PBOC Cuts Deposit Rates, Reserve Requirement Cuts Likely In 2nd Half

3 Min. Read Time

Key News

Asian equities were broadly higher overnight, though South Korea was closed for the Memorial Day holiday.

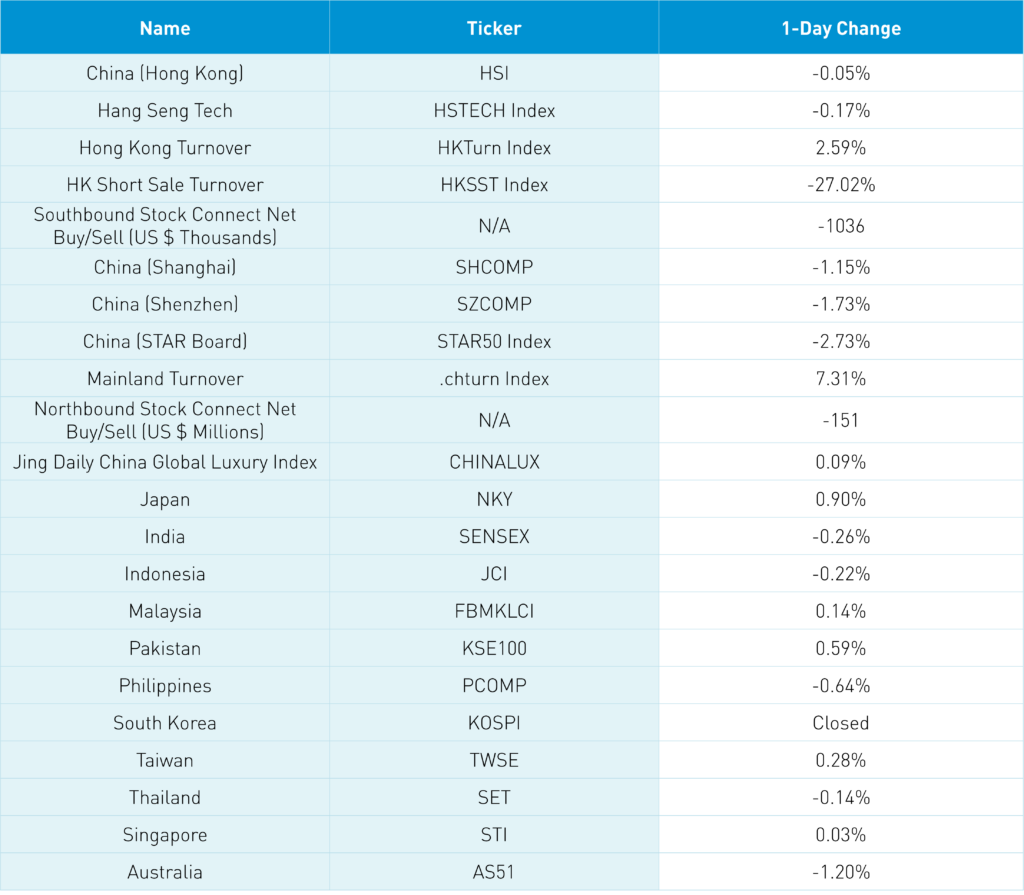

Hong Kong and Mainland China gave back mid-morning gains to close lower, as the Hang Seng Index opened higher by +1.41%, but closed lower by -0.05%. The most important news overnight came at 3:30 pm, after the Mainland’s close, when Bloomberg News reported that the PBOC would cut banks’ deposit rates, which led to a small rally into Hong Kong’s close. Mainland media also reported that the 2nd half of 2023 may see interest rate and bank reserve requirement ratio cuts.

