Quiet on the Western Front

2 Min. Read Time

Key News

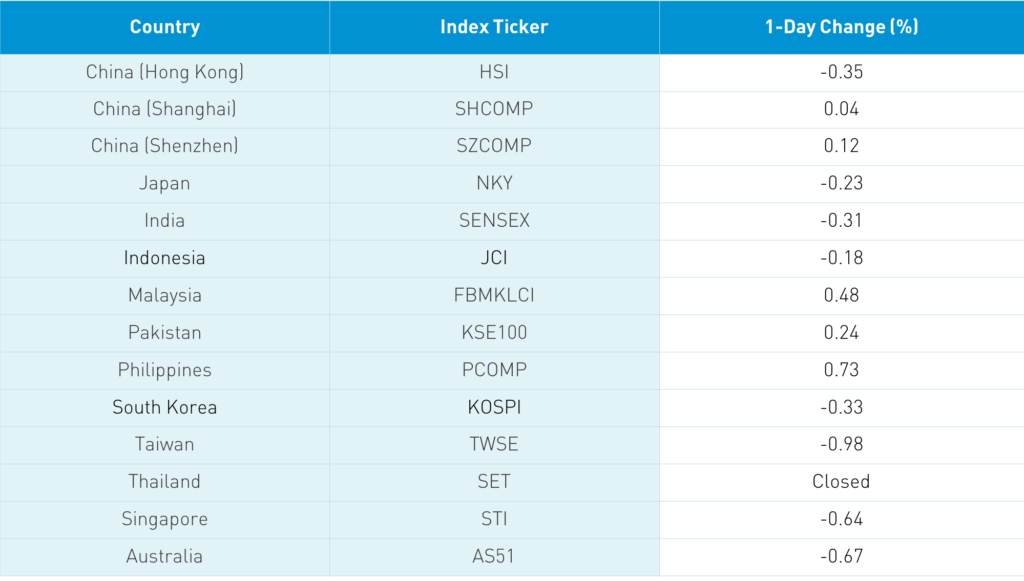

Asian equities followed the US’ tech-driven fall overnight with mild losses on light volumes. It’s interesting to note that South Korea’s Kospi was off -0.33%, but its Kosdaq was up +0.86%. The Hang Seng Index was off -0.35%, led by Hong Kong volume leaders Tencent, which fell -1.2% despite another day of Mainland buying via Southbound Stock Connect, Xiaomi, which rose +0.36%, Alibaba Hong Kong, which dropped -2.07%, Meituan, which gained +0.21%, energy giant CNOOCC, which fell -2.38%, JD.com, which fell -0.68%, JD Health, which was up +0.27%, Ping An Insurance, which rose +0.11%, Sunny Optical, which fell -3.39% on weak November shipments, China Mobile, which dropped -0.55%, and AIA, which gained +0.62%. Autos were weak on Tesla’s downgrade.

Mainland China bucked the regional weakness, managing small gains on light volume. There are rumors that insurance companies’ equity investment cap will be raised. Healthcare was higher after a Chinese coronavirus vaccine reported strong results in clinical trials. Foreign investors were net buyers of Mainland stocks to the tune of $232 million while CNY was flat.

A few weeks ago, we noted that Hong Kong and Mainland regulators had signed an agreement in 2019 allowing Hong Kong-listed Mainland companies to provide access to their audit papers. The South China Morning Post reported that “The Supervision and Evaluation Bureau of China’s finance ministry passed the auditors’ working papers of seven companies on Friday to the Financial Reporting Council (FRC, which oversees the auditing of companies listed in Hong Kong).” The move could provide a template for US-listed Chinese companies to follow suit, though we’ve repeatedly stated that the White House Working Group provides a path for compliance by allowing the companies’ US auditors to validate their Mainland subsidiaries' work. Remember that the US auditors’ China subsidiaries do the audit work on US multinational's China units.

The Wall Street Journal has reported that President-elect Biden will nominate Katherine Tsai as US Trade Representative, replacing Robert Lighthizer. We are seeing several career diplomats joining the Biden team, which should help communication and dialogue. I believe progress can be made due to China hosting the Winter Olympics in two years as there will very likely be an effort to solve issues in advance of the 2022 event.

S&P announced it will be dropping ten Chinese companies comprising of eighteen stocks from indices effective Monday December 21, 2020. The move follows FTSE’s move of simply dropping the names. MSCI is likely to make a similar announcement soon. While not a big deal, it is a bit disheartening that no one has legally challenged the Executive Order, which was clearly done hastily.

H-Share Update

The Hang Seng opened lower and stayed there closing down -0.35%/-92 index points at 26,410. Volume was off -19% from yesterday, which is -13% below the 1-year average while breadth was off with 17 advancers and 34 decliners. The 203 Chinese companies within the MSCI China All Shares Index fell -0.66%, led by real estate +0.42%, while energy was off -1.43%, communication -1.11%, financials -0.95%, staples -0.73%, and materials -0.58%. Southbound Connect volumes were light as Mainland investors bought $238mm of Hong Kong stocks as Southbound trading accounted for 9.9% of Hong Kong turnover.

A-Share Update

Shanghai & Shenzhen managed small gains of +0.04% and +0.12% closing at 3,373 and 2,253 respectively. Volume was off by -10.8% from yesterday, which is -16% below the 1-year average while breadth was off with 1,749 advancers and 1,958 decliners. The 522 Mainland stocks within the MSCI China All Shares Index rose +0.08%, led by heath care +1.18%, tech +0.61%, and communication +0.39%, while utilities fell -0.77%, financials -0.47%, and materials -0.46%. Northbound Stock Connect volumes were moderate as foreign investors bought $232mm of Mainland stocks today as Northbound trading accounted for 5.5% of Mainland turnover.

Last Night's Exchange Rates & Yields

- CNY/USD 6.54 versus 6.54 yesterday

- CNY/EUR 7.94 versus 7.92 yesterday

- Yield on 1-Day Government Bond 1.16% versus 1.19% yesterday

- Yield on 10-Year Government Bond 3.26% versus 3.27% yesterday

- Yield on 10-Year China Development Bank Bond 3.69% versus 3.71% yesterday