Hong Kong Internet, Biden-Xi Virtual Summit, & NetEase Q3 Drive Rally

2 Min. Read Time

Key News

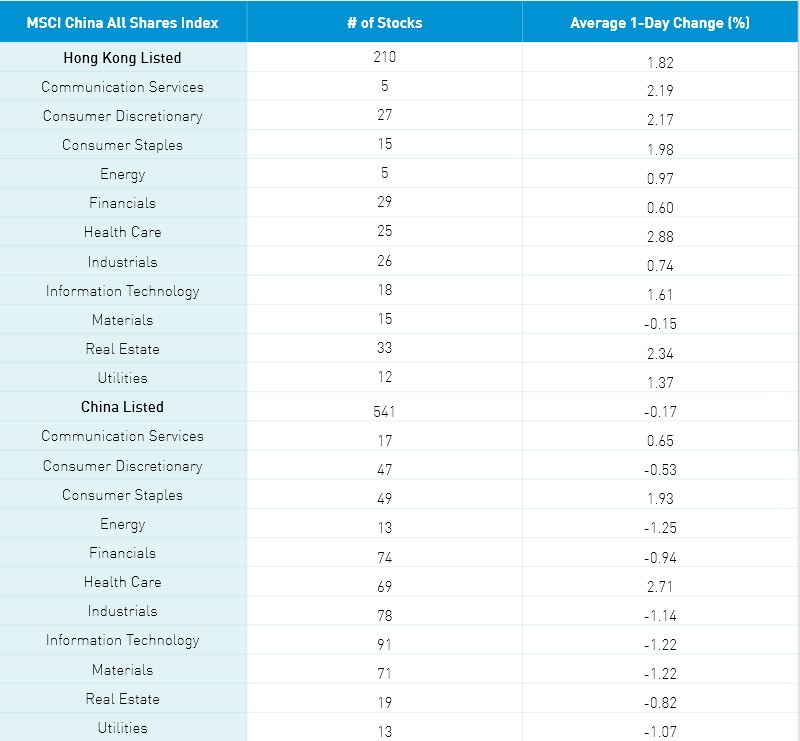

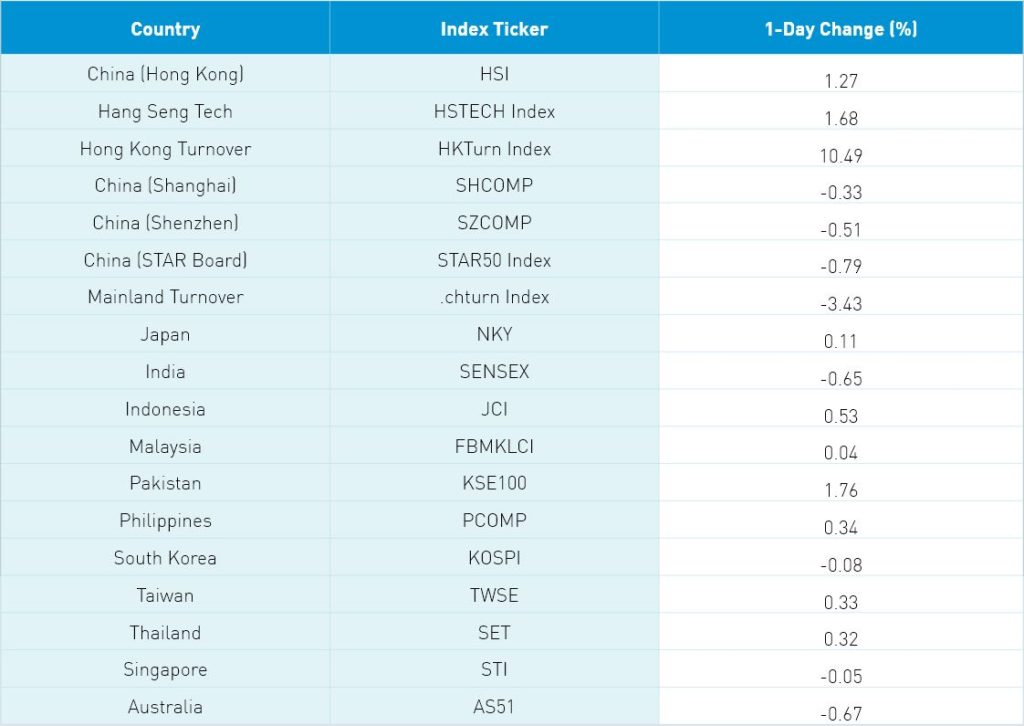

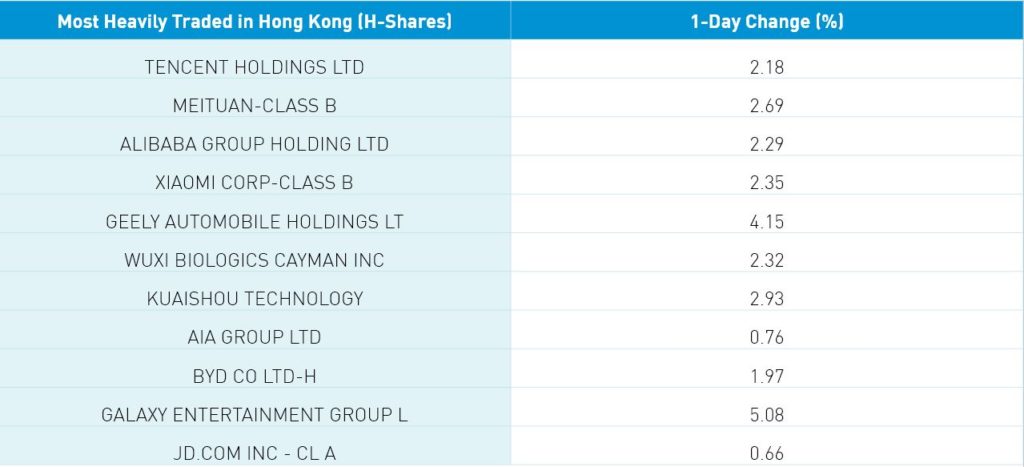

Asian equities had a mixed night on light volumes as Hong Kong outperformed, led by internet stocks. Hong Kong’s three most heavily traded stocks were Tencent, which gained +2.18%, Meituan, which gained +2.69%, and Alibaba HK, which gained +2.29%, driving the Hang Seng +1.27% while the Hang Seng Tech Index gained +1.68%. Hong Kong healthcare and real estate sectors gained +2.88% and +2.34%, respectively, followed by communication services, which gained +2.19%, and consumer discretionary, which gained +2.17%.