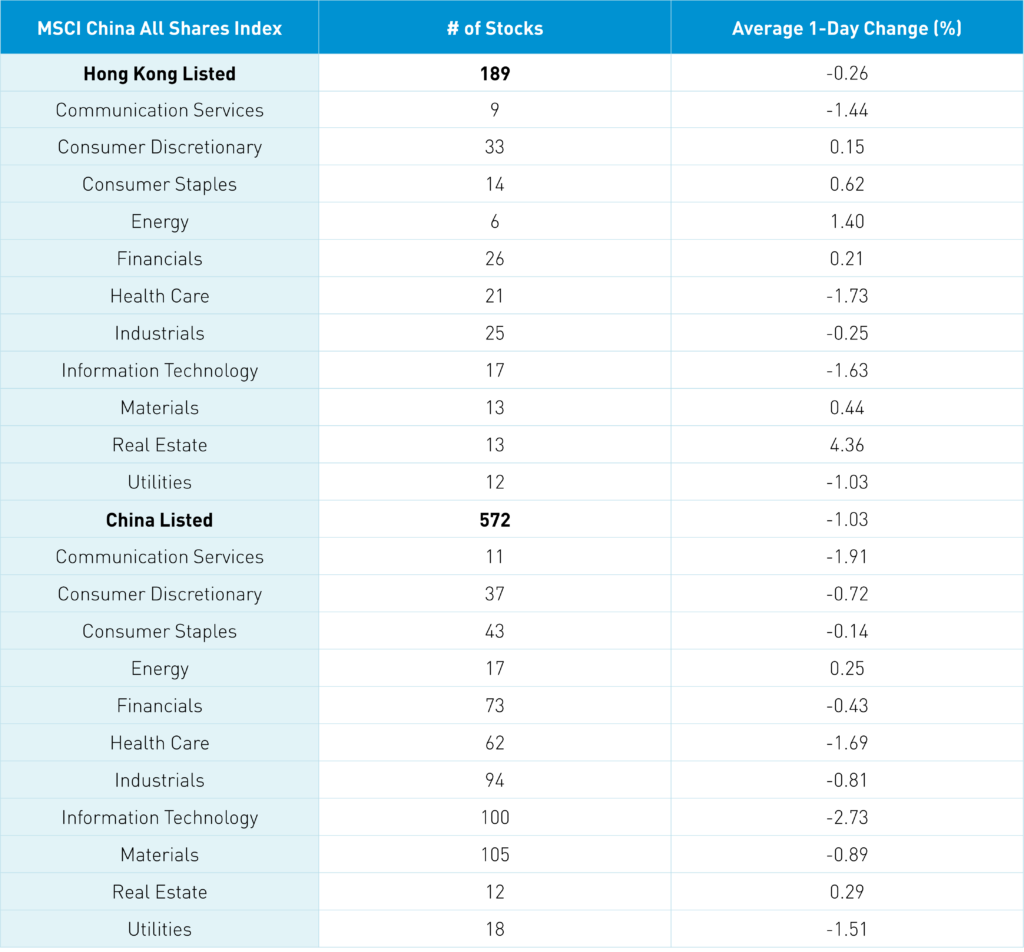

Real estate outperformed in Hong Kong, where it gained +4.38%, and Mainland China, where it gained + 0.27% on Mainland media reports that megacities dubbed Tier 1, which include Beijing, Shanghai, and Shenzhen, will see property support via loosening buying curbs. Cutting the bank deposit interest rate frees up cash for the banks to lend, which makes them more profitable. The news needs to become a reality because investors are impatient with the talk after a moderation in the recovery in April and May. Exhibit A of this impatience would be another strategist reducing, though not eliminating, their China overweight overnight. This was not front page news, but there remains concern about local governments’ balance sheets due to their historic reliance on land sales for revenue as relaxing property buying curbs would help them.

A meeting between US State Department officials and China’s Vice Foreign Minister was described as “candid, constructive and fruitful communication on promoting the improvement of Sino-US relations” by the China foreign ministry. Another indication of green shoots on US-China political relations as US officials finally visit China following the release of the CIA Director’s China visit. The Shanghai and Shenzhen closed just below the 3,200 and 2,000 levels, while the Hang Seng closed above 19,000. The National Team, mega-institutional investors in China, will likely support these levels as they tend to buy low and sell high. Investors did not appear overly impressed with Apple’s VR headset as their Asia supply chain was off.

