No Medium-Term Lending Facility Rate Cut but Online Retail Sales Pick Up

2 Min. Read Time

Key News

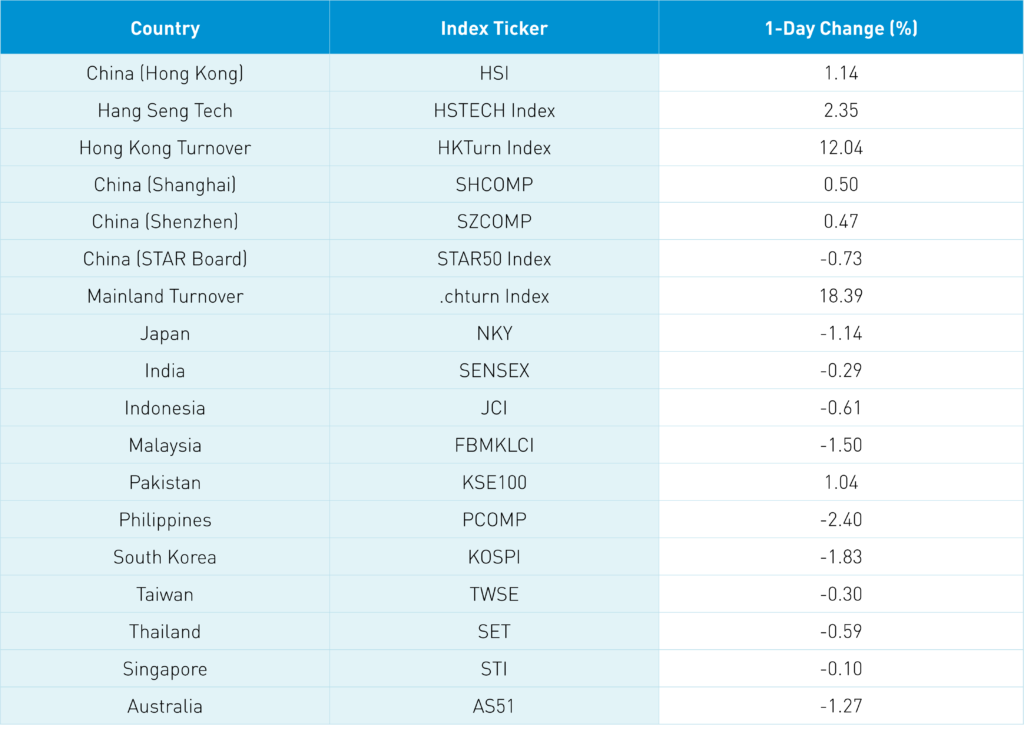

Asian equities were a sea of red excluding Hong Kong and China, which posted gains.

The PBOC kept the 1-year medium-term lending facility rate at 2.85% despite the market expecting a 10-basis point cut. We had another improvement in month-over-month data as May industrial production gained +0.7% year over year (YoY) versus April’s -2.9% and expectations of -0.9%. Coal mining jumped +8.2% YoY followed by oil & gas extraction up +6.6% respectively, while pharmaceuticals were down -12.3%. Retail sales were -6.7% YoY which was better than expectations of -7.1% and April’s -11.1% as auto sales, which accounts for 10% of retail sales, fell by -16%.