The Biden-Xi virtual summit went well enough and continued into overtime, providing a path for continued dialogue in the future. This should help alleviate the overhang of US-China political relations on Hong Kong and US-listed Chinese stocks.

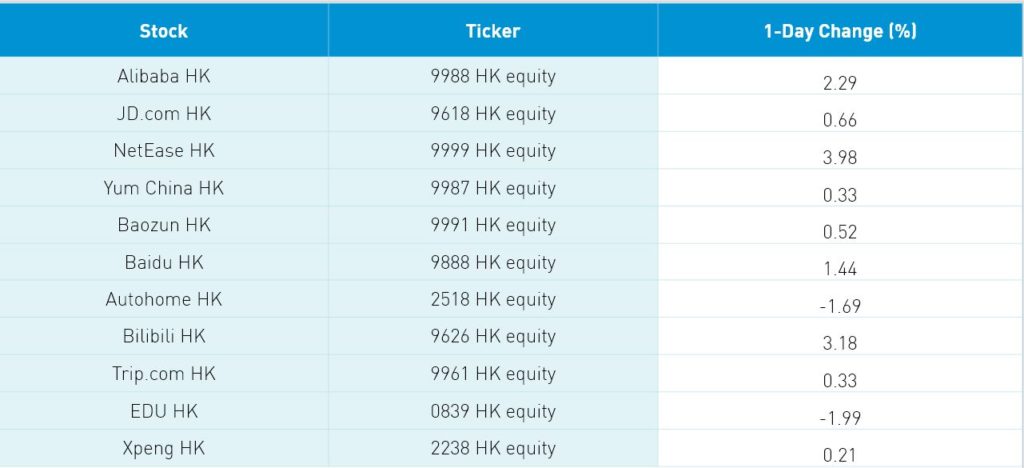

We also had NetEase’s Hong Kong listing rally +3.98% ahead of Q3 financial results, which were released after the Hong Kong close. The results were strong as revenues increased +18.9% year-over-year (YoY) to RMB 22.2B ($3.4B) versus analysts’ estimate of RMB 21.244B led by online gaming revenues, which climbed +14.7% YoY to RMB 15.9B ($2.5B). There was chatter that the new online game approvals could be eased in another sign that the regulatory cycle is coming to end.

