Curb Your Pessimism, Week In Review

4 Min. Read Time

Next week we will be hosting three webinars, please join us.

- The World's Second Largest Bond Market Is Now Open: A Discussion With KraneShares Europe and Sanjay Rao of Bloomberg

June 16th at 2 pm GMT - One Year Review: A Conversation with Nancy Davis of Quadratic Capital and Jonathan Krane, CEO of Krane Funds Advisors

June 16th at 11 am EST - A Larger Piece of the Pie: A Discussion With MSCI on Choosing the Right Mainland China Exposure,

June 18th at 10 am EST

Week In Review

- China released May trade data showing a slight increase of 1.4% in exports on Monday, defying expectations for an export slump. Powering the strong export number were exports of health care supplies to the rest of the world.

- Mainland health care rebounded on Tuesday on the news that a vaccine entered a clinical trial with human testing as Asian equities followed Wall Street higher.

- Asian equities mostly rose again on Wednesday though Shanghai and Shenzhen diverged.

- NetEase listed in Hong Kong for the first time on Thursday. Shares in the company's IPO rose +5.6%.

Friday's Key News

Asian equities posted modest losses as Australia and South Korea took an outsized hit. Broker chatter was fairly muted about the US crash yesterday. The fall was dismissed as an overdue correction following a robust rebound from March lows. Hong Kong gapped lower at the open -2.29% but managed to claw back most of the initial losses to close -0.73%. Volume leaders were Tencent -0.32%, Alibaba HK -0.47%, Meituan Dianping +0.36%, and NetEase HK -1.1%.

It is worth pointing out that NetEase US shares were off -3.1% and Alibaba US shares were off -3.7% Thursday as Hong Kong investors rightfully ask why these stocks would be down on US-centric news. One broker noted there were rumors of a Meituan Dianping and Didi merger though I’ve not seen anyone else mention it. Wouldn’t that be something! Meituan had a broker upgrade today, which likely drove the positive price action.

