocks, while 474 stocks declined. The Hong Kong Stock Exchange lost -4.2%, despite announcing a partnership with Saudi Arabia, an indication of the mood. Main Board short interest up ticked to 17% of total turnover, though Mainland investors bought the dip via Southbound Stock Connect, in a slightly positive move on a rough day.

Yum China will report Q4 financials after the US market close today. The key will not be Q4 financial results, but, rather, their Q1 outlook as China’s reopening should be a strong catalyst. For managers that are underweight China, the pullback/correction from the past week may provide an opportunity to get back in.

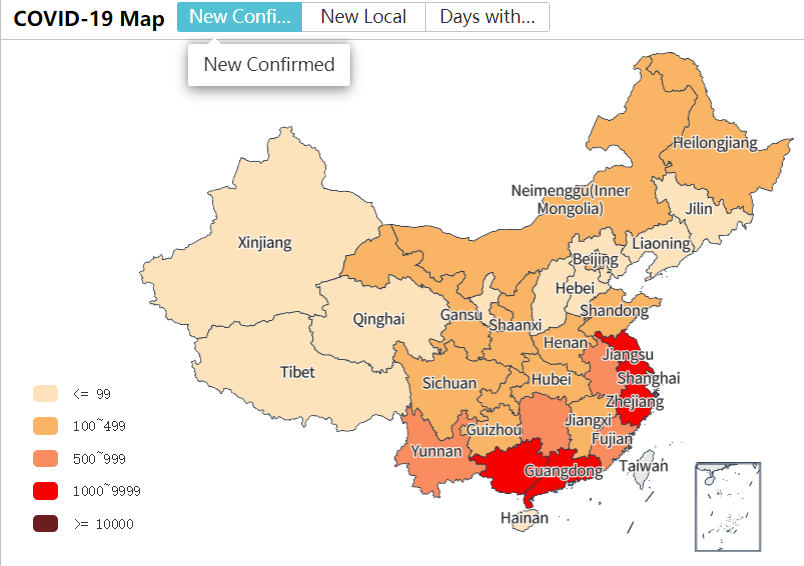

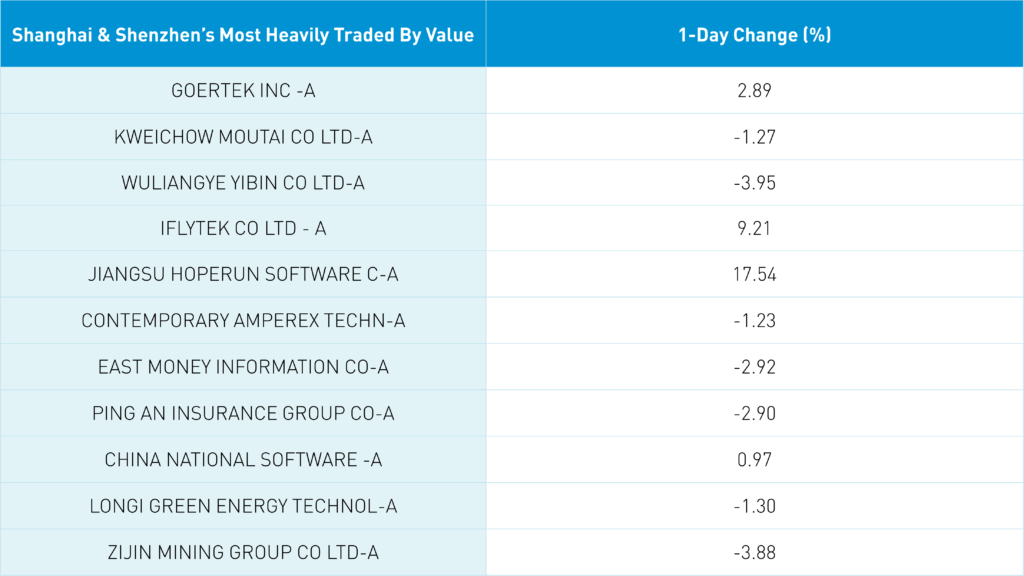

Mainland China was off but less than Hong Kong as Mainland investors were less concerned about US payrolls and the balloon. OpenAI’s ChatGPT has garnered interest in China, lifting AI-related stocks. Foreign investors were very small sellers of Mainland stocks. The People’s Bank of China, China’s central bank, pulled money out of the financial system, which happens after the big holiday week.

The Hang Seng and Hang Seng Tech indexes fell -2.02% and -3.65%, respectively, on volume that increased +4.66% from Friday, which is 108% of the 1-year average. 35 stocks advanced, while 474 stocks declined. Main Board short turnover increased +16.53% from Friday, which is 104% of the 1-year average, as 17% of turnover was short turnover. Value factors outperformed growth factors as large caps outperformed small caps. All sectors were down with tech falling -4.5%, healthcare falling -4.02%, and materials falling -3.8%. All subsectors were negative as pharma/biotech, technical hardware/equipment and healthcare equipment were among the worst. Southbound Stock Connect volumes were moderate/light as Mainland investors bought $253 million worth of Hong Kong stocks as Tencent was a small net buy, Meituan was a large net sell, and Kuaishou was a small net sell.

