Why SOE ADR Delisting is a Good Thing, Real Estate Policy Lifts Sector, MSCI’s Quarterly Index Review, Week in Review

4 Min. Read Time

Week in Review

- Asian equities were largely higher this week as China released better-than-expected trade data, indicating that the global economy could be recovering somewhat from supply chain distress and inflationary pressure.

- China’s National Passenger Car Information Exchange Association announced that China auto sales increased +41% year-over-year in July.

- On Wednesday, China released inflation data for the month of July showing that the consumer price index (CPI) increased by only +2.9% year-over-year, compared to a CPI print of over 8% in the US.

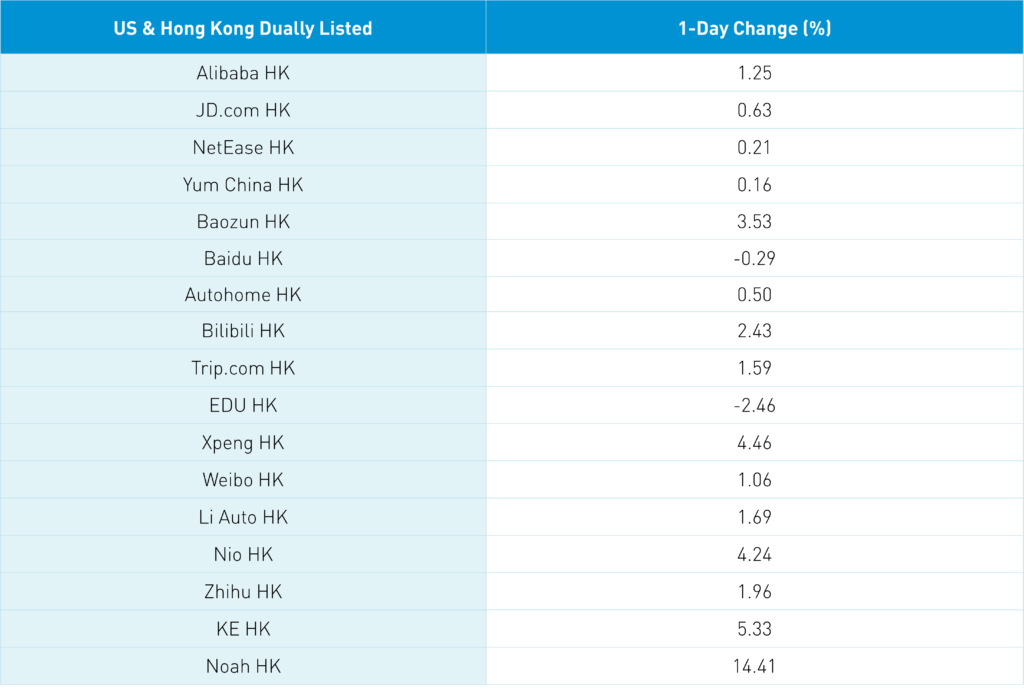

- Softbank reduced its position in Alibaba to 15% from 24% on Thursday, taking profits from its China E-Commerce investment after a difficult year for the tech investor.

Key News

This morning after the close in Hong Kong, five US-listed Chinese companies announced they will be delisting from the New York Stock Exchange (NYSE). The five companies are all State-Owned Enterprises (SOEs). We have long argued that a potential solution to Holding Foreign Companies Accountable Act (HFCAA) would be the delisting of SOEs as their audit reviews may indeed contain sensitive information. An SOE audit might include the amount of government subsidies to the companies. Private companies have long stated that they have nothing to hide from an audit review conducted by the Public Company Accounting Oversight Board (PCAOB). The China Securities Regulatory Commission (CSRC), China’s SEC, put out a statement this morning pointing out the obvious that the five US listings have little volume and account for very small percentage of the companies’ market cap. The CSRC also said that “We will maintain communication with relevant overseas regulatory agencies to jointly safeguard the legitimate rights and interests of enterprises and investors.”1 Market action indicates a lower opening for US-listed Chinese companies despite my strong belief that this could be a very good development for a solution to the HFCAA.

Asian equities were largely higher as Japan played catch up after yesterday’s market holiday while Thailand was on holiday for the Queen Sirkit’s Birthday. It was a quiet session as volumes in Hong Kong were low.

