Ant Group’s STAR Board Listing Approved, RMB Moves Higher

3 Min. Read Time

Key News

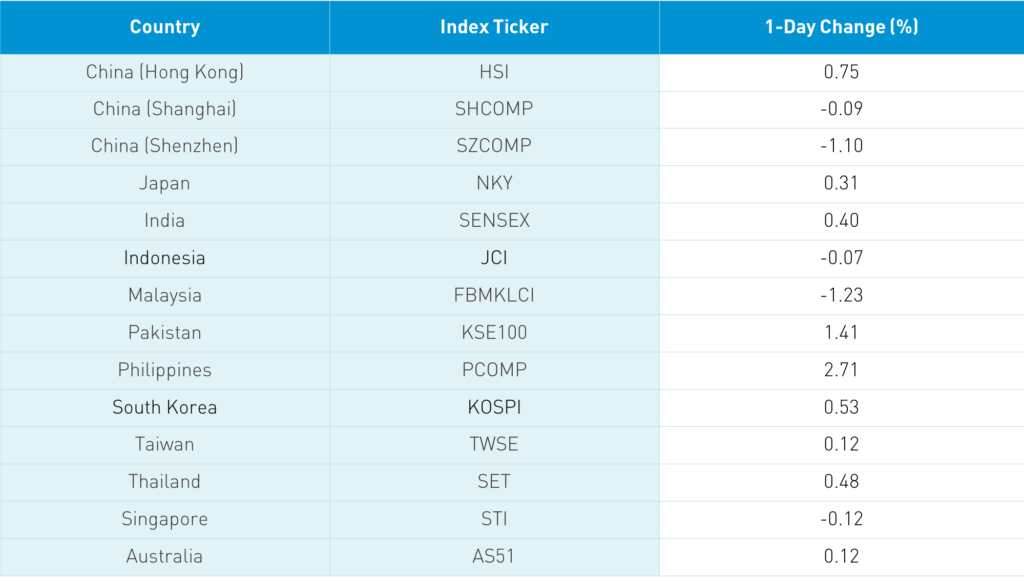

Asian equities were largely higher on anemic volumes driven by US stimulus hopes, though Mainland China was a bit of a laggard today. Hong Kong had a better day with the Hang Seng Index up +0.75%, led by volume leaders Tencent, which rose +0.35%, Alibaba Hong Kong, which rose +0.27%, Meituan Dianping, which gained +3.14%, Wuxi Biologics, which gained +11.61% on positive earnings and positive management comments on the firm’s coronavirus vaccine, Xiaomi, which was up +0.9%, China Mobile, which was up +3.9% on positive earnings, and Ping An Insurance, which rose +0.12%.

Healthcare was a strong performer in both Hong Kong and the Mainland on the Mainland statement that strong progress is being made on a coronavirus vaccine, with 13 trials taking place, four of which involve human testing. Separately, a Mainland research firm reported that Phase 3 trials on 9,000 Brazilians using Sinovac Biotech’s coronavirus vaccine are going well. Full results won’t be released until all 13,000 participants' results are available. Though Telecom was higher on the China Mobile earnings and the announcement on supportive policies, tech was off on news that Sweden won’t use ZTE and Huawei gear. Tech weakness led to a Mainland sell-off in growth names and recent winners.

The renminbi had a very strong day, appreciating 0.33% versus the USD. For US investors in Chinese A-Shares, the positive currency offsets today’s equity weakness. I still have no biters when I mention Chinese fixed income, though the yields are high in relative terms. I also noticed that Copper popped +1.28% overnight, while Baozun’s Hong Kong listing was up +5%. Baozun is an interesting company as it helps foreign firms navigate and sell via e-commerce in China. The chatter of strong e-commerce sales is likely to lead to some connecting the dots on how Baozun might be a beneficiary.

This morning, the South China Morning Post reported that Ant Group’s STAR Board IPO has been approved by the Mainland regulator. According to Bloomberg, the CSRC’s Weibo account reported the news. The exchange had previously approved the IPO, though the green light from the CSRC means it is game on. We still don’t know the exact timing, but we should see an updated Ant Group Hong Kong filing by week’s end, followed by a week of fundraising. The earliest would likely be the week of November 2nd, though the week of November 9th is highly likely.

For investment professionals, having a Bloomberg terminal is an indispensable tool. However, at $25k a year, it is an expensive one. It has an amazing amount of data, analytics, and exceedingly popular instant messaging functionality. I stumbled upon an analysis of the “Top 20 Fund Managers in Emerging Markets”. How these managers were chosen wasn’t clarified, and not one had a China allocation equal to the MSCI Emerging Market’s China weight. Not one! In 2019, China was one of the best performing EM countries, providing plenty of time to play catch up, though not one matched the weight in 2020. What isn’t shocking are the active EM managers allocating to “New China” stocks versus “Old China” stocks. Do we need to pay a manager for the most obvious trade in EM? I think not.

A Mainland media source noted that profits at 97 State-Owned enterprises rose +4.3% to $30.6B. Growth was driven by manufacturing-oriented companies, while energy and chemical companies lagged.

US-listed online education firm GSX is off -22% pre-market on several analyst downgrades and price cuts, while chatter is that revenues expectations appear high.

H-Share Update

The Hang Seng opened higher and stayed there up +0.75%/+184 index points to close at 24,754. Volume picked up 10% though still below the 1-year average, while breadth was positive with 28 advancers and 19 decliners. The 204 Chinese companies listed in Hong Kong rose +0.89%, led by health care +3.54%, discretionary +2.17% and staples +0.89%, while industrials lagged -0.83%, real estate -0.77% and tech -0.69%. Southbound Connect volumes were light as Mainland investors bought $353mm of Hong Kong stocks as Southbound trading accounted for 9.4% of Hong Kong turnover.

A-Share Update

Shanghai & Shenzhen were off -0.09% and -1.1% to close at 3,325 and 2,254 respectively. Volume increased +37% but was still well off the 1-year average while breadth was with only 742 advancers and 3,025 decliners. The 517 Mainland stocks within the MSCI China All Shares gained +0.02%, led by financials +1.43%, real estate +0.55%, and discretionary +0.48%, while tech -1.69%, industrials -0.89% and materials -0.28%. Northbound Stock Connect volumes were light as Foreign investors sold a healthy $1.04B as Northbound trading accounted for 6.1% of Mainland turnover.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.66 versus 6.68 yesterday

- CNY/EUR 7.90 versus 7.90 yesterday

- Yield on 1-Day Government Bond 1.35% versus 1.34% yesterday

- Yield on 10-Year Government Bond 3.19% versus 3.20% yesterday

- Yield on 10-Year China Development Bank Bond 3.72% versus 3.74% yesterday