We also had an editorial in the People’s Daily titled “Provide more financial support for the development of the digital economy” that spoke to the importance of the digital economy to the new economy.

One company that believes its stock is too cheap is Hong Kong-listed Razer (1337 HK), online gaming software and gear maker, which announced it will take itself private at a price of HKD 4 versus today’s close of HKD 2.82. It was somewhat surprising that we saw a net sale in Tencent by Mainland investors via Southbound Stock Connect, though Meituan was a net buy.

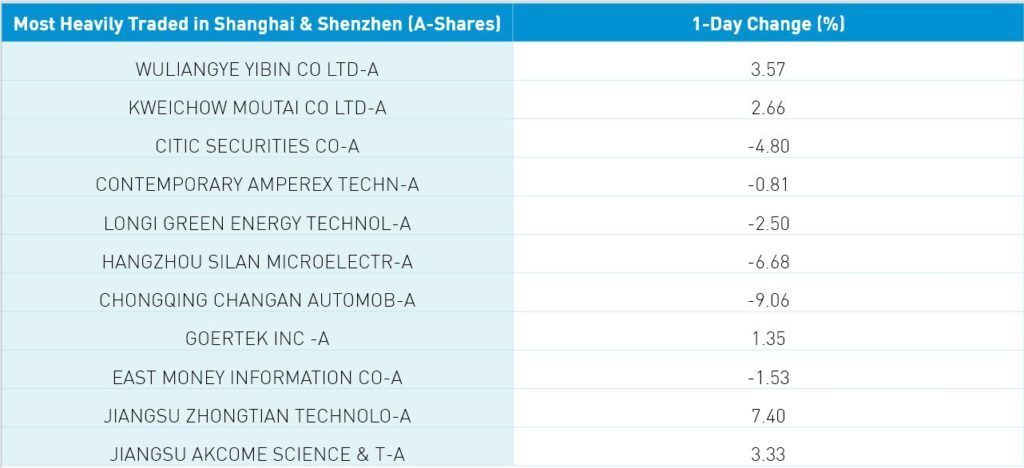

Hong Kong volumes were +10.49% from yesterday though only 77% of the 1-year average. Mainland markets gave up morning gains as stocks eased into the close with Shanghai falling -0.33%, Shenzhen down -0.51%, and the STAR Board falling -0.79%. Healthcare and staples had a strong day gaining +2.7% and +1.92%, respectively, as the latter's performance was driven by liquor stocks. Value stocks outperformed growth sectors as the clean technology ecosystem was soft on Elon Musk’s continued Tesla sales. Military/defense stocks were weak on Biden’s commitment to not support Taiwanese independence. Mainland volumes were off -3.43% from yesterday, which is 110% of the 1-year average. Foreign investors bought $657 million worth of Mainland stocks today via Northbound Stock Connect as Northbound trading accounted for 4.7% of Mainland turnover. CNY was off a touch while copper was off, and bonds rallied.

Sunday’s 60 Minutes had a good segment on the supply chain issues driven by US west coast ports and trucking industry structural issues. This is a big shift in the narrative that the problem was an Asia/China issue. Good to see it took some time for the truth to come out. However, the demand shock created by government stimulus was not examined.

Singapore-based E-Commerce company Sea (SE US) announced strong financial results before the US market open. Google, Singapore sovereign wealth fund Temasek, and consulting firm Bain & Company have been collaborating on Southeast Asia’s (SEA) internet economy report. This year’s report titled The Roaring ‘20s: The SEA Digital Decade is chock full of nuggets, most notably that SEA has 589 million people that will have spent $170B on E-Commerce in 2021 though that will grow to $1 trillion by 2030. The pandemic has been a clear catalyst for internet adoption and E-Commerce saw 80 million new users in 2020 and 2021.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.39 versus 6.38 Yesterday

- CNY/EUR 7.26 versus 7.31 Yesterday

- Yield on 10-Year Government Bond 2.92% versus 2.93% Yesterday

- Yield on 10-Year China Development Bank Bond 3.18% versus 3.19% Yesterday

- Copper Price -0.17% overnight