Tariffs, Karaoke Performers, Donuts, & Capital Controls

5 Min. Read Time

We will be hosting a webinar on the reopening of China's economy and investing after COVID-19 on Thursday, May 14th at 8:30 am EST.

Please click here to sign up!

Key News

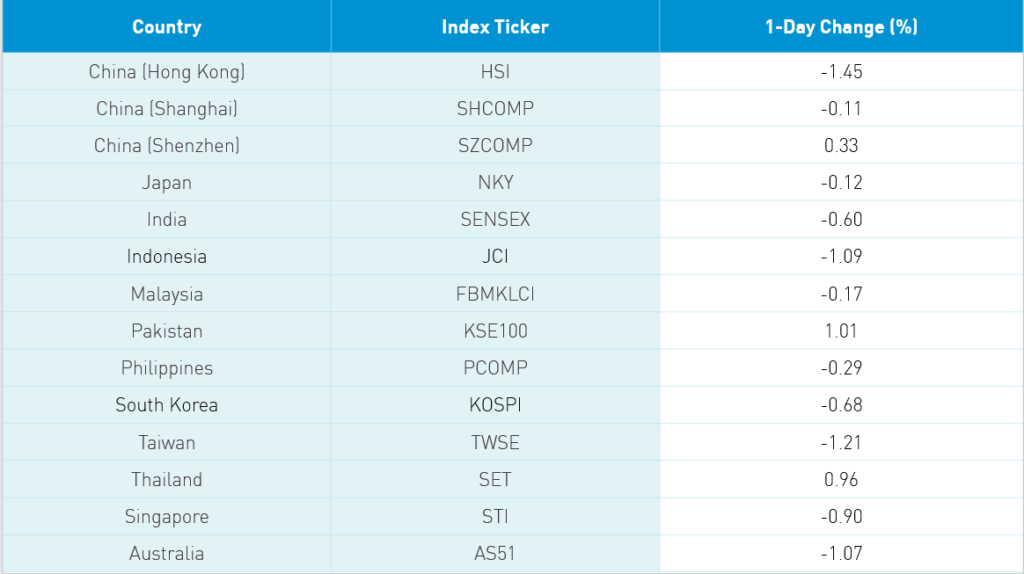

Asian equities ended the session lower on increased US-China political rhetoric and concerns of a coronavirus double dip. Wuhan will test its entire population after a man tested positive. Mainland China fell in the morning as concerns that a lack of investors and trading in B-shares, Chinese companies listed in US dollars, would result in the termination of the share class. However, B-shares are a tiny part of the Mainland market so this is not anything to be concerned about. However, Mainland markets rallied in the afternoon after it was announced that China will waive tariffs on 70 US goods (olive branch?).

Mainland and Hong Kong healthcare stocks rose on the Wuhan news. However, it is worth noting that China continues to return to life pre-quarantine. Despite the uptick in those sectors, Hong Kong was weighed down after a land sale at the old airport had a closing price that was well below estimates. Strong April smartphone sales lifted many players in the space and construction equipment makers were lifted by strong Mainland excavator sales in April, further evidence that construction projects are resuming.

Tencent was off -0.92% ahead of earnings, which will be announced after the close in Hong Kong tomorrow. Tencent traded three times as much as the second most traded stock Alibaba HK +0.5%. Meituan Dianping, the third most traded stock, rose +2.1% as analysts were largely unconcerned by competition from SF Express. Xiaomi was #4 on volume +1.22%.

One of our sharp-eyed brokers noticed that Weighted Voting Right companies’ secondary listings may be eligible for inclusion in the Hang Seng Index and Hang Seng China Enterprises Index. Hang Seng Indexes will announce its final decision on Monday, May 18. “WVR” refers to dual share class companies Facebook, Google, and Berkshire Hathaway where a single shareholder, usually the founder and/or CEO, owns shares with more voting rights than common shareholders. Many technology companies issue such shares so the CEO can implement a strategy without having to answer shareholders. Less than ideal for sure as SNAP gave common shareholders no voting rights at all. In addition to investment flows related to being added to the indices, the companies could be added to Southbound Connect. Current Hong Kong-listed companies include Alibaba, Meituan Dianping, and Xioami. Next Monday’s announcement could be a significant catalyst for the stocks.

The only endearing aspect of NYC’s Penn Station is the Tim Hortons’, a Canadian coffee and donut chain, located in the bowels of the building. While an arrestable offense in the Commonwealth of Massachusetts (the HQ of Dunkin’ Donuts), Tim Horton’s make a very good donut. Tim Hortons China announced an investment from online gaming and social media giant Tencent. I suspect there will be Tim Horton donut emojis coming to Tencent’s social media platform WeChat.

