Signs of Improving US-China Relations, Week in Review

7 Min. Read Time

Week in Review

- Asian equities were nearly all lower this week, except for Mainland China’s STAR Board, on a hawkish US Fed.

- China reported retail sales for November on Monday that missed expectations overall though sales household appliances and autos, the targets of trade-in programs, were particularly strong.

- Tencent and Bytedance were tapped by Apple this week to provide AI-enabled services in iPhones sold in China.

- Battery giant CATL has become the first to challenge carmaker NIO on its battery swapping technology.

Key News

Asian equities ended an off week lower overnight despite a weaker US dollar.

Today is the last liquidity event of the year as index funds and ETFs benchmarked to FTSE Russell indices traded at the market’s close. I would never name names, though FTSE’s largest client is a large index fund, and an ETF provider based in a town in Pennsylvania where George Washington stayed one winter during the Revolutionary War.

Hong Kong bounced around the room while Shanghai and Shenzhen faded into afternoon trading. It was a light session on little news, which is eerily similar to yesterday’s market action in both markets, as the Technology and Communication Services sectors outperformed again.

Tencent gained +2.7% on its new monetary gifting functionality, which might be considered a competitor to E-Commerce players Alibaba, which fell -3.44%, and JD.com, which fell -3.03%, overnight. Then again, both Alibaba and JD.com were net sells today in FTSE indices, which may have accounted for their share price declines. Tencent, along with Weimob, which surged +25.37% following yesterday’s +35% gain, is also benefitting from the Reuters article on their AI collaboration with Apple. Tencent alone contributed 44 points and 10 points to the Hang Seng Index and Hang Seng Tech indexes, respectively.

Semiconductors and technology subsectors rose again on the rumor that Biden will further curtail US semiconductor exports to China before moving out of 1600 Pennsylvania Avenue, which is a gift to local Chinese semiconductor companies, as the Hong Kong-listed Semiconductor Manufacturing (SMIC) gained +8.22% today.

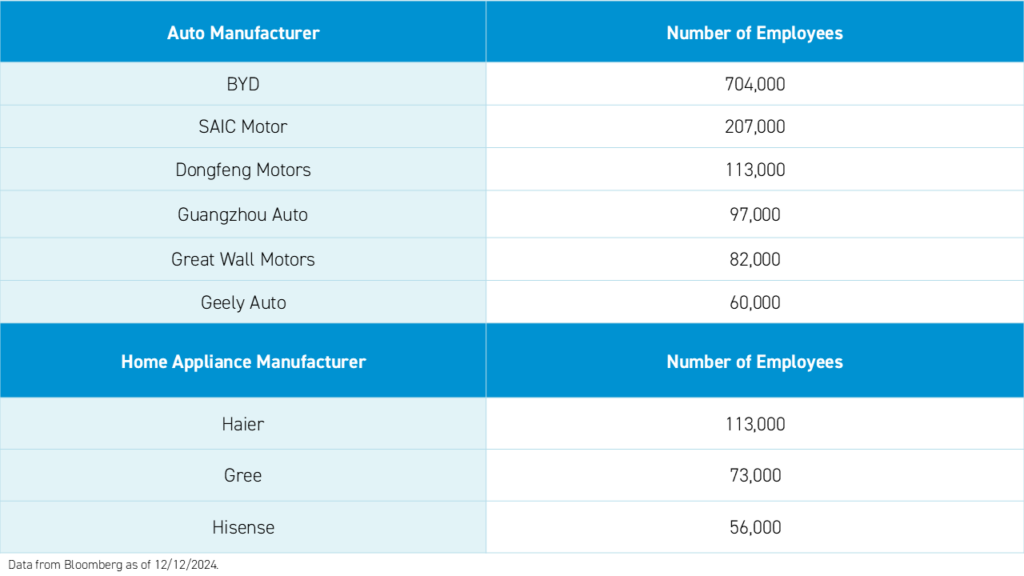

Mainland media highlighted yesterday’s Ministry of Commerce (MoC) release on the expansion of “large-scale equipment replacement and consumer goods exchange”, which was focused on autos and home appliances. 33.3 million people bought 52.1 million home appliance products due to the program. Based on this success, the MoC is exploring how it can expand the program. The trade-in subsidy obviously helps domestic consumption, but implicitly helps employment. BYD alone employs more than 700,000 people.

Through the lens of employment, personal electronics could be the next focus area for trade-in subsidies.

Mainland investors bought a net $209 million worth of Hong Kong-listed stocks and ETFs, including the Hong Kong Tracker ETF, which was a significant net sell after yesterday’s buying, via Southbound Stock Connect. Alibaba was sold and Tencent was bought.