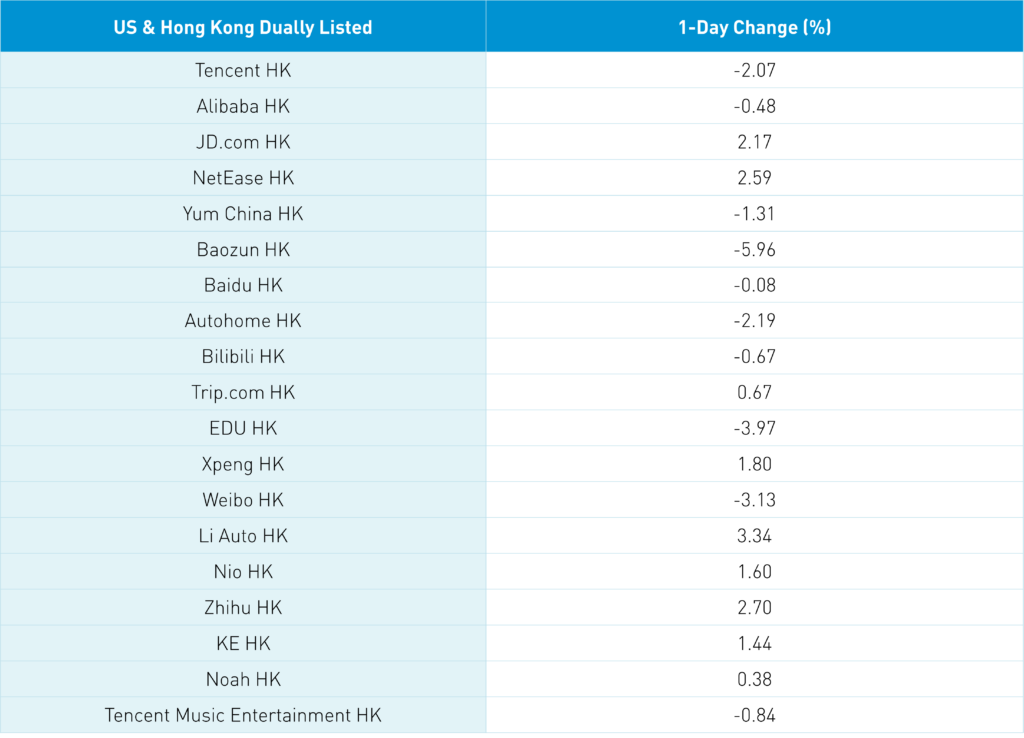

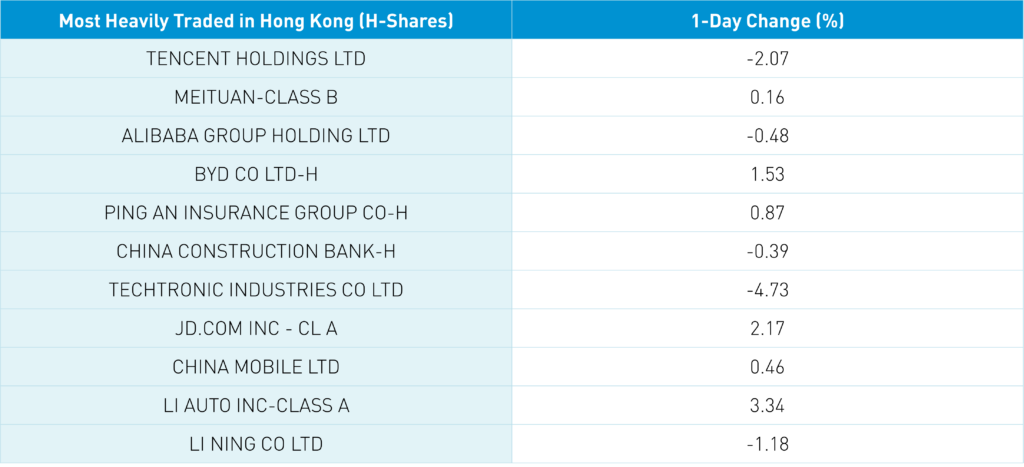

Also weighing on Mainland China and Hong Kong technology was a short seller report on power tool maker Techtronic Industries (669 HK), which fell -4.73% overnight. I’ve never heard of the short seller, though it shows the market sentiment's fragility. Yesterday, we mentioned the large $1.4 billion of net buying of Hong Kong stocks by Mainland investors via Southbound Stock Connect. In a head-scratcher, Mainland investors sold a net -$1.04 billion worth of Hong Kong stocks overnight. Meanwhile, short turnover in two large Hong Kong-listed China ETFs fell from 77% and 74% yesterday to 27% and 20% today. Not sure if the two are related, but the flow reversal is hard to explain. JD.com gained+2.17%, outperforming Hong Kong internet stocks as their 618 sales festival continues. CNY and the Asia Dollar Index were off small versus the US dollar.

