Hong Kong Sees Profit Taking As Autohome Beats Estimates

4 Min. Read Time

Key News

Asian equities, except for Taiwan, the Philippines, and South Korea, had a rough night as the US dollar strengthened versus Asian currencies.

Hong Kong was led lower by profit-taking on growth stocks that outperformed during the rally, on volume that was +13% higher than yesterday. Yesterday and today’s pullback should not be surprising based on the velocity of the rally, which we delve into below. It was a fairly quiet night from a news perspective, though reports that the US will prevent Huawei from buying Nvidia and Qualcomm chips weighed on Chinese semiconductor stocks, though arguably, they are beneficiaries.

The electric vehicle (EV) ecosystem was off as April's preliminary retail car sales release of 706,000 units sold disappointed, declining -2% year-over-year (YoY). This comes after March auto sales overachieved, increasing +6% YoY.

The front page of the China Securities Journal spoke to the potential for another cut to banks' reserve requirement ratio (RRR) and additional interest rate cuts. However, it is hard to see the latter occurring until the Fed starts to cut.

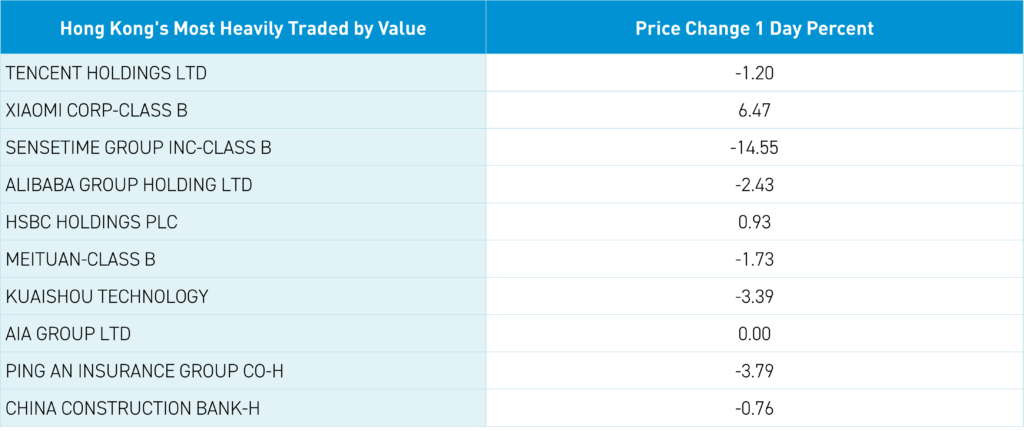

Hong Kong’s most heavily traded stocks by value were Tencent, which fell -1.2%, Xiaomi, which gained +6.47%, Sense Time, which fell -14.55% after a massive AI-fueled buying frenzy, Alibaba, which fell -2.43%, HSBC, which gained +0.93%, Meituan, which fell -1.73%, Kuaishou, which fell -3.39%, AIA, which was flat, Ping An Insurance, which fell -3.79%, China Construction Bank, which fell -0.76%, and Hong Kong Exchanges & Clearing, which fell -3.01%.