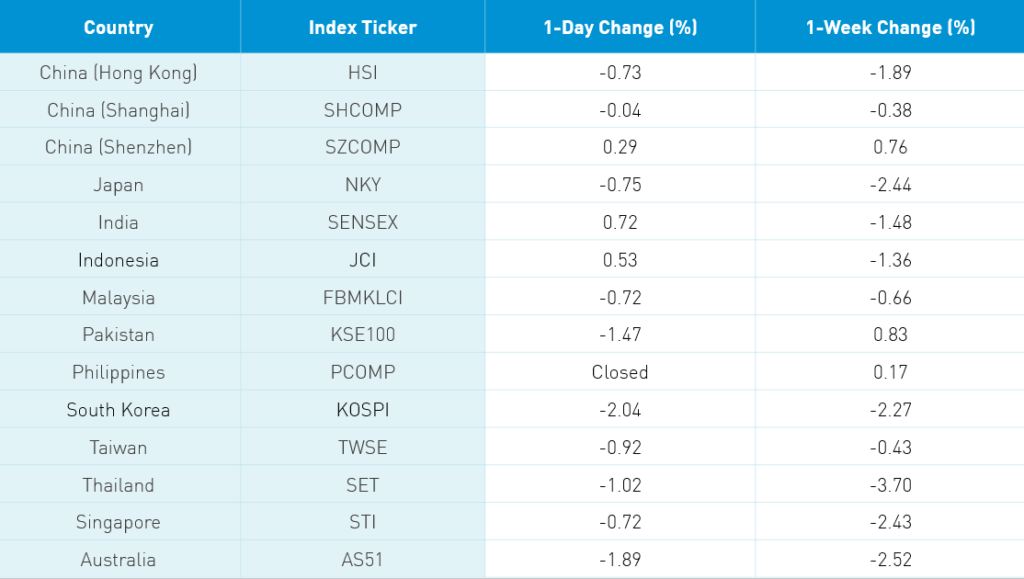

It is worth looking at the weekly returns of Asian equity indices below. Mainland China sticks out doesn’t it? The Mainland market is still a small part of globalized fund flows, which means a very low correlation to other equity indices. Low equity correlation is exceedingly hard to find. It is also worth pointing out that Hong Kong stocks, which have historically been foreign investors’ definition of China, fared much worse than the Mainland. Apparently, investors in China have a different view of the economy than foreign investors. Reuters covered a press conference from Zhu Guangya, “a cabinet advisor and former vice finance minister,” who called on US-China trade communication while Liu Huan, “another cabinet advisor, said he expected China’s economy to rebound sharply in the third quarter.” The current budget deficit is at 3.6% but could be “raised…if economic pressures increase.” There was chatter overnight China’s loan rate could be dropped next week.

Macau casinos had a strong day while energy stocks got hammered in Hong Kong while healthcare had another strong day. Mainland stocks also gapped lower at the open but traded higher into the close with the Shenzhen posting a modest gain.

Bitauto Holdings (BITA US) announced it will go private for $16 a share. Tencent and firm called Hammer Capital are making a smart move as China auto sales appear to have bottomed out. I suppose one less US listed Chinese company for US politicians to worry about.

H-Share Update

The Hang Seng opened lower -2.29% but managed to claw back most of the losses to close -0.73%/-178 index points at 24,301. Volumes were light, down -18.9% from yesterday while breadth was off with 14 advancers and 36 decliners. Index heavyweights HSBC -1.45%/-33 index points, China Construction Bank -1.27%/-25 index points and today’s worst performer energy giant CNOOC -4.64%/-22 index points. Wharf Real Estate was the best performer rising +2.68%/+2 index points. China-domiciled companies were off -1.13% versus -0.06% for Hong Kong-domiciled companies using the HS China Enterprise and HS HK 35 indexes as proxies. The Chinese companies listed in Hong Kong within the MSCI China All Shares Index were off -0.54% with healthcare +1.25%, discretionary +0.0%, tech -0.15%, real estate -0.35%, materials -0.38%, staples -0.39%, communication -0.43%, utilities -0.68%, industrials -0.78%, financials –1.03%, and energy -3.52%.

Southbound Connect volumes were moderate as Mainland investors bought the dip. Volume leaders Tencent, Semiconductor Manufacturing and Meituan Dianping all saw buyers outpace sellers with Tencent’s 2 to 1 leading the way. Mainland investors bought $229mm worth of Hong Kong stocks today as Southbound Connect trading accounted for 7.4% of Hong Kong turnover.

A-Share Update

Shanghai & Shenzhen opened lower -1.51% and -1.99% but clawed back to close -0.04% and +0.29% at 2,919 and 1,870. Volumes were off -2.5% though remained above the 1-year average while breadth was off with 1,562 advancers and 2,041 decliners. Large, mid, and small caps were largely in line with one another. The Mainland stocks within the MSCI China All Shares Index rose +0.05% with communication +1.76%, healthcare +1.09%, discretionary +1.03%, staples +0.79%, financials -0.2%, real estate -0.27%, energy -0.39%, industrials -0.58%, tech -0.6%, and materials -0.95%.

Northbound Connect volumes were moderate though Shanghai saw a pickup in volumes in mixed trading. Foreign investors sold a few positions in size leading to the net sale of Mainland stocks. The selling was concentrated in ICBC stock, which accounted 2/3of total selling. Anhui Conch Cement and Contemporary Amperex Tech saw half the selling of ICBC. If we eliminated those three major sales, there would have been foreign inflow today. Foreign investors sold $126mm worth of Mainland stocks today as Northbound Connect trading accounted for an above average 6.3% of Mainland turnover. For the week, foreign investors were net buyers.

Last Night’s Exchange Rates & Prices

- CNY/USD 7.08 versus 7.07 yesterday

- CNY/EUR 7.99 versus 8.04 yesterday

- Yield on 1-Day Government Bond 1.20% versus 1.25% yesterday

- Yield on 10-Year Government Bond 2.75% versus 2.77% yesterday

- Yield on 10-Year China Development Bank Bond 3.09% versus 3.09% yesterday