Got Growth? Apple Earnings Lift Its Supply Chain, Official PMIs Show Expansion, Week In Review

6 Min. Read Time

Week In Review

- Asian equities had a mixed start to the week on Monday as US-China political rhetoric continues to hang on sentiment while spikes in coronavirus cases gave investors additional pause.

- On Tuesday, Chinese search engine Sogou Inc. (SOGO US) jumped +48% to $8.51 after Tencent offered to buy the remainder of the company for $9 a share.

- Investors in China were joined by foreign investors who bought $1.105 billion worth of Mainland stocks via Northbound Stock Connect on Wednesday after net selling over the previous four trading days and 10 of the last 13 trading days.

- TAL Education reported mixed Q2 results on Thursday. While revenue grew by 35.2% YoY, costs grew by 40.3%. The company continues to gobble up market share, but that growth has come with some margin pressure.

Key News

Asian equities ended the day largely down as Japan, Singapore and Australia were all off due to concerns over coronavirus flare ups. However, hidden in the doom and gloom was the growth rally set off by Apple’s impressive quarterly results as the company’s suppliers across Asia ended the session higher. For instance, while South Korea’s well-followed Kospi index was down -0.78%, the growth-geared Kosdaq was up +0.14%. That being said, investors in Mainland China clearly didn’t get the memo as Shanghai and Shenzhen were up by +0.71% and +1.33%, respectively. Mainland-listed Apple supplier Luxhsare (002475 CH) rose +3.52%, while Air pod maker GoerTek gained +9.8%. China’s DND trade, not Dunkin Donuts, but drugs (pharma stocks) and drinks (alcohol stocks), was up despite Kweichow Moutai falling -0.11%. Meanwhile, health care stocks had another strong day.

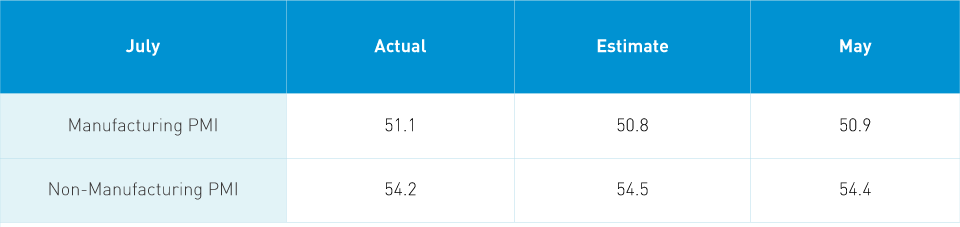

The reported data is the “official” Purchasing Managers Index from the National Bureau of Statistics. The “official” PMI is a survey of large companies with large number of companies participating. The Caixin PMI, on the other hand, surveys medium and smaller companies though its survey is filled out by a far smaller number companies which makes it a little more volatile. PMIs are diffusion indexes meaning they measure activity on a month over month basis. A reading of above 50 means activity is growing while a reading below 50 means activity is contracting.

Regardless, it is 2020 and we don’t need to rely on government data considering the plethora of alternative indicators collected through smartphone data among other sources. The same is true in China.

The “official” Manufacturing PMI posted its fifth month of growth led by strong activity in both output and new orders. The data does show, however, that China is far from immune to the economic consequences of global quarantines as export orders contracted while employment was off slightly for the third month in a row. On the positive side, business activity expectations came in very strong.

The Non-Manufacturing PMI was strong as well, which is important considering the fact that the service sector now comprises more than 50% of China’s GDP. Employment was soft, which is likely due to weakness in offline retailers and restaurants. With no cure and no vaccine, an element of the population remains cautious and is reluctant to go out and spend. The Ministry of Commerce reported today that online retail sales YTD grew +7.3% to $730 billion while June retail sales grew by +7.3% year over year.

A Mainland news source noted that Fosun Pharma (600196 CH and 2196 HK) began Phase 1 trials for a coronavirus vaccine with 36 volunteers. The vaccine is being developed in partnership with Germany’s BioNTech and Pfizer. It is entirely too bad that politicians can’t get along as well as scientists.

Hong Kong stocks posted modest losses with volume leaders Tencent -0.19%, Semiconductor Manufacturing (SMIC) +5.85%, Alibaba HK +0.49%, Meituan Dianping -1.59%, and AIA -1.13%. Apple’s Hong Kong-listed suppliers AAC and Sunny Optical gained +3.61% and +0.97%, respectively. JD.com HK was flat while NetEase HK gained +0.72%. Foreign investors sold -$272mm worth of Mainland Chinese stocks today bringing their weekly total selling to $606mm. Year to date, foreign investors have bought $18B worth of Mainland stocks.

Pew Research disseminated a study showing the decline in Americans’ opinion of China. Politicians and the media piling on the negativity with very little fact checking is having an impact. My biggest concern is that we all end up learning a very hard lesson from ECON 101. US companies generated $376B of revenue in China that never shows up in trade data since the goods are manufactured and sold in China and across Asia. Look at Apple’s earnings, for instance. Apple alone generated $9.3B in revenue in China this quarter. That number won’t go into any trade data since the iPhones were manufactured and sold in China. US companies geared to the consumer such as Nike, Walmart, and General Motors continue to prosper in China’s market.

