Mainland and Foreign Investors Buy The Dip in Chinese Equities

6 Min. Read Time

Key News

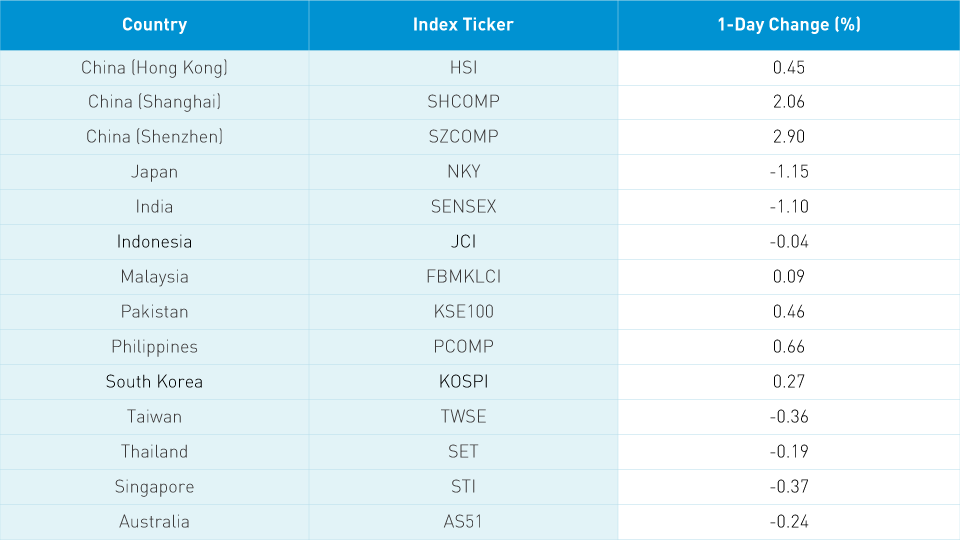

Asian equities were mixed as uncertainty surrounding US stimulus, Fed Chair Powell’s coming conference, and US tech CEOs meeting with Congress all weighed on sentiment. Japan was lower in advance of a significant index rebalance scheduled for tonight. Mainland Chinese markets showed their lack of correlation to US stocks last night by rising strongly.

We have mentioned that technical analysts believe the Mainland has broken out of a five-year base. Post-breakout we saw a nice pullback thanks to US-China political tension. We can’t predict the future, but today’s move showed Mainland investors bought the pullback and sent the market higher. Investors in China were joined by foreign investors who bought $1.105 billion worth of Mainland stocks via Northbound Stock Connect after net selling over the previous four trading days and 10 of the last 13 trading days. Only time will tell how this plays out but I’m optimistic! There were amazingly 3,207 advancing stocks and only 370 decliners on the Mainland. Chinese investors sold bonds hard as the Chinese 10 Year Chinese Gov’t Bond yield rose six basis points from 2.88% to 2.94%. It doesn’t sound like much, but that is a monster move as my colleague and former fixed income guru Fernando would tell you after he picks himself off the floor after having fallen out of his chair.

Kweichow Moutai (600519 CH) fell -2.22% but rallied to close +0.12% following a positive earnings release. The DND trade (drugs/pharma and drinks/alcohol) was strong along with brokers, an indication that investors realize a renewed bull market is good business for brokers. Vaccine hopes continue to lead healthcare higher as Wuxi Biologics (2269 HK) rose +4% after reporting net profit rose +58% year over year in the second quarter. Tech had a strong day both on the Mainland and in Hong Kong due to Apple’s strong China sales for Q2 and anticipation of further product roll outs in the second half of the year. Hong Kong posted modest gains as volume leaders were mixed with Tencent -0.37%, Semiconductor Manufacturing +8.75%, Meituan Dianping +1.05%, and Alibaba HK -0.65%. JD.com HK was off -1.48% while NetEase was down by -0.56%.

After the close, Hong Kong reported that the city-state’s GDP fell -9% year over year in the second quarter. The number was painful but expected. There have been reports have coronavirus flare ups in Mainland China, Vietnam, which had very few cases to begin with, and Hong Kong. Unfortunately, the virus hasn’t gone away just yet. Meanwhile, China is having a very wet summer. The rain may have a minor effect on economic activity during the season.

Our friend Maureen asked a question concerning AIA on our webinar yesterday. AIA is domiciled in Hong Kong rather than China so it is included in the MSCI Hong Kong Index and not in the MSCI China Index. MSCI Hong Kong is a developed market index rather than EM. What if MSCI Hong Kong was merged into MSCI China? MSCI Hong Kong has 40 stocks and a market cap of $448 billion compared to MSCI China’s 711 stocks and market cap of $2.370 trillion. If Hong Kong were merged into China, China’s weight within MSCI EM would increase by 18.9%. Today, China is 40.95% of Emerging Markets. Adding Hong Kong to China would raise China’s weight on EM to about 60%. There is also MSCI’s inclusion of Shanghai and Shenzhen stocks in the MSCI China A Index to consider. Currently, only 20% of the MSCI China A stocks’ free float market cap are included in EM at a 5% weight. At full inclusion, they would represent 20% of EM on their own. So……..China today 40%.........full China A inclusion gets China to 60%.........If Hong Kong goes into China and therefore EM, that would push China to around 80% of Emerging Markets. You heard it here first! This is likely to happen, just not anytime soon.

