Hong Kong Growth Stock Breakout (As I Knock On Wood), Week in Review

6 Min. Read Time

Week in Review

- Asian equities had a strong week, while Mainland China underperformed.

- Oracle’s Open AI announcement and the stock’s very strong performance positively affected Mainland China’s tech sector, STAR Board, growth stocks, AI, cloud supply chain, and related ecosystem stocks.

- NBC News reported that U.S. lawmakers will visit China this month, marking the first visit by a U.S. House of Representatives delegation since 2019, according to Reuters.

- The State Administration for Market Regulation (SAMR) addressed the escalating “race to the bottom” in food delivery subsidies, urging companies to “resist vicious subsidies” and “end unfair competition.”

Key News

Asian equities had a strong week higher, except for Mainland China, which was off slightly as the market consolidates after its recent strong sprint higher.

After enduring a bear market from 2021 through 2023, ending with the capitulation bottom in January 2024, Chinese equity investors finally saw a strong week, highlighted by Hong Kong breaking above recent resistance. The rally in Chinese stocks has been ongoing but largely overlooked by global investors. U.S.-listed China ETFs have seen a "whopping" $232 million of net inflow year-to-date (YTD), which tells you everything you need to know about investor positioning and participation in the rally.

Hong Kong growth stocks led gains, with Alibaba Group Holding Limited (Alibaba) rising +5.44% and Baidu Inc. (Baidu) climbing +8.08% after Western media reported both companies are developing proprietary semiconductor chips, potentially at Nvidia's expense. While this news circulated in China, today’s coverage of Alibaba in Mainland media focused primarily on the release of Qwen3-Next and Qwen3-Next-80B-A3B, which offer significant improvements in speed and power at a lower cost.

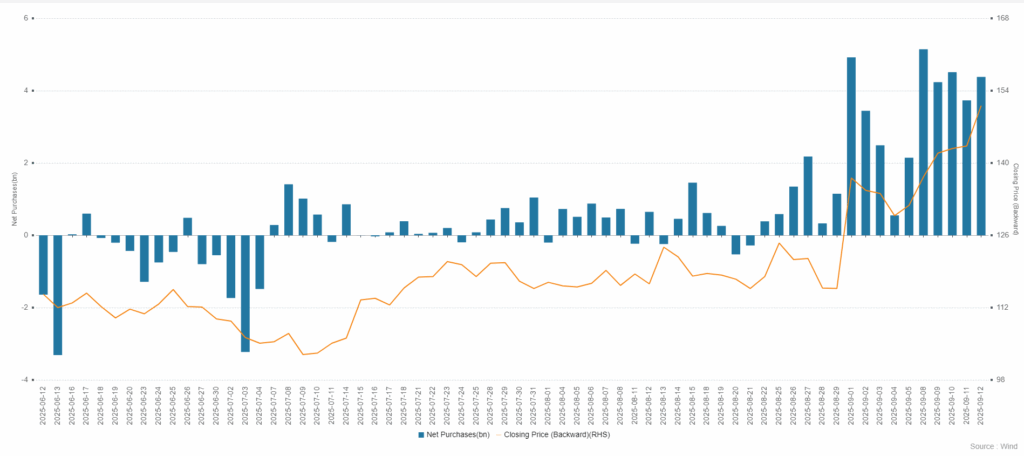

Mainland investors continued to purchase Alibaba shares in Hong Kong via Southbound Stock Connect. Baidu’s rally appears driven in part by short covering. Alongside internet stocks like Tencent (+2.22%), insurance and non-ferrous metal sectors, including metals, mining, and precious metals, also had a strong day.

Mainland China stocks closed lower, led down by banks, insurance, and household appliance sectors. Technology hardware was mostly weaker, except for Foxconn Technology Group (Foxconn), which gained +4.84%. Semiconductor stocks were mixed; Cambricon Technologies posted a gain of +7.28% while Semiconductor Manufacturing International Corporation (SMIC) fell -1.69%.

Chinese healthcare stocks rebounded in response to concerns about possible United States government tariffs on imported healthcare drugs and equipment, and the promotion of generic drug production in the US. The healthcare sector has outperformed YTD, prompting some profit-taking, although the United States policy aims to address COVID-19 shortages as ports closed. Recent positive developments in Chinese biotech overshadow these concerns.

