“Kabuki Theater” Politics Weigh on Hong Kong, Tencent Bull Run Interrupted, Mainland Higher on PBOC Comments

5 Min. Read Time

Key News

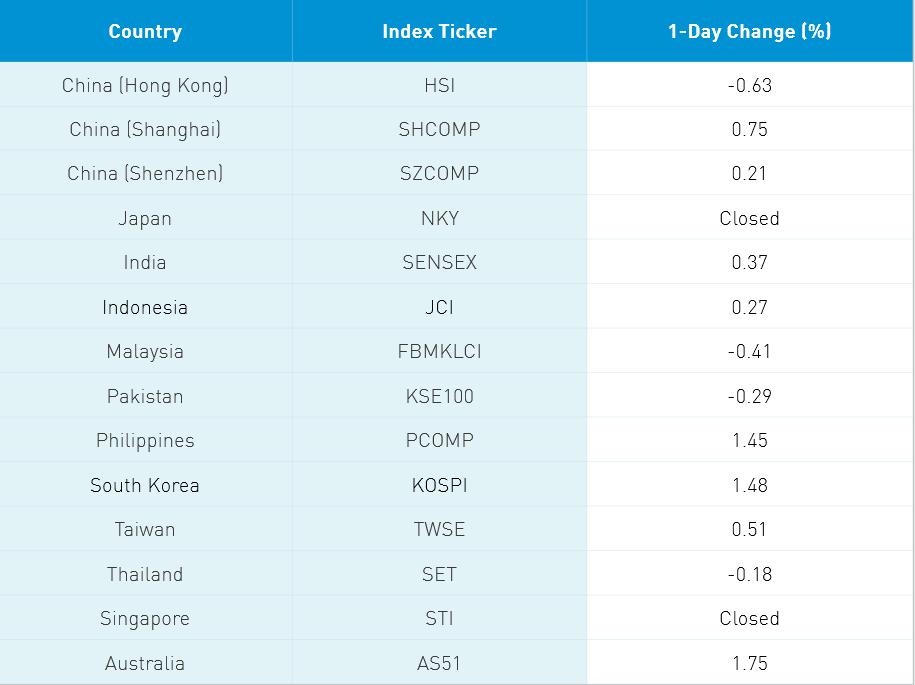

Asian equities were mixed as Japan and Singapore were closed today. Hong Kong and Mainland China diverged with the former slightly weaker on US-China political rhetoric, tit for tat travel sanctions on eleven China hawks including Sens. Marco Rubio and Ted Cruz, and the arrest of media tycoon Jimmy Lai. Mainland markets ended Monday modestly higher as PBOC Governor Yi Gang’s commented that monetary policy would be “flexible” and efforts to assist small medium enterprises in accessing credit would remain in place. Hong Kong volume leaders were Tencent -4.83%, accounting for -135 index points of the Hang Seng’s -154 index point drop, Alibaba HK -2.73%, Meituan Dianping +0.27%, Semiconductor Manufacturing -7.02%, HK Exchanges -1.94% and Macau casino operator Galaxy Entertainment +5.59% as the market anticipates a relaxing of travel restrictions. Tech stocks were weak on continued political rhetoric with Apple suppliers AAC -5.63% and Sunny Optical -2.83%.

Hong Kong growth stocks have had a very strong year so far, which has led some to take profits on the headlines though I don’t see their leadership role being unseated especially as we head into Q2 earnings. Remember, Hong Kong-listed stocks are foreign investors’ traditional definition of China, leading to higher headline risk than the Mainland stocks, which have relatively little foreign ownership.

Macau stocks were universally higher Monday though it is worth noting these companies are Hong Kong-domiciled companies meaning they are in the MSCI Hong Kong Index, which is part of developed market indices, and not MSCI China or MSCI EM. Mainland China saw large caps/value companies outperform mid/small cap/growth companies as financials and real estate were firmer than tech, which was weak in Monday trading.

Takeaway: PPI did increase +0.4% month over month as the rate of mining, raw materials and manufacturing goods declined at a lower rate than in June. PPI weakness is indicative of the economic consequence of global quarantines. China’s CPI also increased +0.6% month over month. A +13.2% jump in food prices due to supply disruptions following heavy rains and flooding accounted for most of the rise in inflation. Transportation and communication prices were soft -4.4% while recreation and education prices firmed +0.3% along with unsurprising medical good prices +1.6%.

Kabuki Theater is the traditional Japanese theater known for its intricate costumes and overly dramatic acting. I believe recent action on WeChat and, to a lesser degree, TikTok is a continuation of our “more bark than bite” thesis. Even today’s tit for tat travel bans have no real consequence outside of optics. US companies are doing very well in China and selling to its growing urban middle class. The two economies are far more intertwined than most realize.

US and China trade teams will connect at week’s end and both sides want to strengthen their positions going into the talks. The White House’s Working Group announcement last week reaffirmed the US delisting bill but assured that if a US auditor gets PCAOB approval to verify the audit the company would not be delisted. Sounds like an olive branch to me as virtually all of the US Chinese companies are audited by the Big Four auditors! I believe an element of the rhetoric is a distraction technique. There has been little examination of how well US companies are doing in China as evidenced by US companies’ Q2 earnings, which is discussed below. Companies place their factories in China in order to manufacture and sell, not only to China, but also to Asia’s 4 billion potential consumers. Ultimately, we need to take headlines with a grain of salt.