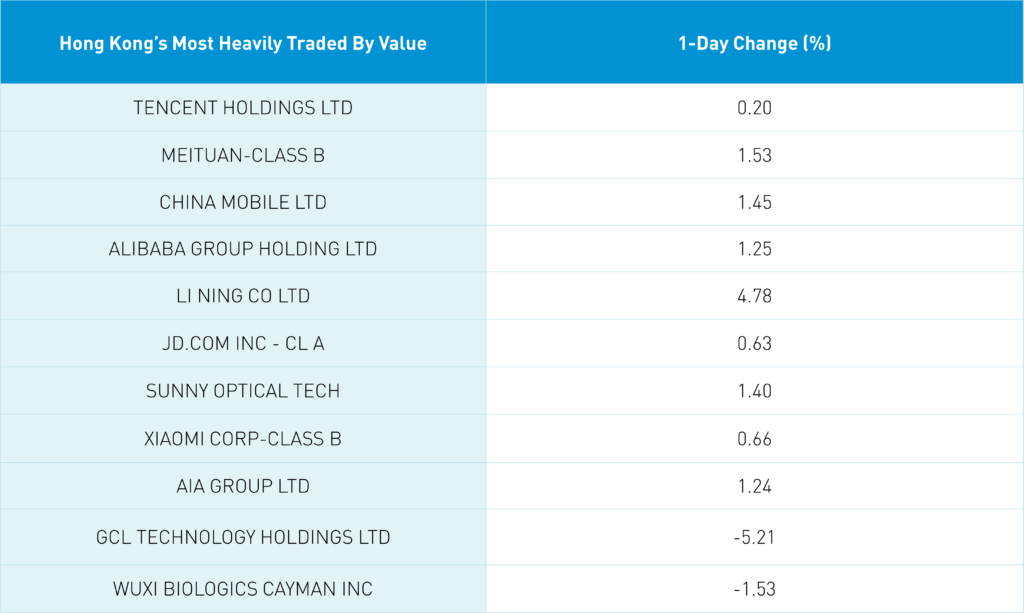

The most heavily traded stocks by value in Hong Kong were Tencent, which gained +0.2%, Meituan, which gained +1.53%, China Mobile, which gained +1.45%, Alibaba HK, which gained +1.25%, and Li Ning, which gained +4.78% after strong first half results. Energy was the top sector in both Hong Kong and Mainland China, gaining +1.8% and +2.29% in both markets, respectively, on firming prices and a data release showing that first half power consumption increased +6% year-over-year with a strong and a strong second half estimate.

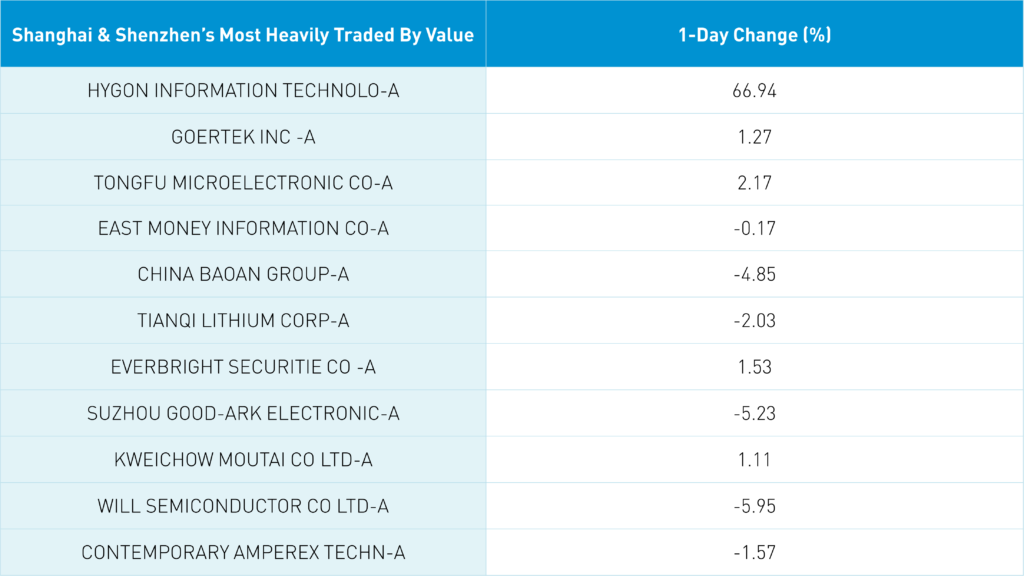

Mainland stocks were off as pre-weekend as profit-taking hit this week’s outperformers such as semiconductors. Computer component maker Hygon Information (688041 CH) soared +66% in its IPO today and was the most heavily traded Mainland stock overnight by value traded. Real estate had a decent day on the Mainland, where the sector gained + 1.22% as policy support is clearly coming for the space. We mentioned yesterday that several cities are curtailing their home buying restrictions to support collapsing sales.

