Mainland Moves Lower On Eve of Major Policy Meeting

3 Min. Read Time

Upcoming Event This Week:

What’s Next for China in 2021? A-Share Inclusion and Macro Update with MSCI

Thursday, December 17th at 11 am EST

Click here to register

Key News

Asian equities were largely off on light volumes as positive vaccine news is offset by the reality of rising coronavirus cases globally. Mainland China outperformed, but still moved lower. It was a fairly quiet night as investors are likely closing up their books for the year.

The Hang Seng Index was off as investors once again unloaded internet plays and replaced them with autos, healthcare, and clean energy plays. Hong Kong volume leaders were Tencent, which fell -1.93%, Xiaomi, which gained +1.2%, Meituan, which fell -2.97%, Alibaba Hong Kong, which fell -2.23%, JD.com Hong Kong, which dropped -2.79%, Geely Auto, which rose +2.67%, AIA, which fell -0.39%, China Construction Bank, which fell -0.35%, JD Health, which rose +4.71%, and Ping An, which fell -0.69%.

It is hard for me to believe that the new anti-monopoly law will have a detrimental effect on the long-run prospects of these companies. I imagine investors may quickly regret selling these companies considering their alignment with China’s growing domestic consumption, which one research firm says will account for 60% of China’s GDP growth in 2021. Shanghai and Shenzhen had a choppy session but rallied into a divergent close, falling -0.06% and rising +0.39%, respectively, though growth companies outperformeddriving mid and small caps higher.

In addition to the strong economic release, we also have the Central Economic Work Conference (CEWC) taking place this week. Policymakers will review the Five-Year Plan draft and start the process of articulating a game plan. The Five Year Plan will be announced in the spring. The CEWC is likely to provide further positive news around favored sectors such as clean energy, EV, domestic consumption, and 5G. These growth companies outperformed overnight, and they could continue to do so as CEWC news leaks out. Foreign investors bought $66 million worth of Mainland stocks overnight as the CNY eased a touch versus the US dollar. Copper was off a touch and bonds rallied.

There has been a fair amount of discussion surrounding Baidu entering the EV space, which is not surprising considering the investment made in autonomous driving technology.

The Global Industry Classification Standard (GICS) is a consortium of two index providers comprised of MSCI and S&P Dow Jones that determine what sector a stock is classified under. There are competitors such as Bloomberg’s BICS and ICB, which is determined by FTSE Russell. Would you believe that JD Health, Alibaba Health, and Ping An Health are considered consumer staples by BICS? Even more confusing, GIC considers JD Health consumer discretionary, while Alibaba Health and Ping An Health are considered healthcare. If you’re not scratching your head, reread the above.

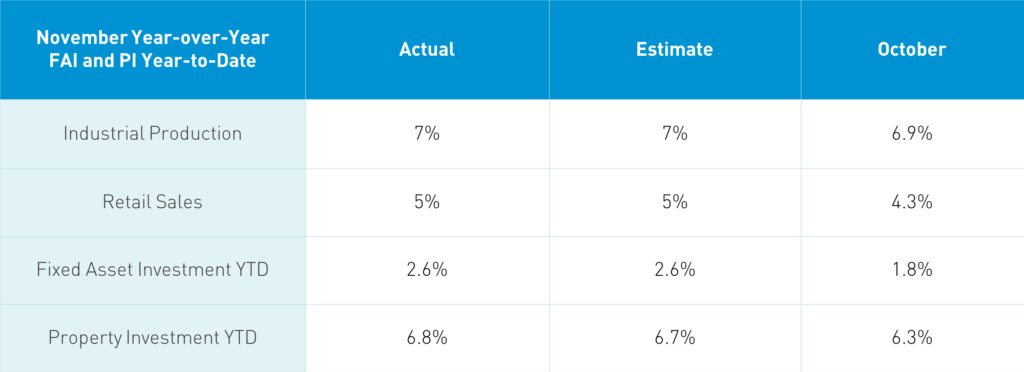

Takeaway: The economic release occurred shortly after the market opened. Retail sales increased +5% year-over-year and month-over-month is driven by the strong Singles Day event, as cosmetics rose +32%, jewelry +24%, and communication appliances +43%. YTD online retail sales have increased +11.5% year-over-year, accounting for 25% of the total retail sales of consumer goods. Autos had a strong reading, up +11.8% YoY, while medicine was up +12.8%, and office supplies +11.2%. I find the results quite impressive! Industrial Production was inline, driven by manufacturing, which rose +7.7%, while on an industry level, pharmaceutical gained +13.6%, metal products +13.8%, machineries +18%, auto manufacturing +11.1%, and both general and specially used equipment +10.2% and +10.5% respectively. Diving into the nitty-gritty, electricity production increased by 6.8% in November, which is up 2.2% from October. Many track electricity usage as a measure of economic activity. Fixed Asset Investment was driven by strong readings in pharmaceutical, which rose +27%, and health care, which rose +23.7%, with telecom/computers gaining +17.5% and agriculture +18%. Otherwise, most industries were off on a year-over-year basis. Overall, this is a very strong report as anticipated.

H-Share Update

The Hang Seng opened lower and stayed there closing down -0.69%/-182 index points at 26,207. Volume was up +0.4% from yesterday, which is 13% above the 1-year average. The 203 Chinese companies listed in Hong Kong within the MSCI China All Shares Index fell -0.47%, with healthcare up +2.85%, staples +0.96%, and utilities +0.84%, while communication fell -1.75%, energy -1.1%, and discretionary -1.1%. Southbound Stock Connect volumes were moderate/light as Mainland investors bought $66mm of Hong Kong stocks as Southbound trading accounted for 10.3% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen bounced around the room closing -0.06% and +0.39% closing at 3,367 and 2,256 respectively. Volume was basically flat off -0.5% from yesterday, which is -17% below the 1-year average while breadth was off with 1,647 advancers and 2,085 decliners. The 522 Mainland stocks within the MSCI China All Shares Index rose +0.12%, led by healthcare +1.77%, discretionary +0.99%, industrials +0.83%, and communication +0.76%, while real estate fell -1.22%, financials -0.71%, and utilities -0.64%. Northbound Stock Connect volumes were moderate as foreign investors sold -$53mm of Mainland stocks today as Northbound trading accounted for 6.5% of Mainland turnover.

Last Night's Exchange Rates & Yields

- CNY/USD 6.54 versus 6.55 yesterday

- CNY/EUR 7.95 versus 7.95 yesterday

- Yield on 1-Day Government Bond 1.35% versus 1.35% yesterday

- Yield on 10-Year Government Bond 3.28% versus 3.29% yesterday

- Yield on 10-Year China Development Bank Bond 3.68% versus 3.70% yesterday