The new Hang Seng Tech Index has garnered some attention. My thoughts? 1) It is not a tech index. It is a growth index. The definition of technology changed in September 2018 when the Global Industry Classification made real estate its own sector and many technology companies were reclassified from technology to consumer discretionary and communication. For instance, Amazon and Alibaba went from being classified as tech to being classified as discretionary. Likewise, Facebook and Tencent went from tech to communication services. Is the name a big deal? No, but it does rub me the wrong way. 2) The index is comprised of only Hong Kong-listed stocks. I do not believe that the Hong Kong IPO parade will end in the short term. However, Chinese companies are still listing in the US. Dada Nexus is due to list there in early June. What if, following the US election, US-China relations improve? Companies want to garner the highest IPO price, which means US Exchanges will still have an advantage. US companies relisting in Hong Kong are issuing smaller floats so we haven’t seen a monster Hong Kong IPO yet. 3) The Hang Seng Index is likely to add BABA HK, Meituan Dianping, and Xiaomi in the September rebalance. The Hang Seng Index is widely subscribed to by both ETFs and futures. Adding these growth names will make it slightly less dominated by financials. Takeaway: The index is apt to be used regionally, but I believe it will have a hard time competing with its larger sibling the Hang Seng.

There is an interesting Hong Kong IPO coming: Tigermed (oversubscribed 50X) and JD Health along with several US listings. These are on my radar and there will be more details to come.

The Financial Times had an article today titled “This surge in Chinese stocks is not like the last one” by Enodo Economics’ chief economist Diana Choyleva. The article speaks to the low margin level compared to the 2014/2015 run up. An interesting point is the effort to diversify Chinese household wealth between the stock market and the housing market. Ms. Choyleva believes housing is causing wealth inequality in China. If you knew Denver was going to grow like it did, wouldn’t you buy land or build houses in anticipation of its growth? In China, many investors poured money into “ghost cities” in anticipation of their growth. The “ghost cities” are, in many cases, now filled with residents making those speculators rich. We have pointed out previously that only 4% of Chinese household wealth is invested in stocks and mutual funds. We are experiencing a slight shift in Chinese household wealth to stocks though even a small shift will have a big effect on markets.

H-Share Update

The Hang Seng swung between losses and gains twice intra-day to close +0.45%/+110 index points at 24,883. Volume was off -7%, making it barely above the 1-year average while 34 stocks advanced and 14 declined. Index heavyweights led the way with top performer HSBC +2.73%/+60 index points, HK Exchanges +1.16%/+15 index points, and Tencent -0.37%/-11 index points. Today’s worst performer was Sino Biopharma, which fell -1.48%/-3 index points. Hong Kong-domiciled companies outperformed China-domiciled stocks +0.78% versus +0.32% using the HS HK 35 and China Enterprise indexes as proxies. The 204 Chinese companies listed in Hong Kong and within the MSCI China All Shares Index +0.46% with tech +2.68%, materials +2.19%, healthcare +1.25%, real estate +0.98%, discretionary +0.89%, financials +0.63%, industrials +0.28%, communication -0.21%, staples -0.35%, energy -0.65%, and utilities -0.76%.

Southbound Stock Connect volumes are back to normal levels though Mainland investors continue to buy Hong Kong stocks. Shanghai Connect volume leaders were Semiconductor Manufacturing, which was bought 7 to 5, Tencent, which was bought 2 to 1, and Meituan Dianping, which was bought nearly 2 to 1. Mainland investors bought $472mm worth of Hong Kong stocks today as Southbound Connect accounted for 10% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen moved from the lower left to the upper right to close +2.06% and +2.9% at 3,294 and 2,236, respectively. Volume increased +15% from yesterday to 1.5 times the 1-year average while breadth was very strong with 3,207 advancers and only 370 decliners. Mid and small caps outperformed large in a broad rally. The 509 Mainland stocks within the MSCI China All Shares Index gained +2.44% with tech +3.98%, health care +3.62%, discretionary +3.33%, communication +3.14%, financials +2.57%, industrials +2.16%, materials +1.6%, real estate +1.44%, energy +1.06%, staples +0.9%, and utilities +0..48%.

Northbound Stock Connect volumes were strong especially on the Shenzhen as foreign investors were net buyers of Mainland stocks after four days of net outflows and net selling for 10 of the last 13 trading sessions. Shanghai Connect volume leaders were Kweichow Moutai, which was sold nearly 2 to 1, China Tourism, which was sold 8 to 7, and Longi Green Energy Technology, which was sold 3 to 1. Shenzhen Connect volume leaders were Gree Electric Appliances, which was bought 2 to 1, Wuliangye Yibin, which was sold 2 to 1, and East Money Information, which was net bought by a small margin. Foreign investors bought $1.105 billion worth of Mainland stocks as Southbound Connect trading accounted for 7% of Mainland turnover.

Last Night’s Exchange Rates & Yields

- CNY/USD 7.00 versus 7.00 yesterday

- CNY/EUR 8.23 versus 8.20 yesterday

- Yield on 1-Day Government Bond 1.02% versus 1.32% yesterday

- Yield on 10-Year Government Bond 2.94% versus 2.88% yesterday

- Yield on 10-Year China Development Bank Bond 3.43% versus 3.39% yesterday