After the close, July aggregate financing and loans came in well below expectations at RMB 756B versus the estimate of RMB 1.35T/June’s 5.17T and RMB 679B versus the estimate of RMB 1.125T and June’s RMB 2.81T. This release will garner significant attention from policy makers as rumors of a RMB 1 trillion rescue plan have been rumored.

After the US close yesterday, MSCI released its Quarterly Index Review, which will be implemented by asset managers at the close on August 30th. China’s weight within Emerging Markets is projected to increase from 33.5% to 33.8% as the number of stocks increases from 716 to 721. New additions include Tianqi Lithium, which is very popular foreign and domestically held stock. China’s 721 stocks account for 52% of MSCI EM’s 1,386 stocks. At some point, the numeric count will catch up with the percentage weight. One might argue China is becoming an asset class, requiring both a China and an EM ex-China strategy.

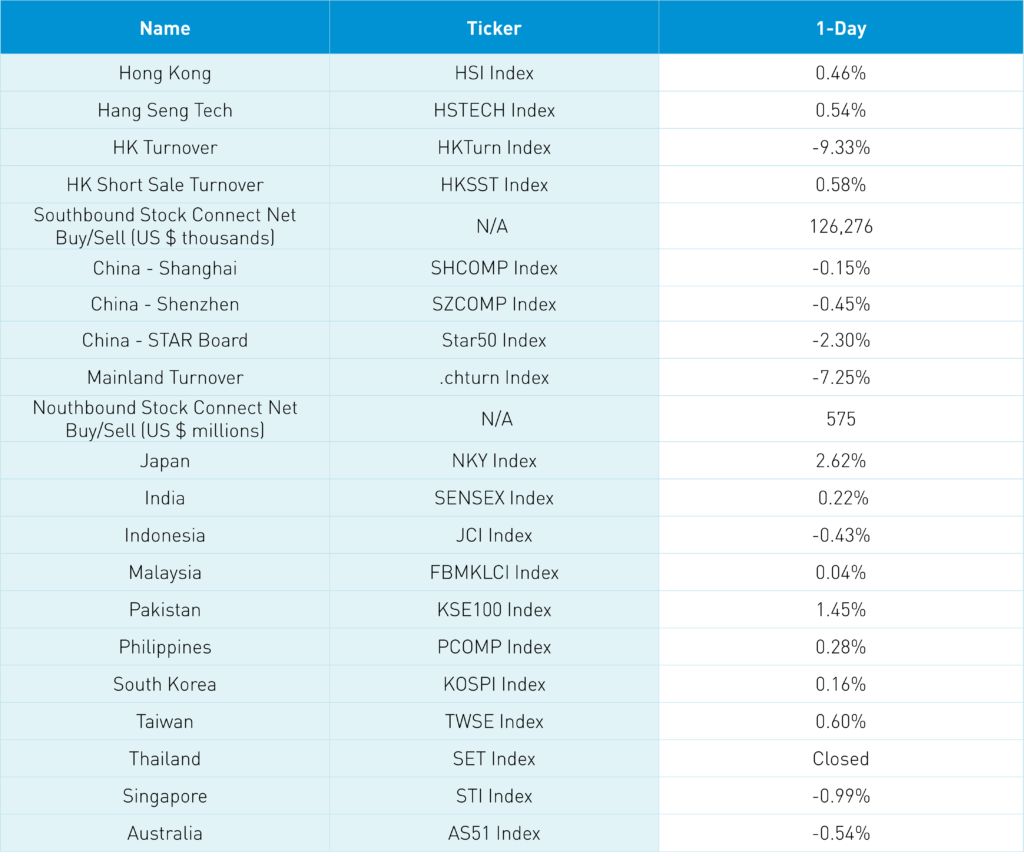

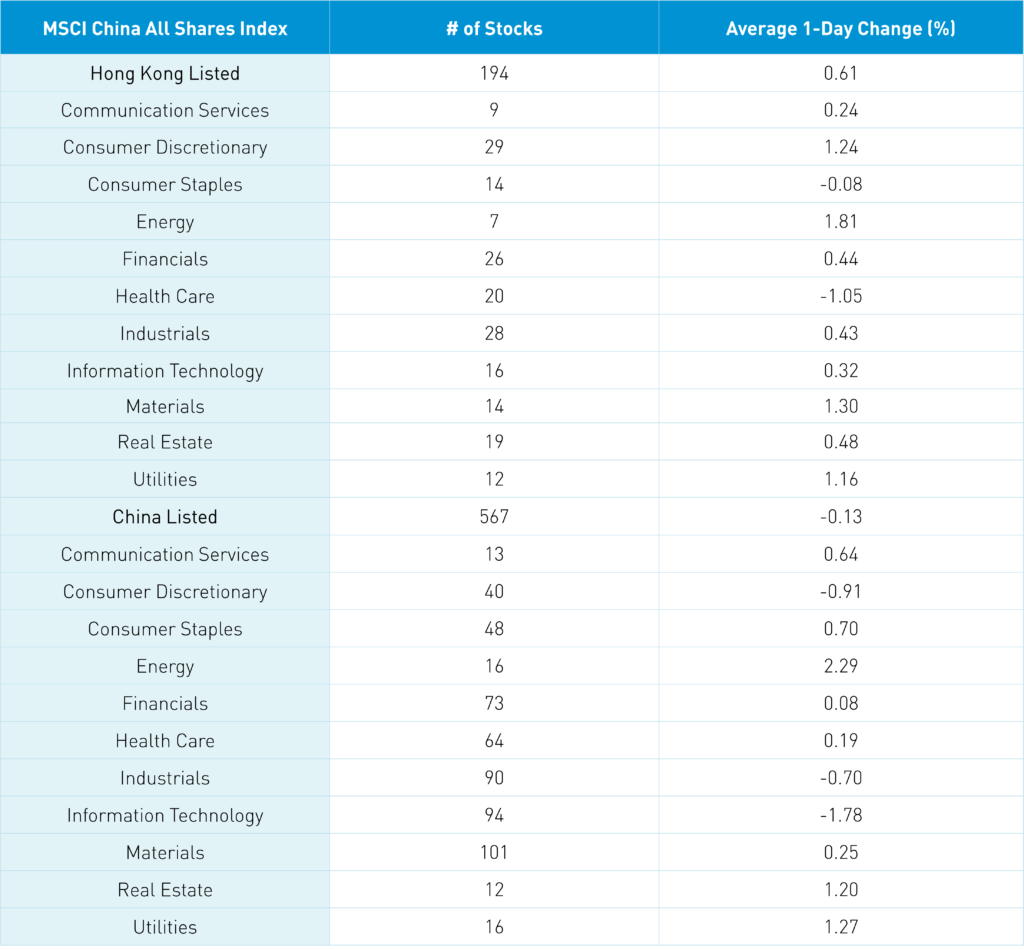

The Hang Seng and Hang Seng Tech indexes gained +0.46% and +0.54%, respectively, on volume that decreased -9.33% from yesterday, which is 56% of the 1-year average. 302 stocks advanced while 160 declined. Hong Kong short sale turnover increased +0.67%, which is 56% of the 1-year average as short sale turnover accounted for 16% of total turnover. Value factors outperformed growth factors as large caps edged above small caps. The top performing sectors overnight were energy, which gained +1.82%, materials, which gained +1.31%, and consumer discretionary, which gained +1.25% while healthcare was off -1.04% and consumer staples was down -0.08%. The top performing sub-sectors were materials, metal-related sectors such