The Hang Seng and Hang Seng Tech indexes eased -0.05% and -0.17%, respectively, on volume that increased +2.59% from yesterday, which is 86% of the 1-year average. 223 stocks advanced, while 270 declined. Main Board short turnover declined -27.05% from yesterday, which is 86% of the 1-year average, as 17% of turnover was short turnover. The value factor outperformed the growth factor as small calls outperformed large caps. The top-performing sectors were real estate, which gained +4.38%, energy, which gained +1.41%, and consumer staples, which gained +0.63%. Meanwhile, healthcare fell -1.72%, technology fell -1.61%, and communication services fell -1.43%. The top-performing subsectors were real estate, autos, and energy. Meanwhile, semiconductors, software, and pharmaceuticals were among the worst. Southbound Stock Connect as Mainland investors sold $1.04 billion worth of Hong Kong stocks as Kuaishou was a small net buy, and Tencent and Meituan were small net sells.

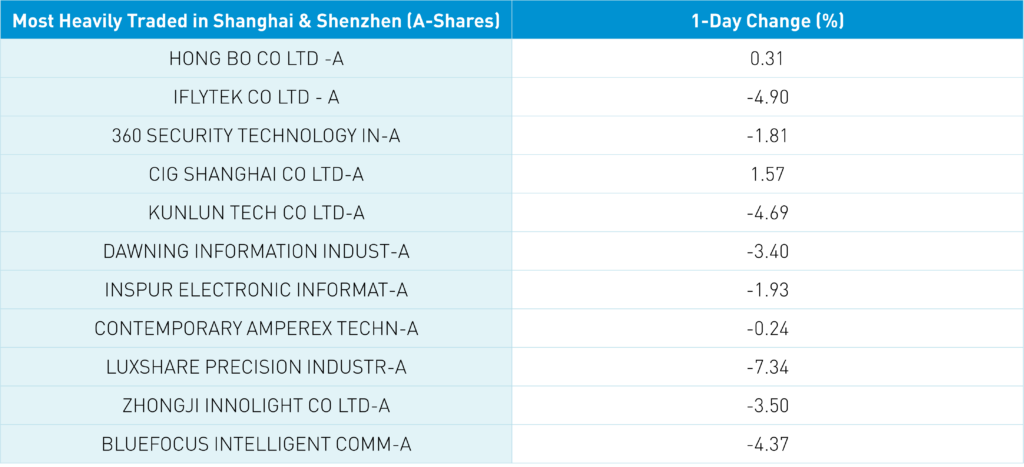

Shanghai, Shenzhen, and the STAR Board fell -1.15%, -1.73%, and -2.73%, respectively, on volume that increased +7.31% from yesterday, which is 101% of the 1-year average. 631 stocks advanced, while 4,134 stocks advanced. Meanwhile, value factors “outperformed" (i.e. fell less) than growth factors, while large caps “outperformed” small caps. Real estate and energy were the only positive sectors, gaining +0.27% and +0.23%, respectively. Meanwhile, technology fell -2.75%, communication services fell -1.93%, and healthcare fell -1.71%. The top-performing subsectors were household products, motorcycles, and coal, while electronic components, internet, and software were among the worst. Northbound Stock Connect volumes were moderate/high as foreign investors sold a net -$151 million worth of Mainland stocks. Kweichow Moutai was a large net buy, while LONGi Green Energy and Ping An Insurance were small net sells. CNY and the Asia Dollar Index eased versus the US dollar while Treasury bonds rallied. Meanwhile, copper and steel rallied.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.12 versus 7.12 yesterday

- CNY per EUR 7.61 versus 7.61 yesterday

- Yield on 10-Year Government Bond 2.68% versus 2.69% yesterday

- Yield on 10-Year China Development Bank Bond 2.83% versus 2.84% yesterday

- Copper Price +0.73% overnight

- Steel Price +0.47% overnight