Shanghai, Shenzhen, and the STAR Board were down -0.76%, -0.84%, and -0.91%, respectively, on volume that decreased -3.95% from yesterday, which is 96% of the 1-year average. 1,782 stocks advanced, while 2,891 stocks declined. Value factors edged out growth factors as small caps “outperformed” large caps. All sectors were negative as real estate fell -2.85%, consumer discretionary fell -2.24%, and materials fell -2.08%. The top-performing subsectors were internet, software, and computer hardware. Meanwhile, precious metals, diversified financials, and household appliances were among the worst. Northbound Stock Connect volumes were light as foreign investors sold a net -$80 million worth of Mainland stocks. CNY fell gained versus the US dollar, Treasury bonds were sold, copper was off, and steel gained.

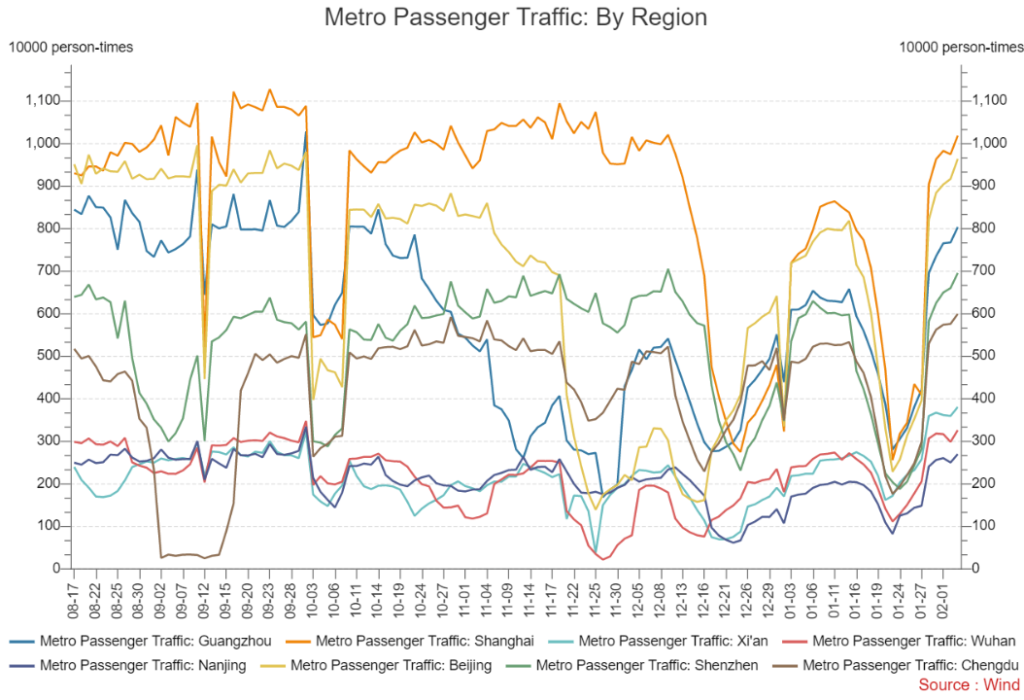

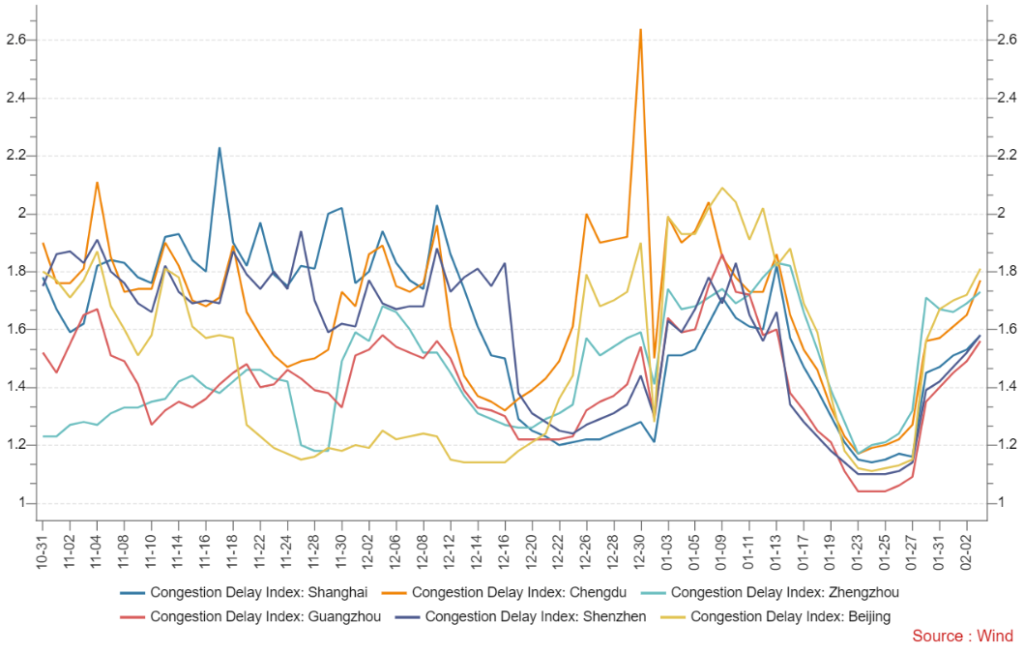

Major Chinese City Mobility Tracker

Up, up, and away.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 6.79 versus 6.80 Friday

- CNY per EUR 7.29 versus 7.33 Friday

- Yield on 1-Day Government Bond 1.40% versus 1.29% Friday

- Yield on 10-Year Government Bond 2.90% versus 2.89% Friday

- Yield on 10-Year China Development Bank Bond 3.06% versus 3.06% Friday

- Copper Price -0.54% overnight

- Steel Price +0.15% overnight