Markets Look Forward Not Back, Q1 GDP Slightly Below Estimate

5 Min. Read Time

Economic Releases

Q1 GDP Year over Year: -6.8% versus estimate -6% and Q1 2019’s 6%

Takeaway: We knew the GDP print was going to be bad and it didn’t disappoint. Despite the headlines, markets knew this and focused on the Industrial Production release. The question will be whether the global economic slowdown’s effect on China as global trade is falling. How quickly we come back online globally will drive Q2 and 2nd half of the year estimates. Policymakers cannot create external demand. It is important to note that China has a lot of dry powder as they have not cut interest rates as dramatically as the US. Support has come in the form of freeing up cash for banks to provide loans with an emphasis on small-medium enterprises and private companies. Fiscal policies have been supportive though measured.

March Industrial Production YoY: -1.1% versus estimate -6.2%

Takeaway: While not everyone is buying yet, evidently China’s industrial sector has been able to maintain relatively stable production considering the circumstances. Industrial production requires inputs such as raw materials and commodities so we should have anticipated copper’s rally on the news. There are several interesting items that jump out to me such as Pharmaceutical +10.4% and Telecommunications/Computers +9.9%. While the reason for the pharma surge is obvious, the latter may be the effect of global work from home policies. We need more laptops, servers and cloud computing to work from home. Auto Manufacturing remains in the pain cave off -22.4%. Ford noted their Q1 China revenue was off -35% according to a Reuters article.

March Retail Sales YoY: -15.8% versus estimate -10%

Takeaway: Retail sales were hit hard by restaurant/catering plummeting -46% and bigger ticket items such as auto -18% and household electronics -29.7% and jewelry -29.7%. Not surprising medicine +8%, food +19.2%, and office supplies +6.1%. I had hoped retail sales would beat estimates as China returns to work. That assumption was incorrect though I remain optimistic April data will be a significant improvement. Yes, the quarantine has been lifted but people are still nervous. We’ve seen that as mass transit activity, i.e. subways and buses, is recovering slowly while traffic is bad. Many Chinese are social distancing by driving to work instead of taking the subway. This trend should benefit internet and e-commerce companies versus physical stores. The quarantine also forced some people to utilize e-commerce companies for the first time. This is a belief that these habits will stick post-quarantine.

March Property Investment YTD YoY: -7.7% versus Feb’s -16.3%

Takeaway: The release does show an improvement month over month indicating that work is picking up. This should accelerate in the months ahead as work resumes in earnest.

March Fixed Asset Investment YoY: -16.1% versus estimate -15% and Feb’s -24.5%

Takeaway: No surprises as building factories was hampered due to the quarantine. Private companies suffered worse than state owned enterprises. Expectations are for this data to improve as delayed projects start come back online.

March Jobless Rate: 5.9% versus prior’s 6.2%

Takeaway: Like every country, employment is job 1 for China’s policy makers.

Week In Review

- On Monday, FTSE announced that it will be adding Alibaba’s Hong Kong listing to its FTSE China 50 Index, which is tracked by the largest China ETF by assets. This will likely lead to the purchasing of $510 million in Alibaba’s Hong Kong shares.

- On Tuesday, China’s trade data surprised to the upside. Exports decreased -3.5% YoY in RMB terms compared to an expected -12.8% and imports decreased by -2.4% YoY in March compared to an expected -7%.

- On Wednesday, the PBOC lowered the Medium-term lending facility, the rate that the central bank charges to key financial institutions, by 0.2%, implying that the Central Bank will cut its overall target rate, the loan prime rate, on April 20th.

- On Thursday, Tencent announced that gaming revenue increased by 40% YoY in the first quarter.

- China released its first-quarter GDP growth on Friday along with industrial output and retail sales. The releases are the most significant official sign yet of the impact that the coronavirus outbreak had on the country’s economy.