Ever send an email in an emotional state and quickly regret it? We all have, which is why I force myself to wait 24 hours if I find myself fired up over something. Last week, we noted the Federal Thrift Saving Plan had new board members appointed by the Trump administration. They didn’t waste time negating the move from MSCI EAFE Index (developed markets, i.e. Europe and Japan) to the MSCI All Country Ex-US Index (developed markets and emerging markets) due to the 11% exposure to China. The public document is rather scathing and blames China for coronavirus in its explanation of the “investment” decision despite the fact that YTD, 1-year, 3-year, and 5 year time frames the ACWI ex-US Index outperforms EAFE (over 10 years EAFE outperforms). Ultimately, the government can determine what it invests in like any investor. At the same time, removing great companies such as Tencent, Alibaba, and others makes no sense to me. The politicization of investing is a very dangerous trend. We should call it what it is: capital controls.

April PPI Year over Year:

-3.1% versus estimate -2.5% and March’s -1.5%

April CPI YoY:

3.3% versus estimate 3.7% and March’s 4.3%

Takeaway: PPI was off due to oil’s big drop while CPI continues to fall due to falling pork prices. Pork prices were off -7.6% which brought food prices -14.8% YoY or -3% month over month. Today’s release gives the PBOC the green light to continue easing measures due to the lack of inflation.

Tencent Music Entertainment Group (ticker TME) announced Q1 financial results after the US close. My favorite line from the release explaining a decline in operating profit “increased revenue sharing ratio to online karaoke performers”. Those greedy karaoke performers….

- Revenues increased +10% to $891mm (RMB 6.31 billion) from RMB 5.74B

- Online music subscription revenues grew +70% to $170mm (RMB 1.21B)

- Online paying music users +50.4% to 42.7mm, 657mm total users

- Cost of revenues +17% to $612mm (RMB 4.33B)

- Net profits $125mm (RMB 887mm) versus RMB 987

- EPS $0.80

H-Share Update

The Hang Seng opened lower and remained down for the count to close -1.45%/-356 index points at 24,245. Volumes were off -6% from yesterday while breadth was atrocious with only 4 advancers. The index was led lower by AIA -1.63%/-39 index points, HSBC -1.87%/-36 index points and Tencent -0.92%/-26 index points. Today’s best performer was China Mengniu Dairy (ticker 2319) +1.59%/+3 index points while Swire Pacific (ticker 19) -4.64%/-3 index points.Hong Kong and China-domiciled companies were both off -1.38% and -1.59%, respectively, using the HS HK 35 and HS China Enterprise indices as proxies. The mainland stocks listed in Hong Kong within the MSCI China All Shares Index lost -1.04%, led lower by real estate -2.51%, energy -2.46%, utilities -2.17%, materials -2.17%, financials -1.18%, industrials -1.16%, communication -1.1% and discretionary -0.25%. Healthcare had a strong day +1.24%, tech +0.54%, and staples +0.03%. Southbound Connect flows were light though Mainland investors bought the dip as buying activity outpaced selling activity on Southbound Connect. Volume leader Tencent had buyers outpace seller pre-earnings by a small margin, Meituan Dianping had buyers outpace sellers 3 to 2, and Semiconductor Manufacturing had buyers outpace sellers by a similar amount. Mainland investors bought $235mm worth of Hong Kong-listed stocks today as Southbound Connect trading accounted for 8% of Hong Kong’s turnover.

A-Share Update

The Shanghai & Shenzhen had a choppy day diverging -0.11% and +0.33%, respectively, on volumes down -12% from yesterday, to close at 2,891 and 1,810, respectively. Breadth was weak with 1,074 advancers and 2,612 decliners as small and mid-caps outperformed large caps. The Mainland stocks within the MSCI China All Shares Index gained +0.16%, led higher by\staples +1.04%, tech +0.5%, communication +0.19% and utilities +0.05%. Real estate fell -1.06%, and energy -0.69%. Northbound Connect had light/moderate volumes as Shenzhen Connect once again had higher volumes than Shanghai Connect. Volume leader Gree had buyers outpace sellers by a small margin as did Ping An while Kweichow Moutai had buyers outpace sellers 3 to 2. Foreign investors bought $247mm worth of Mainland stocks today as Northbound Connect accounted for just over 5% of the Mainland’s turnover.

Last Night's Prices & Yields

- CNY/USD 7.08 versus 7.10 yesterday

- CNY/EUR 7.70 versus 7.67 yesterday

- Yield on 1-Day Government Bond 0.83% versus 0.91% yesterday

- Yield on 10-Year Government Bond 2.66% versus 2.67% yesterday

- Yield on 10-Year China Development Bank Bond 3.01% versus 3.02% yesterday