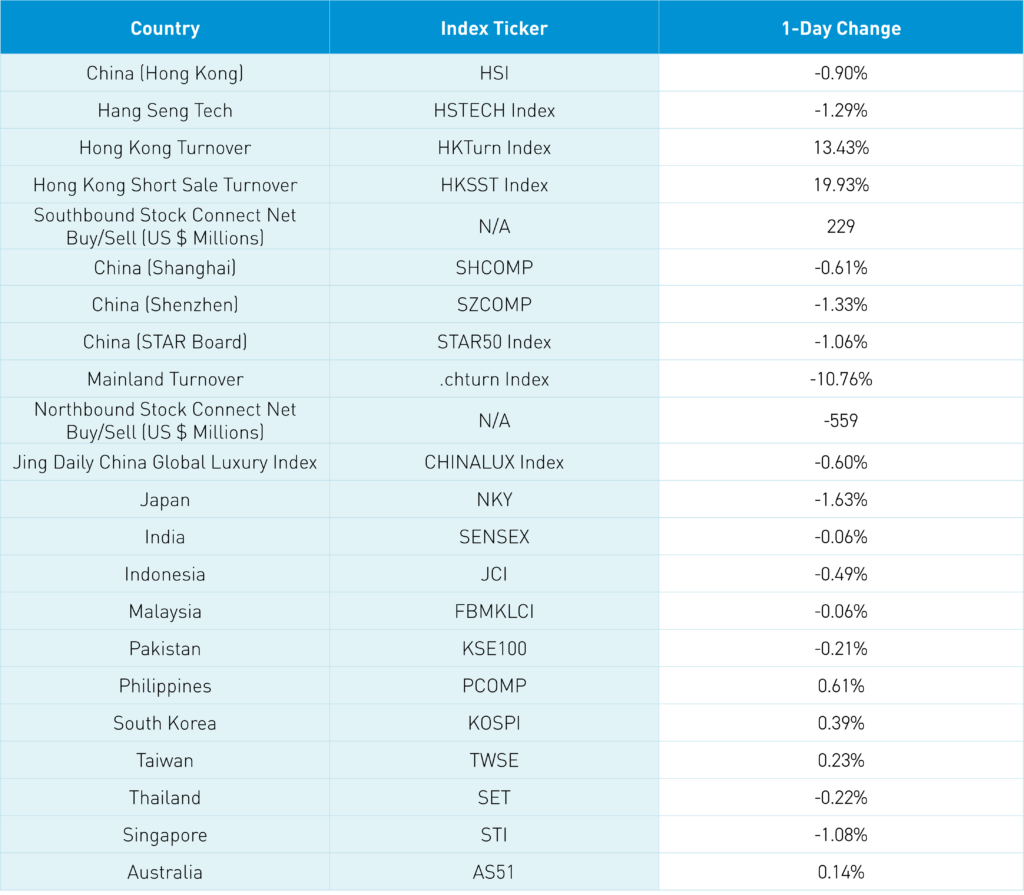

Real estate was whacked -4.45% in Hong Kong and -3.12% in Mainland China on profit-taking from tis recent bounce, though these companies trade like micro-caps. Mainland investors bought the Hong Kong dip via Southbound Stock Connect with an average of $229 million worth of net buying today. Mainland China was off, and foreign investors sold a decent amount of Mainland stocks, to the tune of -$559 million. The National Team’s two favorite mainland-listed ETFs had below-average volume.

Skepticism, skepticism, skepticism! After a debilitating decline from February 2021, the skepticism around the China rally is understandable. Rebuilding investor trust and confidence could take years, which is why investors should be excited, as fear and skepticism are the foundation for building bull markets. China’s rally following January’s derivative-induced meltdown has been impressive. No one would believe the returns in US dollars since January 31st, through yesterday's close: Shanghai Composite up +12%, Shenzhen Component up +15%, Hang Seng up +19%, and Hang Seng Tech up +30%. This is compared to the S&P 500's gain of +7%, the Nasdaq 100's gain of +5%, MSCI Japan's gain of +3%, and MSCI India's gain of +4%. Our argument has been that there is always a rebound after a liquidation event. Why not take some profits in US tech, India, and Japan and buy China? Not everything, but just a piece. What could turn the short-term rally into something with legs? This is what should be on investors' minds.

Today, Chinese companies bought back stock and pay dividends while the National Team bought ETFs. This should sound familiar to investors in Japan, where the government’s push to enact similar reforms ended the 25-year bear market (It is funny that no one uses the term "National Team" to explain the Japanese government’s ETF purchases).

We also have China’s economy slowly rebounding. Not one of 30 economists polled predicted China’s GDP would grow 5.3% in Q1 2024. They were skeptical! Policy amplification is occurring with July’s Third Plenum on the horizon. Next week, Q1 financial results from the largest internet companies will kick off.

This morning, online car sales platform, similar to Carvana in the US, Autohome (ATHM) beat analyst expectations on revenue, adjusted net income, and adjusted earnings per share (EPS). Autohome is a small company that I am using as an example of "out of sight & out of mind", as the stock went from a peak of nearly $140 to $27 today, with a P/E of 11. Anyway, I am saying that conditions overall may have changed for the better, which could help the rally continue.

