Export/Import Data Highlight China/Global Growth, Internet Regulator Opines on Anti-Competitive Measures

3 Min. Read Time

Upcoming Webinar

Join us on Tuesday April 20th at 11:00 am EDT for our event:

Diving Into Dividends: 3D/L Capital Management co-CIOs Make the Case for Yield

Click here to register.

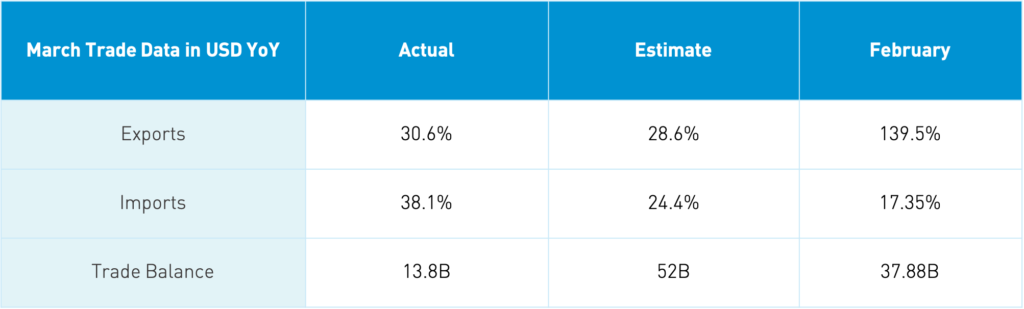

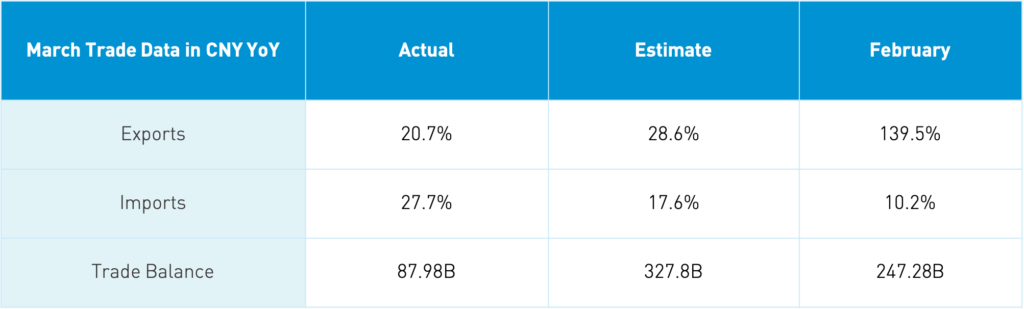

March Export/Import Data Release

Takeaway: China’s imports beat expectations while exports were a touch light in a late morning release. Exports to the US grew +53.3% YoY to $38.66B while EU exports grew +45.9% to $36.56B. US imports increased 75% YoY to $17.29B while EU imports increased 33.9% YoY. Soybean imports have increased +19% YTD to 7.77mm tons while copper exports increased +11.7% YTD to 1.44mm tons. Steel exports YTD are up +38.4% to $7.85B while aluminum exports are up +22.6% to $3.94%B. It’s worth noting that coal imports are off -31.7% YTD. As the middle person in global trade due to being the world’s factory, the Chinese data is important to monitor. The import data shows the resiliency of China’s economy while the export data is indicative of the recovery in the global economy. I expect the export data to increase rapidly in the months to come as the global economy reopens.

Key News

The State Administration for Market Regulation (SAMR) released a statement on how Chinese internet companies can avoid being fined like Alibaba. The companies are being ordered to play nice in the sandbox and remove anti-competitive practices such as banning their competitors on their platforms and forcing vendors to choose one firm. “Fair competition” was reiterated several times in the release, telling us what the regulator wants to see. The companies have a month to remove anti-competitive measures, or they may be fined like Alibaba was. The statement wasn’t released until 3:00 pm local time though news appears to have weighed on the companies in the afternoon session. I’ve read the statement several times, which leaves me a little surprised at the market’s reaction. It is worth noting that Meituan and Tencent were bought in modest size via Southbound Connect by Mainland investors. Maybe they agree with me.