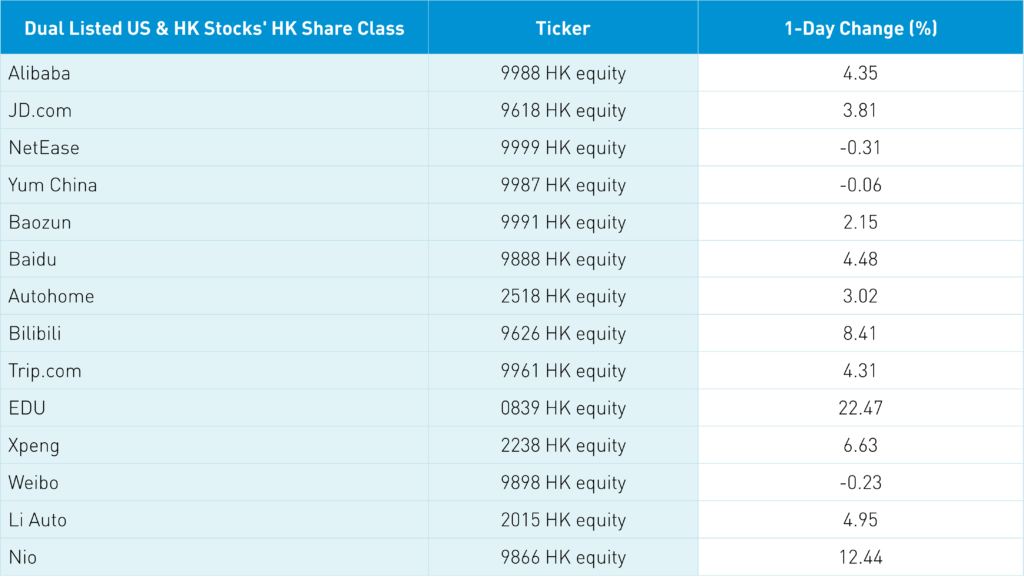

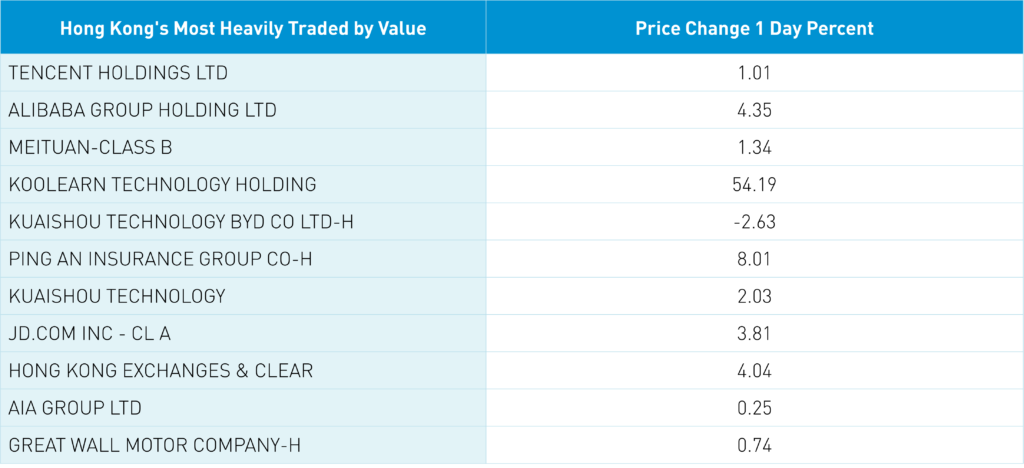

Both Hong Kong and China rallied on better than anticipated economic news and a nice uptick in volume though gains were curtailed with late-day profit-taking. Not bad considering the whole region was off which will make for an uncomfortable day for active managers underweight China. Hong Kong was led by internet stocks with Tencent gaining +1.01%, Alibaba HK +4.35%, and Meituan +1.34%.

With the retail sales release, year-to-date online retail sales of physical goods increased by 5.6% year on year which is an increase from YTD to April of +0.4%. 24.9% of the total retail sales of consumer goods took place online. The National Bureau of Statistics noted that express delivery business volume increased +20.6% month over month. Remember that the 618 e-commerce sales event is taking place with preliminary numbers looking strong thus far. Real estate was the top performer in both markets as last month’s loan prime rate cut appears to have the intended effect. I had thought another LPR cut could occur this weekend though the lack of MLF makes it unlikely; clearly my PBOC predictions are off.

Reuters reported that Baidu is selling its stake in iQIYI though the company is denying it.