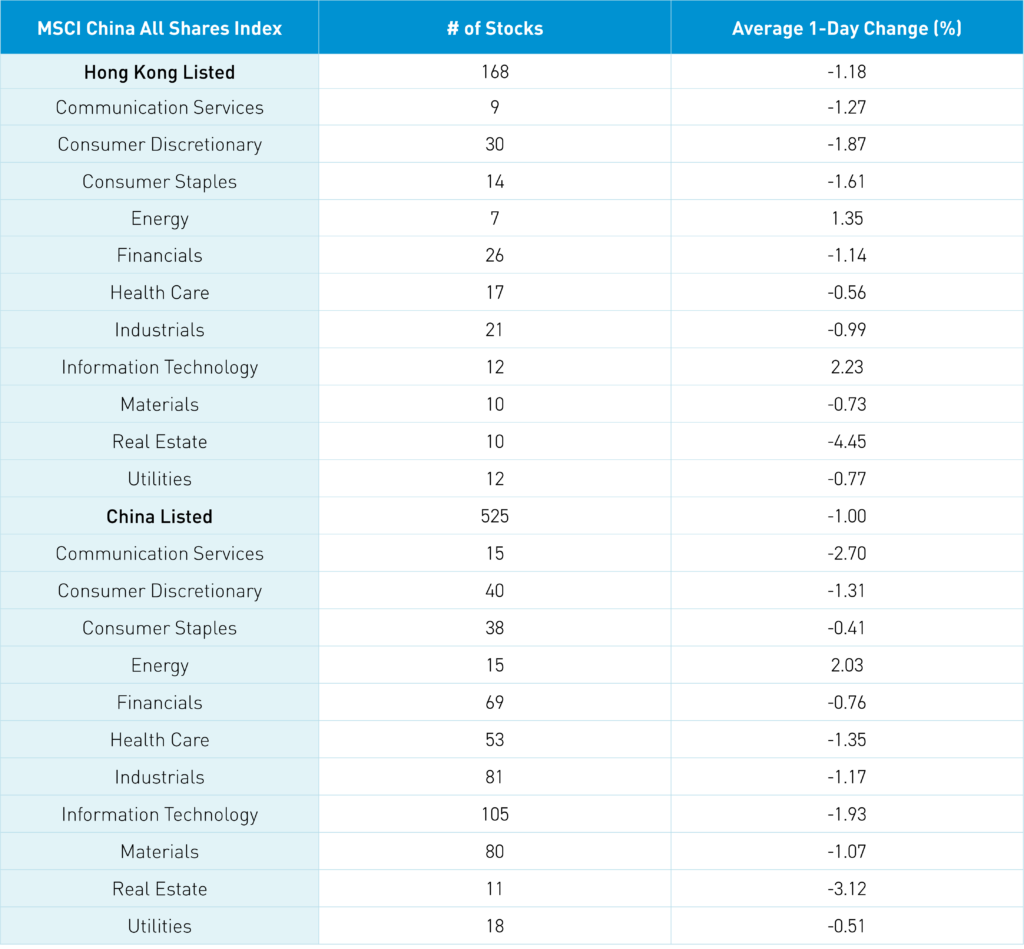

The Hang Seng and Hang Seng Tech indexes fell -0.9% and -1.29%, respectively, on volume that increased +13.43% from yesterday, which is 130% of the 1-year average. 98 stocks advanced, while 384 stocks declined. Main Board short turnover increased by +19.93% from yesterday, which is 117% of the 1-year average, as 16% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). All factors were negative, as the value factor fell slightly less than the growth factor, as large caps “outperformed” (i.e. fell less than) small caps. Technology and Energy were the only positive sectors, gaining +2.23%, and +1.35%, respectively, while Real Estate fell -4.45%, Consumer Discretionary fell -1.87%, and Consumer Staples fell -1.61%. The top-performing subsectors were technical hardware, energy, and household products. Meanwhile, semiconductors, real estate, and diversified financials were among the worst-performing subsectors. Southbound Stock Connect volumes were high as mainland investors bought a net $229 million worth of Hong Kong-listed stocks and ETFs, including Li Auto and China Mobile. Meanwhile, Xiaomi was a small net sell, and Tencent and HSBC had moderate/large net sells.

Shanghai, Shenzhen, and the STAR Board fell -0.61%, -1.33%, and -1.06%, respectively, on volume that decreased -10.76% from yesterday, which is 102% of the 1-year average. 1,027 stocks advanced, while 3,959 stocks declined. The value factor and large caps fell less than the growth factor and small caps. Energy was the only positive sector, gaining +2.02%. Meanwhile, Real Estate fell -3.13%, Communication Services fell -2.71%, and Technology fell -1.95%. The top-performing subsectors were coal, agriculture, and shipping. Meanwhile, internet, real estate services, and software were among the worst-performing subsectors. Northbound Stock Connect volumes were moderate as foreign investors sold a net -$559 million worth of Mainland stocks, including PAB, Nari-Tech, and Zhongji Innolight. However, Inovance and Mindray were small net buys. CNY and the Asia Dollar Index were off versus the US dollar. Treasury bonds were sold. Copper and steel fell.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.22 versus 7.21 yesterday

- CNY per EUR 7.76 versus 7.76 yesterday

- Yield on 10-Year Government Bond 2.29% versus 2.29% yesterday

- Yield on 10-Year China Development Bank Bond 2.39% versus 2.38% yesterday

- Copper Price -1.11%

- Steel Price -0.72%