Key News

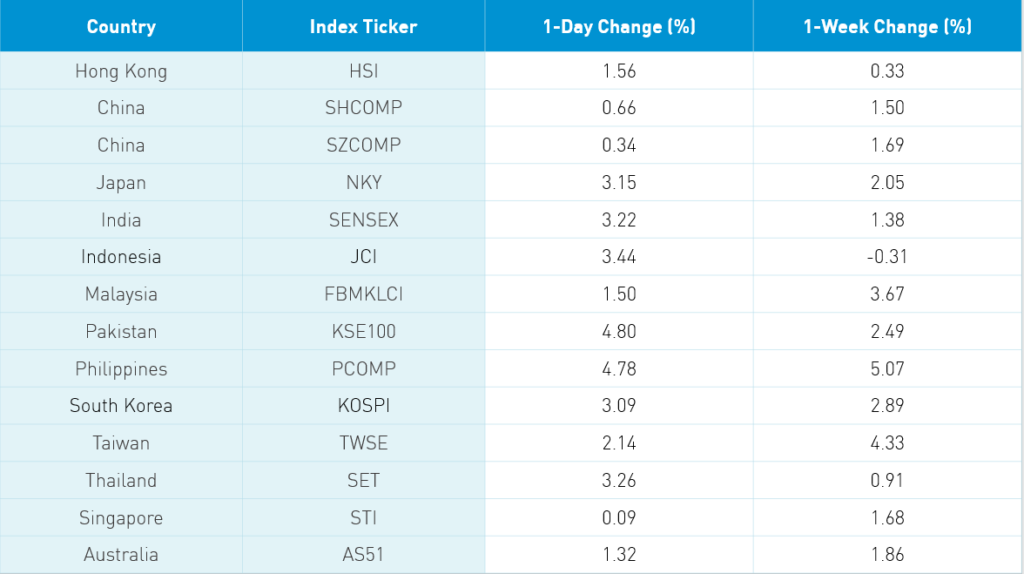

Asian equities ripped higher Friday on news that the US will re-open states incrementally and positive Gilead drug results in Chicago. For many Asian equity markets, today’s price action accounted for nearly all of their weekly gains.

Investors had anticipated the dismal 10 am GDP and economic data release though March Industrial Production came in better than expected. Hong Kong and the Mainland China markets gave up some of their intra-day gains on the mid-afternoon release of updated coronavirus victims, which increased to 39% to 4,632 deaths of which another 1,290 occurred in Wuhan, bringing its total to 3,869. One broker noted that in the early afternoon a large global hedge fund reported a large Q1 loss and a sell-side Apple downgrade were factors in markets giving up gains.

Some of the worst-performing sectors of late outperformed in Hong Kong today such as casinos and autos. The most heavily traded stocks in Hong Kong were Tencent +0.69%, Alibaba’s HK listing +2.37% and Ping An Insurance +3.22%. Foreign investors were active today and this week in buying Mainland stocks via the Northbound Stock Connect trading venue. For the week, foreign investors bought $4.25 billion worth of Mainland stocks. Tech and consumer staples had a strong day on 5G chatter, strong Apple iPod sales and alcohol stocks proving why they are considered staples. A Mainland broker noted profit-taking in health care ahead of the weekend.

H-Share Update

The Hang Seng opened +1.88% higher hit an intra-day high of +2.75% before easing in the afternoon to close +1.56%/+373 index points at 24,380. Volumes surged 30% from yesterday while breadth was strong with 46 advancers and 4 decliners. Index heavyweights led the way with AIA +4.54%/+114 index points, Ping An Insurance +3.22%/+45 index points and Tencent +0.69%/+18 index points. Real estate firm Wharf Real Estate was the best performer +6.1%/+6 index points while food maker Want Want was off -2.26%/-2 index points. Hong Kong companies outperformed Chinese companies +1.84% versus +1.47% using the HS HK 35 and HS China Enterprises as proxies. The Chinese companies listed in Hong Kong within the MSCI China All Shares gained +1.26% led higher discretionary +2.7%, industrials +1.96%, real estate +1.92%, financials +1.77%, tech +1.32%, materials +1.1%, utilities +1.07%, communication +0.71%, energy +0.34%, staples +0.3% and health care +0.26%. Southbound Connect volumes were moderate as Mainland investors were buyers of Hong Kong-listed stocks. Volume leader Ping An saw massive buying of 20 to 1, Tencent 2 to 1 though Semiconductor Manufacturing sold almost 3 to 2.

A-Share Update

Shanghai & Shenzhen followed a similar trajectory as the Hang Seng. Shanghai opened +0.31% higher, hit an intraday higher of +1.24% before easing into the close +0.66%. Shenzhen opened +0.73% higher, hit an intraday high of +1.23% before easing into the close +0.34%. Turnover on the Mainland jumped +24% from yesterday while breadth was mixed with 1,960 advancers and 1,599 decliners. Large caps outperformed mid and small caps by nearly 1%. The Mainland listed socks within the MSCI China All Shares Index gained +0.8% led higher by tech +1.75%, staples +1.33%, industrials +1.22%, discretionary +1.13%, financials +0.92%, materials +0.48%, real estate +0.47%, communication +0.38% and energy +0.37%. Utilities and healthcare were off -0.53% and -1.14%. Foreign investors were active buyers of Mainland stocks via the Northbound Connect trading platform. Volumes in Shanghai were nearly as high as the Shenzhen though the buying was more pronounced. The most heavily traded stocks were MSCI inclusion names Kweichow Moutai and Ping An Insurance, which saw buyers outpace sellers by a small amount. Foreign investors bought $1.219B of Mainland stocks today, bringing the weekly total to $4.25B.

Last Night’s Prices & Yields

- CNY/USD 7.07 versus 7.08 yesterday

- CNY/EUR 7.70 versus 7.67 yesterday

- Yield on 1-Day Government Bond 0.46% versus 0.46% yesterday

- Yield on 10-Year Government Bond 2.56% versus 2.53%

- Yield on 10-Year China Development Bank Bond 2.84% versus 2.81% yesterday

- Commodities on the Shanghai & Dalian Exchanges were higher with Dr. Copper +1.71%