An institutional broker had a great note on the Q2 results of US multi-nationals operating in China. US consumer-geared companies almost universally noted strong e-commerce growth while restaurant companies experienced slower growth. Luxury goods providers reported strong China sales while US companies geared to construction showed resiliency

MSCI’s pro forma for the end of month Quarterly Index Review will be released on Wednesday after the US market close. We will likely see China’s weight in Emerging Markets increase slightly as Chinese equities have outperformed their peers in emerging markets. On Friday, following the close in Hong Kong, we find out whether Alibaba’s Hong Kong listing, Meituan Dianping, and Xiaomi will be added to the widely followed Hang Seng Index as part of the early September rebalance.

Tencent Music Entertainment (TME US) reports after the US close today. The Adjusted EPS estimate from analysts is RMB 0.64

Shout out to NBC News for sending a reporter to the Wuhan Institute of Virology to interview senior staff. Fact finding instead of conjecture and hyperbole. Kudos!

This morning two companies recently in the news reported Q2 financial results before the US market open. US-listed search engine Sogou (SOGO US), which is soon to be acquired by Tencent, reported Q2 financials with revenues that fell -14% year over year to $261mm as advertising dollars were weak. Offline/traditional retailers are rebounding far slower post-quarantine than their online equivalents as habits formed during China’s quarantine appear to be sticking. Companies dependent on advertisting dollars from traditional stores are suffering as budgets are cut. Online gaming streamer DouYu (DOYU US) also reported Q2 financial results this morning with revenue growing +33% to $354mm. The company showed fiscal restraint in keeping costs down this quarter while the company’s Q3 revenue forecast was strong with projected growth between +42% and +44%. Tencent, which owns large stakes in both companies, engineered the merger of DOYU with competitor HUYA.

H-Share Update

The Hang Seng opened lower and never got off the mat felling -0.63%/-154 index points to close at 24,377. Volume plunged -23% from Friday though remained above the 1-year average. Breadth was off with 19 advancers and 26 decliners. Tencent weighted on the index -4.83%/-135 index points, HK Exchanges -1.94%/-26 index points, and Macau casino operator Galaxy Entertainment +5.59%/+20 index points. Hong Kong-domiciled companies outperformed China-domiciled companies +0.06% versus -0.72%. The 205 Chinese companies listed in Hong Kong within the MSCI China All Shares Index fell -1.72% with financials +0.14%, discretionary +0.1%, industrials -0.1%, real estate -0.21%, energy -0.53%, staples -1.07%, utilities -1.31%, health care -2.31%, tech -3.41%, materials -3.85%, and communication -4%.

Southbound Stock Connect, the trading venue that allows Mainland investors access to Hong Kong stocks, saw moderate volumes in mixed trading. Investors can choose to trade through the Shanghai or the Shenzhen Stock Exchanges, both of which distribute buy and sell volume. I tend just to quote Shanghai volume over Shenzhen volume as the former tends to have higher volumes. Today’s Shanghai volume leaders were Tencent, which had more buy volume than sell volume by a small margin, indicating that Mainland investors bought more Tencent today than they sold. SMIC was sold 5 to 3 (sell volume exceed buy volume) and Meituan Diangping was bought 2 to 1. Mainland investors bought $348mm worth of Hong Kong-listed stocks today as Southbound Connect trading accounted for 12.5% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen opened lower but rose off the lows to close +0.75% and +0.21% at 3,379 and 2,277, respectively. Trading volume was off -8% from Friday though remained nearly 50% higher than the 1-year average. Breadth was positive with 2,689 advancers and 1,008 decliners. Large caps outperformed mid and small caps. The 510 Chinese companies within the MSCI China All Shares Index rose +0.13% with real estate +2.56%, financials +1.08%, energy +0.89%, communication +0.84%, utilities +0.61%, industrials +0.11%, staples -0.01%, health care -0.15%, discretionary -0.19%, tech -0.69%, and materials -1.37%.

Northbound Stock Connect, the trading venue that allows foreign investors to trade Mainland stocks, had moderate volumes as foreign investors were net buyers by a very small amount in mixed trading. Shanghai had more buying volume than Shenzhen, which was sold by nearly the same amount bought in a reversal of a long-term trend. Shanghai Connect volume leader Kweichow Moutai was sold by a small amount, China Tourism Group was bought by a small amount, and Ping An Insurance was sold by small amount. Shenzhen Connect volume leader Wuliangye Yibin was sold 10 to 7, Luxshare was sold 10 to 7 and Walvax Biotechnology was sold by small amount. Foreign investors bought $1mm of Mainland stocks today as Northbound Stock Connect trading accounted for 4.8% of Mainland turnover.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.97 versus 6.97 Friday

- CNY/EUR 8.20 versus 8.22 Friday

- Yield on 1-Day Government Bond 1.28% versus 1.20% Friday

- Yield on 10-Year Government Bond 2.95% versus 2.99% Friday

- Yield on 10-Year China Development Bank Bond 3.496% versus 3.52% Friday