Climbing The Wall of Political Worry, Week in Review

5 Min. Read Time

Week in Review

- Asian equities started the week and ended the month by trading mostly lower on Monday. The main culprit was MSCI’s Semi-Annual Index Review, which obligated passive investors to sell positions in Asian markets to make room for new index constituents from other regions.

- The Caixin China Manufacturing PMI for November came in at a decade-high 54.9 compared to an expected reading of 53.5 on Tuesday, indicating a greater expansion than had been anticipated. The positive release was mirrored by the services PMI, released Thursday, which also beat expectations after coming in at 57.8, indicating that the demand side recovery is catching up with the supply side.

- The China Banking and Insurance Regulatory Commission (CBIRC) on Tuesday implied it will tighten regulations on real estate lending and speculation, which many brokers believe could channel more household savings into China’s stock market.

- The Holding Foreign Companies Accountable Act has passed in both houses of Congress as of Wednesday. While headlines have emphasized the potential for delisting, the SEC has already come up with a viable solution that avoids punishing US investors. Click here to read our full analysis.

Key News

Yesterday, US-listed Chinese companies rose despite the House passing a bill Wednesday that, at face value, introduces the potential that the companies will be delisted after three years if they cannot have their audit papers reviewed by the PCAOB. As the bill goes to the President’s desk for signing, it is key to understand why the stocks brushed off the news. The White House Working Group on Financial Markets’ August 6th release included the below:

“Companies unable to satisfy this standard as a result of governmental restrictions on access to audit work papers and practices in NCJs may satisfy this standard by providing a co-audit from an audit firm with comparable resources and experience where the PCAOB determines it has sufficient access to audit work papers and practices to conduct an appropriate inspection of the co-audit firm.”

Bingo! The vast majority of US-listed Chinese companies are audited by the Mainland China subsidiaries of the Big Four (PWC, EY, Deloitte & KPMG) US accounting firms. So, if the US parent signs off on the audit, that means that the companies are complying. Remember, the SEC is responsible for determining compliance. Also, on November 20th, a spokesperson for the China Securities Regulatory Commission (CSRC, China’s version of the SEC) said that they want to solve this issue. After all, it is 2020 people: pick up a phone, hop on a Zoom, or (if possible) a plane, and figure this out.

Asian equities finished a positive week on a high note as markets dismissed the US adding four more companies to the sanctioned list.

The Wall Street Journal reported that the US Justice Department would dismiss charges against Huawei’s Meng Wanzhou if the company agrees to wrongdoing. The founder’s daughter has been stuck in legal limbo in Canada for two years so I assume they’ll want to put it to bed.

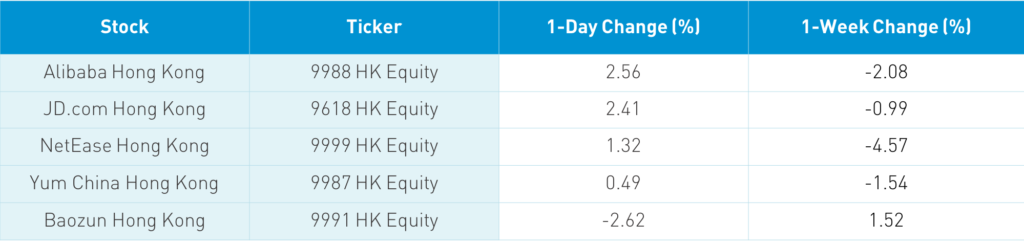

The Hang Seng Index gained 0.4% overnight as the index rebalanced today, adding Meituan, which gained +4.64% on 2X the volume of Tencent’s -0.08% decline. I mentioned all week that Meituan’s weakness was strange due to today’s inclusion. It is always good to get one right. Both Meituan and Tencent saw healthy buying by Mainland investors via the Southbound Connect today. Hong Kong’s other volume leaders were Alibaba Hong Kong, which gained +2.56% after Ant and e-commerce rival Sea were given a Singapore digital banking license, Ping An Insurance, which gained +2.62%, Xiaomi, which gained +0.2%, HSBC, which gained +0.81%, Semiconductor Manufacturing (SMIC), which fell -5.41%, China Construction Bank, which gained +0.5%, energy giant CNOOC, which fell -3.9%, and JD.com Hong Kong, which gained +2.41%.