as iron, cobalt, and steel while online education and circuit boards were among the losers. Southbound Stock Connect volumes were light as Mainland investors bought a net $126 million worth of Hong Kong stocks net of sales with Tencent and Li Auto among the net buys while Meituan was a net sell.

Shanghai, Shenzhen, and the STAR Board were off -0.15%, -0.45%, and -2.3%, respectively, on volume that fell -7.25% from yesterday, which is 93% of the 1-year average. 2,110 stocks advanced while 2,326 stocks declined. Value factors outperformed growth factors today as large caps outpaced small caps. The top performing sectors were energy, which gained +2.28%, utilities, which gained +1.27%, and real estate, which gained +1.2%. Meanwhile, tech fell -1.79%, discretionary fell -0.91%, and industrials fell -0.71%. The top performing sub-sectors included coal, precious metals, and energy equipment while solar, semiconductors, and battery plays were among the losers. Northbound Stock Connect volumes were light to moderate as foreign investors bought $575 million worth of Mainland stocks today. Chinese Treasuries were flat, CNY eased -0.04% versus the US dollar to 6.74 while copper gained +1%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.74 versus 6.74 yesterday

- CNY/EUR 6.91 versus 6.97 yesterday

- Yield on 1-Day Government Bond 1.00% versus 1.03% yesterday

- Yield on 10-Year Government Bond 2.73% versus 2.73% yesterday

- Yield on 10-Year China Development Bank Bond 2.91% versus 2.91% yesterday

- Copper Price +1.00%

- "CSRC Official of Relevant Departments Answered Reporter Question Regarding Recent Decisions by A Few Chinese Companies to Voluntarily Delist from U.S. Exchanges," China Securities Regulatory Commission. August 11, 2022.