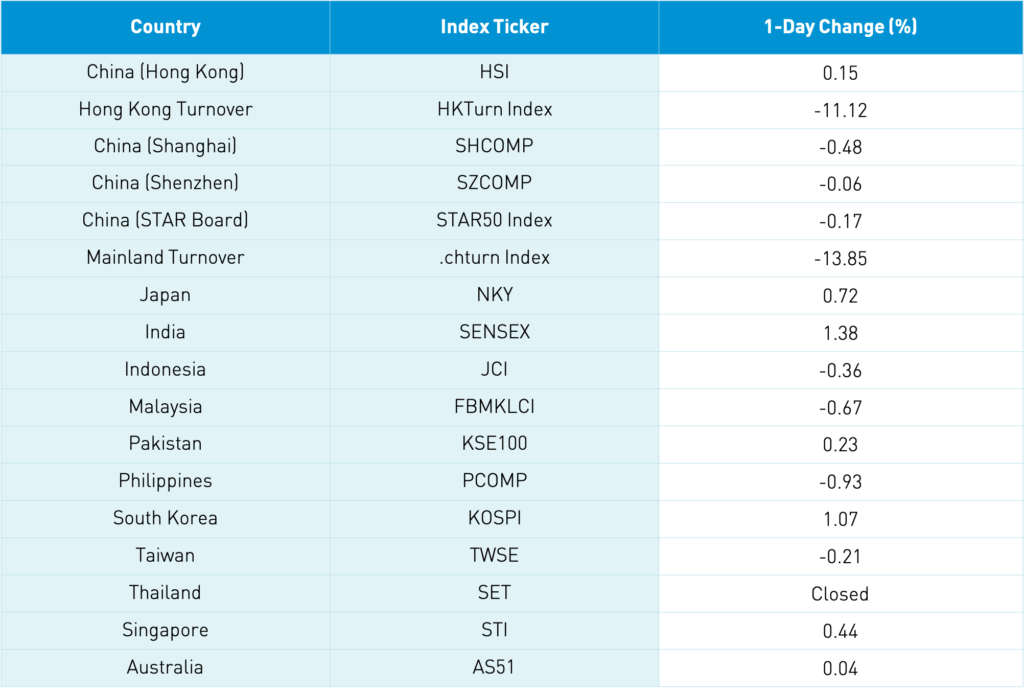

Asian equities had a mixed day as Japan, South Korea, and India outperformed while Southeast Asia was largely off. Hong Kong cheered the trade data but eased in the afternoon on the SAMR statement, which weighed on internet companies.

The STAR Board has had 44 IPOs this year, adding a total market cap of $43.272 billion. The largest company listed was battery maker Tianneng Battery Group with a market cap of $6.598B.

Trip.com (TCOM US) announced the details of its Hong Kong listing. The company will list 31.635mm shares at a price of HK $268 (~US $34.57), which is below yesterday’s close of $25.20. The listing date is next Monday, April 19th under ticker 9961 Hong Kong.

Southeast Asian food delivery, mobile payment, and ride-hailing app company Grab will go public via a SPAC. I’m a little surprised by the method of going public, though the company is a very interesting one.

It’s been reported that Janet Yellen won’t label China a currency manipulator, which mathematically makes sense as the renminbi has appreciated versus the US dollar. The determination of the label is formulaic.