Zijin Mining Group Company Limited (Zijin Gold), a Mainland-listed and non-ferrous metals all-star, declined -0.23% ahead of its planned relisting in Hong Kong. The Chinese government announced the "Special Action Plan for the Large-scale Construction of New Energy Storage (2025-2027)" and the "Program for Stabilizing Growth in the Power Equipment Industry (2025-2026)." Contemporary Amperex Technology Co., Limited (CATL) rose +0.76% on electrical equipment prospects, though Sungrow Power Supply dropped -2.49% and Inovance Technology fell -1.26%. Ant Group, the Alipay mobile payment company one-third owned by Alibaba, announced an upgrade to its Ant Wealth platform. Whether this signals an initial public offering (IPO) remains uncertain.

While headlines have focused on United States saber-rattling over proposed tariffs targeting both India and China for the countries’ purchases of Russian oil, it is worth noting that United States Treasury Secretary Scott Bessent is scheduled to meet Vice Premier He Lifeng next week in Madrid to discuss trade, economic, and national security issues. This pick-up in United States–China diplomatic activity is a positive sign.

Meanwhile, the Ministry of Finance’s Lan Fuan reviewed the "fiscal reform and development" during the 14th Five-Year Plan, clarifying that the government budget deficit increased to 4% this year, up from 2.7% as special government bond issuance climbed to RMB 1.94 trillion and tax cuts and refunds "will exceed CNY 10 trillion." Although real estate was not mentioned, the support for local governments to convert existing commercial housing to affordable housing and sufficient fiscal policy space suggest continued economic policy support as planning begins for the 15th Five-Year Plan.

If yesterday’s update was missed, readers are encouraged to watch the interview with Louis Gave of GaveKal Research. Excluding the introduction, Louis shared valuable insights into Chinese stocks and new government policies, supported by comprehensive charts and data. His perspectives remain rare in American investment circles, especially given the sixteen-year US equity bull market that has left non-US equities out of sight, out of mind.

Alibaba HK Stock Price and Net Inflow From Mainland Investors via Southbound Stock Connect

Last Night's Performance

| Country / Index | Ticker | 1-Day Change |

|---|---|---|

| China (Hong Kong) | HSI Index | 1.2% |

| Hang Seng Tech | HSTECH Index | 1.7% |

| Hong Kong Turnover | HKTurn Index | -1.4% |

| Hong Kong Short Sale Turnover | HKSST Index | 0.6% |

| Short Turnover as a % of Hong Kong Turnover | N/A | 13.8% |

| Southbound Stock Connect Net Buy/Sell (US $ Millions) | N/A | 936.24 |

| China (Shanghai) | SHCOMP Index | -0.1% |

| China (Shenzhen) | SZCOMP Index | -0.2% |

| China (STAR Board) | Star50 Index | 0.9% |

| Mainland Turnover | .chturn Index | 3.4% |

| Northbound Stock Connect Net Buy/Sell (US $ Millions) | N/A | Not Available |

| Jing Daily China Global Luxury Index | CHINALUX Index | 0.5% |

| Japan | NKY Index | 0.9% |

| India | SENSEX Index | 0.4% |

| Indonesia | JCI Index | 1.4% |

| Malaysia | FBMKLCI Index | 1.1% |

| Pakistan | KSE100 Index | -1% |

| Philippines | PCOMP Index | -0.3% |

| South Korea | KOSPI Index | 1.5% |

| Taiwan | TWSE Index | 1% |

| Thailand | SET Index | 0.4% |

| Singapore | STI Index | -0.3% |

| Australia | AS51 Index | 0.7% |

| Vietnam | VNINDEX Index | 0.6% |

| Indicator | Hong Kong | Mainland |

|---|---|---|

| Today's Volume % of 1-Year Average | 147% | 157% |

| Advancing Stocks | 284 | 1942 |

| Declining Stocks | 189 | 3033 |

| Outperforming Factors | Liquidity, Quality, Momentum | |

| Underperforming Factors | Low Volatility | Dividend Yield, Low Volatility, Large Caps |

| Top Sectors | Materials, Discretionary, Communication | Real Estate, Materials, Tech |

| Bottom Sectors | Energy, Staples | Communication, Financials, Discretionary |

| Top Subsectors | Steel, Consumer Discretionary Distribution, Non Ferrous Metal | Computer Hardware, Base Metals, Semis |

| Bottom Subsectors | Coal, Textiles, Household Appliances | Communication Equipment, Insurance, Soft Drink |

| Southbound Connect Buys | Alibaba (Very Large), Tencent (Large), Pop Mart (Moderate), SMIC, Transthera (Small), Xiaomi (Tiny) | |