One small story thinking about my first China trip back in 2013. Jon and I had lunch at a very modern restaurant in Beijing with two old colleagues from his days living and running a business in Shanghai. Jon and one friend went to field calls leaving me with his other buddy who spoke as much English as I did Chinese, i.e. nada. My dining partner started eating these puff balls so doing my best Marco Polo I figured: why not? When in Rome, do as the Romans do. So I grabbed one and popped it in the pie hole. However, I realized immediately that this thing was extremely chewy. As my dining partner ate more puff balls I felt obligated to go toe to toe with him by matching his enthusiasm for the puff balls. My dining partner was giving me a strange look as I chomped away trying to get the puff balls down without a waiter having to give me the Heimlich maneuver. Finally, Jon and his friend came back to the table and my dining partner immediately spoke to them in Chinese while pointing at me. Having chocked down several puff balls, I asked: what did he say? Jon’s returning friend said “Mr XYZ recommends taking the shell off the chestnut before eating them.” Chewiness mystery solved….and good advice.

H-Share Update

The Hang Seng traded in a tight range and eased as the session progressed to close-0.47%/-115 index points at 24,595. Volume was off -7% from yesterday though remained above the 1-year average. Breadth was off with 21 advancers and 25 decliners led by HSBC -1.96%/-42 index points, China Construction Bank -1.56%/-29 index points, and HK Exchanges +2.1%/+28 index points. Apple supplier AAC was the day’s best performer while energy giant CNOOC -2.84% was the worst. Hong Kong-domiciled companies outperformed China-domiciled companies +0.18% versus -0.57% using the HS HK 35 and China Enterprise indexes as proxies. The 205 Chinese companies listed in Hong Kong within the MSCI China All Shares Index fell -0.3% with tech +1.49%, real estate +0.7%, materials +0.2%, utilities +0.12%, health care -0.04%, industrials -0.12%, communication -0.16%, staples -0.79%, financials -0.89%, discretionary -0.97%, and energy -1.79%.

Southbound Stock Connect, the trading venue that allows Mainland investors to buy Hong Kong-listed stocks, saw modest volumes that were well off the elevated levels of the last month. The Hong Kong exchange (HKEX) disseminates buying and selling volume for individual stocks. So, we know that if buying volume exceeds selling volume investors were net buyers or vice versa. Unfortunately, the HKEX doesn’t give the data as buying minus selling requiring people like me to do the math for you. I am your humble Stock Connect math servant. Mainland investors were net buyers of Hong King stocks today as they usually are. Shanghai Southbound Connect volume leader SMIC had buyers outpace sellers by a small margin, Tencent had buyers outpace sellers by 2 to 1 and Meituan Dianping had buyers outpace sellers by 3 to 2. Mainland investors bought $360mm worth of Hong Kong stocks today as Southbound Connect trading accounted for nearly 10% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen had a roller coaster day as a surge in the morning session collapsed before the noon lunch break and was followed by an afternoon rally that led the indexes to close +0.71% and +1.33% at 3,310 and 2,256, respectively. Volume increased 4% to 1.75X the 1-year average. Breadth was mixed with 2,080 advancers and 1,475 decliners as mid and small caps outpaced large caps. The 510 Mainland-listed Chinese stocks in the MSCI China All Shares Index gained +1.36% with tech +2.55%, discretionary +2.25%, health care +1.79%, materials +1.46%, industrials +1.12%, communication +1.05%, financials +0.98%, real estate +0.72%, staples +0.67%, utilities +0.52%, and energy +0.23%.

Northbound Stock Connect, the trading venue that allows foreign investors to buy Shanghai and Shenzhen listed stock via Hong Kong, had elevated volumes as foreign investors sold Shanghai stocks and bought Shenzhen stocks. Shanghai-listed stocks are mainly large companies/value stocks versus Shenzhen, which is geared towards more mid and small caps/growth stocks. Shanghai Connect volume leader Kweichow Moutai was sold by a small margin, China Tourism was sold nearly 2 to 1, and Ping An Insurance was sold nearly to 2 to 1 as well. Shenzhen Connect volume leaders were Luxshare, which was bought 7 to 5, Gree Electric Appliances, which was sold 3 to 1, and EV battery maker CATL, which was bought by 2 to 1. Foreign investors sold -$272mm worth of Mainland stocks as Northbound Stock Connect trading accounted for just over 6% of Mainland turnover.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.98 versus 7.01 yesterday

- CNY/EUR 8.26 versus 8.25 yesterday

- Yield on 1-Day Government Bond 1.40% versus 0.98% yesterday

- Yield on 10-Year Government Bond 2.97% versus 2.94% yesterday

- Yield on 10-Year China Development Bank Bond 3.48% versus 3.43% yesterday