H-Share Update

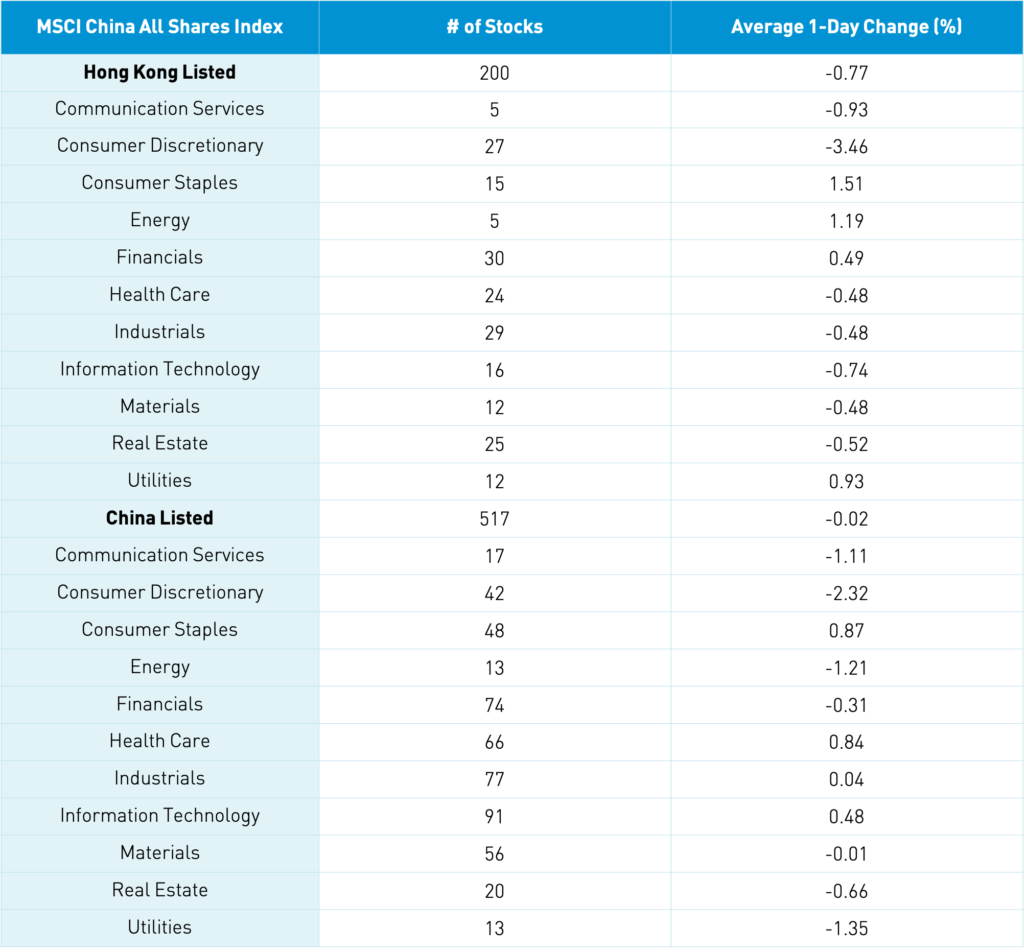

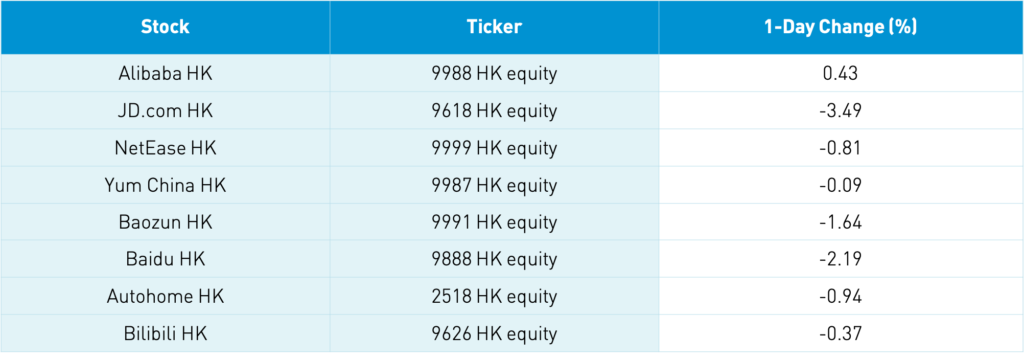

The Hang Seng managed a gain of +0.15%, though off its highs of +1.49%. Volume slumped -11% from yesterday to 90% of the 1-year average. The Chinese companies listed in Hong Kong within the MSCI China All Shares Index were off -0.76%, as staples rose +1.51%, energy +1.2%, and utilities +0.94%, while discretionary fell -3.46%, communication -0.93%, and tech -0.74%. The culprits were Hong Kong’s most heavily traded by volume Meituan, which fell -7.44% on speculation of a private placement/SAMR news, Tencent, which fell -0.9%, Alibaba Hong Kong, which gained +0.43%, JD.com Hong Kong, which was off -3.49%, Xiaomi, which fell -0.2%, AIA, which rose +3.22%, China Mobile, which was off -0.3%, China Construction Bank, which gained +1.7%, Bank of China, which was up +1.33%, and Li Ning Co, which gained +1.68%. Southbound Connect volumes were very light as Mainland investors bought $159mm of Hong Kong stocks as Southbound trading accounted for 9.4% of Hong Kong turnover.

A-Share Update

Shanghai, Shenzhen, and STAR Board eased off morning gains to close -0.48%, -0.06%, and -0.17% respectively. Volumes were off -13.85% from yesterday to just 76% of the 1-year average. Breadth saw 1,208 advancers and 2,668 decliners. The 517 Mainland stocks within the MSCI China All Shares Index gained +0.02%, led by staples +0.9%, healthcare +0.87%, and tech +0.51%, while discretionary fell -2.29%, utilities -1.32%, and energy -1.18%. Recent winners were Hainin Island plays, the Hawaii of China, while hydro and wind stocks were hit with profit-taking. Mainland’s most heavily traded were BOE Tech +1.56%, China Tourism -10%, Kweichow Moutai +0.6%, CATL +3.1%, and COSCO Shipping -4.91%. Northbound Connect volumes were moderate/light as foreign investors bought $1.294B of Mainland stocks today as Northbound Connect trading accounted for 5.7% of Mainland turnover.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.54 versus 6.55 yesterday

- CNY/EUR 7.81 versus 7.80 yesterday

- Yield on 1-Day Government Bond 1.54% versus 1.54% yesterday

- Yield on 10-Year Government Bond 3.16% versus 3.19% Yesterday

- Yield on 10-Year China Development Bank Bond 3.57% versus 3.57% Yesterday

- China’s Copper Price -0.27% overnight