| Southbound Connect Sells | Meituan (Large) |

| MSCI China All Shares Index | # of Stocks | Average 1-Day Change (%) |

|---|---|---|

| Hong Kong Listed | 152 | 1.86 |

| Communication Services | 9 | 2.62 |

| Consumer Discretionary | 28 | 2.71 |

| Consumer Staples | 13 | -0.32 |

| Energy | 6 | -0.7 |

| Financials | 24 | 0.18 |

| Health Care | 12 | 2.35 |

| Industrials | 21 | 0.07 |

| Information Technology | 10 | 1.25 |

| Materials | 10 | 3.48 |

| Real Estate | 7 | 1.88 |

| Utilities | 12 | 0.19 |

| Mainland China Listed | 395 | -0.4 |

| Communication Services | 7 | -1.97 |

| Consumer Discretionary | 29 | -1.25 |

| Consumer Staples | 24 | -0.76 |

| Energy | 13 | 0.01 |

| Financials | 64 | -1.47 |

| Health Care | 32 | -0.48 |

| Industrials | 61 | -0.12 |

| Information Technology | 90 | 0.45 |

| Materials | 54 | 0.87 |

| Real Estate | 6 | 1.33 |

| Utilities | 15 | -0.33 |

| US & Hong Kong Dually Listed | Ticker | 1-Day Change (%) |

|---|---|---|

| Tencent HK | 700 HK Equity | 2.2 |

| Alibaba HK | 9988 HK Equity | 5.4 |

| JD.com HK | 9618 HK Equity | 1.5 |

| NetEase HK | 9999 HK Equity | 2.8 |

| Yum China HK | 9987 HK Equity | -0.8 |

| Baozun HK | 9991 HK Equity | 24.6 |

| Baidu HK | 9888 HK Equity | 8.1 |

| Autohome HK | 2518 HK Equity | 5 |

| Bilibili HK | 9626 HK Equity | 2.5 |

| Trip.com HK | 9961 HK Equity | 0.6 |

| EDU HK | 9901 HK Equity | -2.3 |

| Xpeng HK | 9868 HK Equity | 3.2 |

| Weibo HK | 9898 HK Equity | -0.4 |

| Li Auto HK | 2015 HK Equity | 1.1 |

| Nio Auto HK | 9866 HK Equity | 4.8 |

| Zhihu HK | 2390 HK Equity | 2.8 |

| KE HK | 2423 HK Equity | 1.2 |

| Tencent Music Entertainment HK | 1698 HK Equity | -1.3 |

| Meituan HK | 3690 HK Equity | 0 |

| Hong Kong's Most Heavily Traded by Value | 1-Day Change (%) |

|---|---|

| ALIBABA GROUP HOLDING LTD | 5.4 |

| TENCENT HOLDINGS LTD | 2.2 |

| MEITUAN-CLASS B | 0 |

| XIAOMI CORP-CLASS B | 0.9 |

| SEMICONDUCTOR MANUFACTURI-H | -0.9 |

| BAIDU INC-CLASS A | 8.1 |

| POP MART INTERNATIONAL GROUP | 1.2 |

| SENSETIME GROUP INC-CLASS B | 7.1 |

| BYD CO LTD-H | -0.7 |

| TRANSTHERA SCIENCES NANJIN-H | 77.1 |

| Shanghai and Shenzhen's Most Heavily Traded by Value | 1-Day Change (%) |

|---|---|

| CAMBRICON TECHNOLOGIES-A | 7.3 |

| VICTORY GIANT TECHNOLOGY -A | 0.5 |

| LUXSHARE PRECISION INDUSTR-A | -0.4 |

| EOPTOLINK TECHNOLOGY INC L-A | -5.8 |

| ZHONGJI INNOLIGHT CO LTD-A | -4.1 |

| FOXCONN INDUSTRIAL INTERNE-A | 4.8 |

| HYGON INFORMATION TECHNOLO-A | -0.4 |

| CHINA NORTHERN RARE EARTH -A | 6 |

| DAWNING INFORMATION INDUST-A | 6.4 |

| SUNGROW POWER SUPPLY CO LT-A | -2.5 |

Last Night's Exchange Rates, Prices, & Yields

- CNY per USD 7.12 versus 7.12 yesterday

- CNY per EUR 8.35 versus 8.32 yesterday

- Yield on 10-Year Government Bond 1.87% versus 1.87% yesterday

- Yield on 10-Year China Development Bank Bond 1.94% versus 1.96% yesterday

- Copper Price +0.72%

- Steel Price +0.19%