China’s 10-Year Government bond yield hit a new 52-week and all-time low of 1.71%, as the Loan Prime Rate (LPR) was left unchanged, as expected.

The National Team’s favored ETFs had nearly average volumes, indicating potential intervention.

Much attention was given to last night’s US House of Representatives’ failed vote to keep the US government funded via a continuing resolution (CR). In an example of how boring my Thursday night was, or my dedication to you, the reader, I might be one of the few people to notice that the second CR version no longer includes the “Comprehensive Outbound Investment National Security Act of 2024”. What caused the difference between the first and second CR? President Trump and Elon Musk! Stop and think about what the removal means based on who caused the revision. What does that tell you about the incoming President and his key advisor’s view of China?

We know President Trump has extended an invitation to President Xi to the inauguration. While I think President Xi should attend and bring ten Chinese CEOs who can open factories in the US, it is unlikely. However, I believe Premier Li or someone very high up will attend. The “Art of the Deal” could lead to a grand bargain. Is any investor positioned for that? I don’t think so.

This change and its implications might be the most important thing ever written in ChinaLastNight.com. Candidly, I found the “Comprehensive Outbound, etc.” language legal mumbo jumbo. Nonetheless, while it clearly would prohibit investing in military companies, the scope was potentially very broad to punish many US corporate interests.

The Hang Seng and Hang Seng Tech indexes diverged to close -0.16% and +0.11%, respectively, on volume that increased +24.91% from yesterday, which is 136% of the 1-year average. 153 stocks advanced while 335 stocks declined. Main Board short sale turnover decreased -1.28% from yesterday, which is 121% of the 1-year average, as 14% of turnover was short turnover (Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). The growth factor and small caps outperformed the value factor and large caps. The top-performing sectors were Technology, which gained +1.76%, and Communication Services, which gained +1.69%. Meanwhile, Energy fell -1.80%, Materials fell -1.50%, and Consumer Discretionary fell -1.35%. The top-performing subsectors were semiconductors, software, and technology hardware. Meanwhile, coal, steel, and consumer discretionary were among the worst-performing subsectors. Southbound Stock Connect volumes were 1.5x pre-stimulus levels, as Mainland investors bought a net $209 million worth of Hong Kong-listed stocks and ETFs, including Tencent, SMIC, Weimob, XtalPi, and East Buy. Meanwhile, Alibaba and Kuaishou were large net sells.

Shanghai, Shenzhen, and the STAR Board diverged to close -0.06%, +0.44%, and +1.83%, respectively, on volume that increased +4.8% from yesterday, which is 147% of the 1-year average. 3,422 stocks advanced while 1,531 stocks declined. The growth factor and small caps outperformed the value factor and large caps. The top-performing sectors were Technology, which gained +0.65%, Real Estate, which gained +0.54%, and Financials, which gained +0.03%. Meanwhile, the worst-performing sectors were Energy, which fell -2.09%, Industrials, which fell-1.22%, and Materials, which fell -1.10%. The top-performing subsectors were semiconductors, chemicals, and aerospace. Meanwhile, construction machinery, coal, and shipping were among the worst-performing subsectors. Northbound Stock Connect volumes were just above average. CNY fell slightly versus the US dollar and the Asia dollar index gained small versus the US dollar. Treasury bonds rallied. Copper and steel fell.