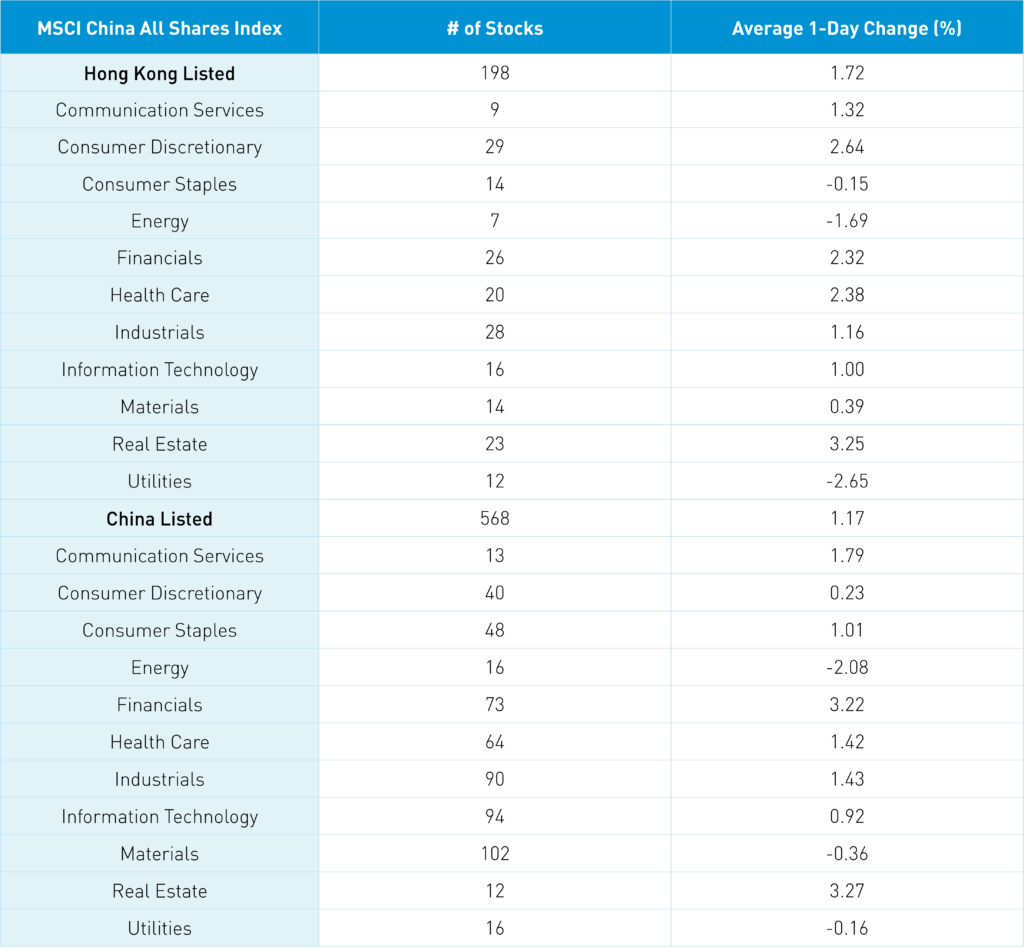

The Hang Seng and Hang Seng Tech gained +1.14% and +2.35% on volume +12.04% from yesterday which is 105% of the 1-year average. 305 stocks advanced while 175 stocks declined. Hong Kong short sale turnover increased +2.94% which is 107% of the 1-year average. Growth factors outperformed value factors while small caps outperformed large caps. Top sectors were real estate gained +3.25%, discretionary +2.64%, healthcare +2.39%, and financials up +2.32% respectively while utilities were down -2.65%, energy -1.69%, and staples -0.15%. The top sub-sectors were online education, and Alibaba ecosystem stocks while EV, lithium, and gas stocks were off. Southbound Stock Connect volumes were moderate/high as Mainland investors were net buyers of Hong Kong stocks today with Tencent, Meituan, Kuaishou, and Li Auto net buys.

Shanghai, Shenzhen, and STAR Board closed +0.5%, +0.47%, and -0.73% on volume +18.39% from yesterday which is 121% of the 1-year average. 2,664 stocks advanced while 1,718 stocks declined. Value and dividend factors outperformed growth while mega and small caps outperformed large and mid-caps. Top sectors were real estate +3.35%, financials +3.29%, communication +1.86%, and industrials +1.5% while energy fell -2.01%, materials -0.29% and utilities -0.09%. Software, insurance, and cement were the top sub-sectors while energy exploration, coal mining, and lithium were off. Foreign investors bought a healthy $1.991B of Mainland stocks via Northbound Stock Connect though Kweichow Moutai, Ping An, and CATL saw a small net outflow.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.71 versus 6.74 yesterday

- CNY/EUR 7.03 versus 7.04 yesterday

- Yield on 10-Year Government Bond 2.78% versus 2.77% yesterday

- Yield on 10-Year China Development Bank Bond 2.99% versus 2.98% yesterday

- Copper Price -0.53% overnight