There was some chatter that, within growth names, the electric vehicle sector is seeing some profit-taking after Li Auto issued shares at a healthy discount. The resulting flows appear to be heading to internet and e-commerce.

The jock growth stocks outperformed the nerd value stocks today. Real estate was off in both Hong Kong and Mainland China as a government official once again stated that “housing is for living and not speculating”. Shanghai pulled a James Bond, gaining +0.07% while Shenzhen rose +0.5%. Mid and small caps outperformed in Shenzhen. The DND trade (drugs, i.e. pharma, and drinks, i.e. alcohol) did well today as Mainland volume leader Kweichow Moutai gained+2.52% and rival Wuliangye Yibin gained +2.13%. Meanwhile, health care saw a broad rally.

Foreign investors bought a healthy $572 million worth of Mainland stocks today via Northbound Stock Connect, bringing the week’s total to $3.738 billion. We mentioned a few weeks ago that the 20 largest US active EM funds are all underweight China! Looks like that might be changing. Year-to-date, foreign investors have bought $24.486 billion worth of Mainland stocks.

CNY hit another 52-week low versus the USD, closing -0.16% to 6.53 from yesterday’s 6.54. The dollar’s decline is something else. It is amazing that there is chatter China’s V-shaped economic recovery could see interest rates raised in 2021!

It is being reported that JD Health’s Hong Kong IPO is trading up 27% in the “grey market,” which is the term used for describing brokers’ making a market in stocks pre-IPO.

SMIC and energy giant CNOOC were added to the Defense Department’s sanctioned list. For index providers, I would assume MSCI and FTSE will drop the stocks. No problem! Index funds, ETFs and mutual funds will drop the stocks. That being said, the Executive Order creates a massive problem for the US and global financial community. What happens to China Mobile’s US ADR? China Mobile is part of the Hang Seng Index. Are US financial firms now not allowed to trade Hang Seng futures? What about structured products in Asia from US financial firms? Swaps off of the CSI 300 that hold SMIC and CNOOC? So many questions and so few answers. Generation Z Tik Tok users came together and sued to challenge the EO concerning Tik Tok. Shouldn’t someone do the same on this EO? The problem is that no financial firm wants the press surrounding a legal challenge.

Guess how many IPOs were in Mainland China this year. 340. Not a typo! 340!!!

H-Share Update

The Hang Seng rose into the close +0.4%/+107 index points at 26,835. Volume jumped +27%, which is 139% of the 1-year average while breadth was off with 22 advancers and 25 decliners. The 203 Chinese companies listed in Hong Kong within the MSCI China All Shares Index rose +0.32% led by staples 2.63%, discretionary +2.53% and financials +0.69% while energy -2.82%, real estate -1.82%, utilities-1.41% and tech -0.63%. Southbound Connect volumes were moderate with Mainland investors buying $708mm of Hong Kong stocks as South Connect trading accounted for 8.7% of Hong Kong turnover.

A-Share Update

Shanghai & Shenzhen rose into the close +0.07% and +0.5% to 3,444 and 2,301 respectively. Volume was off -7% from yesterday, which is 89% of the 1-year average while breadth was mixed with 1,828 advancers and 1,899 decliners. The 522 Mainland stocks within the MSCI China All Shares +0.9% led by staples +2.89%, health care +1.79%, materials +1.62%, and industrials +1.15% while real estate -1.19% and financials -0.74%. Northbound Stock Connect volumes were moderate/light as foreign investors bought $572mm of mainland stocks as Northbound trading accounted for 5.4% of Mainland turnover.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.53 versus 6.54 yesterday

- CNY/EUR 7.94 versus 7.96 yesterday

- Yield on 1-Day Government Bond 1.32% versus 1.13% yesterday

- Yield on 10-Year Government Bond 3.27% versus 3.29% yesterday

- Yield on 10-Year China Development Bank Bond 3.72% versus 3.73% yesterday

- China's Copper Price +0.46%