Caixin Manufacturing PMI Exceeds Expectations, ATMX Rises Again

2 Min. Read Time

We have two webinars coming up in September. You can find the descriptions below.

1. China Macro Update: Digital Transformation & Structural Reforms Provide Catalysts For Post Covid-19 Growth

2. Covid:19: An Inflection Point For Emerging Markets Consumer Technology

Key News

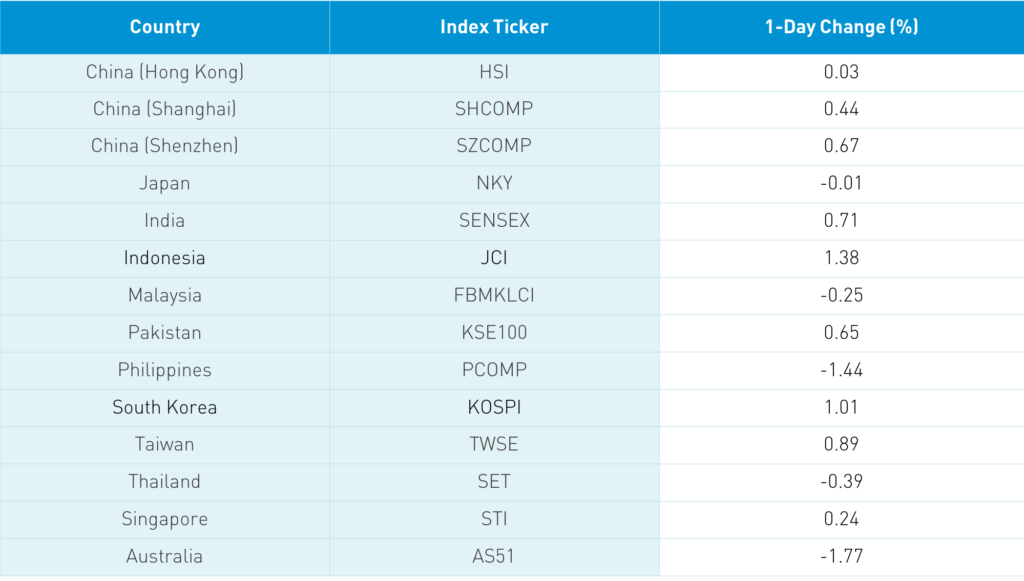

Asian equities had a mixed day as Hong Kong and Mainland China pulled out small gains while increased tension on the India-China border dampened sentiment. The PMI release didn’t have a large impact on the equity market today, though commodity markets will love the release. Materials stocks were strong on the PMI release and gold’s pick up. What did move the equity market was government policy supporting rural consumers as consumer discretionary stocks in Hong Kong and Mainland China outperformed. Car stocks also helped consumer discretionary stocks, as August auto sales firmed in China.

Hong Kong volume leaders were the ATMX stocks: Alibaba Hong Kong, which was unchanged, Tencent, which was up +1.6%, Meituan-Dianping, which gained +3.52%, and Xiaomi, which rose +8.4%. Mainland China rallied into the close on light volumes as defense stocks, discretionary, and materials outperformed. It is interesting that MSCI’s definition of Chinese companies in Hong Kong and Mainland China, the MSCI China All Shares Index, performed much better than the Hang Seng Index (Hong Kong) and the Shanghai & Shenzhen Indexes. We’ll take it! We also had another decline in the US dollar as the renminbi went up +0.44% versus the US dollar to close at 6.81.

Yesterday’s close required passive managers to implement changes following MSCI's index rebalance. I had previously noted that Peloton (PTON US) was being added. PTON US traded 15mm shares Monday, though nearly half of that volume was at the close when 7mm shares traded. The power of passive was on full display!

The “private” Manufacturing PMI for August was released at 9:45am local time.

Takeaway: The Caixin Manufacturing PMIs are calculated by IHS Markit (NYSE ticker INFO) through a survey of 500 private and state-owned enterprises versus the “official” PMI calculated by the National Bureau of Statistics through a survey of 5,000 companies. This was a very strong release as production and new orders grew faster than they grew July, export sales picked up for the first time in 2020, output increased to the highest level since January 2011, and new orders rose from July to the highest level since January 2011. Remember that PMIs are a diffusion index that compare month-over-month activity. Levels over 50 indicate growth month-over-month and vice versa. While employment fell slightly, its rate of decline narrowed. It is feasible that employment could turn up next month. The copper market noticed the positive release gaining 0.88%.

H-Share Update

The Hang Seng traded in a very tight range up +0.03%/+7 index points to close at 25,184 as volumes contracted 23% from yesterday. Breadth was off with 17 advancers and 30 decliners. Chinese domiciled companies were up +0.22% versus -0.23% using the HS China Enterprise and Hong Kong 35 indexes as proxies. The 204 Chinese companies within the MSCI China All Shares Index were up +1.04%. Southbound Stock Connect flows light with buyers outpacing sellers. Mainland investors bought $381mm of Hong Kong stocks today as Southbound Connect trading accounted for 9.6% of Hong Kong turnover.

A-Share Update

Shanghai & Shenzhen overcame a morning swoon to close up +0.44% and +0.67% at 3,410 and 2,310, respectively. Volumes slumped -17% to just above the 1-year average. Breadth was off with 1,688 advancers and 1,930 decliners as mid and small caps outperformed large caps by a small margin. The 517 Mainland stocks within the MSCI China All Shares Index gained +1.11%. Northbound Stock Connect volumes were moderate/light as foreign investors sold Shanghai stocks and bought Shenzhen stocks. Foreign investors sold -$43mm of Mainland stocks today as Northbound Connect trading accounted for 5.6% Mainland turnover.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.82 versus 6.85 yesterday

- CNY/EUR 8.18 versus 8.18 yesterday

- Yield on 1-Day Government Bond 1.05% versus 1.45% yesterday

- Yield on 10-Year Government Bond 3.05% versus 3.02% yesterday

- Yield on 10- Year China Development Bank Bond 3.63% versus 3.59% yesterday