Last Night's Performance

| Country/Index | Ticker | 1-Day Change |

|---|---|---|

| China (Hong Kong) | HSI Index | -0.2% |

| Hang Seng Tech | HSTECH Index | 0.1% |

| Hong Kong Turnover | HKTurn Index | 24.9% |

| HK Short Sale Turnover | HKSST Index | -1.3% |

| Short Turnover as a % of HK Turnovr | N/A | 13.7% |

| Southbound Stock Connect Net Buy/Sell (US $ Millions) | N/A | 52.6 |

| China (Shanghai) | SHCOMP Index | -0.1% |

| China (Shenzhen) | SZCOMP Index | 0.4% |

| China (STAR Board) | Star50 Index | 1.8% |

| Mainland Turnover | .chturn Index | 4.8% |

| Nouthbound Stock Connect Net Buy/Sell (US $ Millions) | N/A | Not Available |

| Jing Daily China Global Luxury Index | CHINALUX Index | -0.4% |

| Japan | NKY Index | -0.3% |

| India | SENSEX Index | -1.5% |

| Indonesia | JCI Index | 0.1% |

| Malaysia | FBMKLCI Index | -0.5% |

| Pakistan | KSE100 Index | 3.4% |

| Philippines | PCOMP Index | 0.2% |

| South Korea | KOSPI Index | -1.3% |

| Taiwan | TWSE Index | -1.8% |

| Thailand | SET Index | -0.9% |

| Singapore | STI Index | -1.1% |

| Australia | AS51 Index | -1.2% |

| MSCI China All Shares Index | # of Stocks | Average 1-Day Change (%) |

|---|---|---|

| Hong Kong Listed | 152 | -0.08 |

| Communication Services | 9 | 1.69 |

| Consumer Discretionary | 30 | -1.34 |

| Consumer Staples | 13 | -0.09 |

| Energy | 7 | -1.8 |

| Financials | 23 | -0.33 |

| Health Care | 13 | -0.78 |

| Industrials | 19 | -0.75 |

| Information Technology | 10 | 1.77 |

| Materials | 10 | -1.6 |

| Real Estate | 6 | -0.4 |

| Utilities | 12 | -0.58 |

| Mainland China Listed | 432 | -0.38 |

| Communication Services | 9 | -0.48 |

| Consumer Discretionary | 31 | -0.84 |

| Consumer Staples | 27 | -0.23 |

| Energy | 16 | -2.09 |

| Financials | 63 | 0.03 |

| Health Care | 40 | -0.07 |

| Industrials | 69 | -1.22 |

| Information Technology | 85 | 0.65 |

| Materials | 68 | -1.1 |

| Real Estate | 7 | 0.54 |

| Utilities | 17 | -0.79 |

| US & Hong Kong Dually Listed | Ticker | 1-Day Change (%) |

|---|---|---|

| Tencent HK | 700 HK Equity | 2.7 |

| Alibaba HK | 9988 HK Equity | -3.4 |

| JD.com HK | 9618 HK Equity | -3 |

| NetEase HK | 9999 HK Equity | -0.6 |

| Yum China HK | 9987 HK Equity | -0.1 |

| Baozun HK | 9991 HK Equity | -5.5 |

| Baidu HK | 9888 HK Equity | -2.6 |

| Autohome HK | 2518 HK Equity | -3.3 |

| Bilibili HK | 9626 HK Equity | -0.3 |

| Trip.com HK | 9961 HK Equity | -0.1 |

| EDU HK | 9901 HK Equity | 0.3 |

| Xpeng HK | 9868 HK Equity | 0.2 |

| Weibo HK | 9898 HK Equity | -2.6 |

| Li Auto HK | 2015 HK Equity | 2.4 |

| Nio Auto HK | 9866 HK Equity | 1.9 |

| Zhihu HK | 2390 HK Equity | -1.6 |

| KE HK | 2423 HK Equity | -3.2 |

| Tencent Music Entertainment HK | 1698 HK Equity | 3.9 |

| Meituan HK | 3690 HK Equity | 0.1 |

| Hong Kong's Most Heavily Traded by Value | 1-Day Change (%) |

|---|---|

| TENCENT HOLDINGS LTD | 2.7 |

| ALIBABA GROUP HOLDING LTD | -3.4 |

| SEMICONDUCTOR MANUFACTURING | 8.2 |

| XIAOMI CORP-CLASS B | 2.8 |

| MEITUAN-CLASS B | 0.1 |

| WEIMOB INC | 25.4 |

| KUAISHOU TECHNOLOGY | -5.4 |

| JD.COM INC-CLASS A | -3 |

| TRIP.COM GROUP LTD | -0.1 |

| HONG KONG EXCHANGES & CLEAR | -0.9 |

| Shanghai and Shenzhen's Most Heavily Traded by Value | 1-Day Change (%) |

|---|---|

| SEMICONDUCTOR MANUFACTURIN-A | 10.3 |

| ZTE CORP-A | -1.1 |

| EAST MONEY INFORMATION CO-A | 1 |

| IEIT SYSTEMS CO LTD-A | 0.7 |

| GIGADEVICE SEMICONDUCTO-CL A | 0.9 |

| CONTEMPORARY AMPEREX TECHN-A | -2.6 |

| VISUAL CHINA GROUP CO LTD-A | 2 |

| RANGE INTELLIGENT COMPUTI-A | 1 |

| CAMBRICON TECHNOLOGIES-A | 6.3 |

| LEO GROUP CO LTD-A | 8.2 |

Last Night's Exchange Rates, Prices, & Yields

- CNY per USD 7.30 versus 7.30 yesterday

- CNY per EUR 7.59 versus 7.59 yesterday

- Yield on 10-Year Government Bond 1.70% versus 1.74% yesterday

- Yield on 10-Year China Development Bank Bond 1.78% versus 1.82% yesterday

- Copper Price -0.34%

- Steel Price -0.15%