Year-End Profit Taking Rules the Day, JD Health Joins Southbound Connect, Potential Kuaishou IPO

3 Min. Read Time

Key News

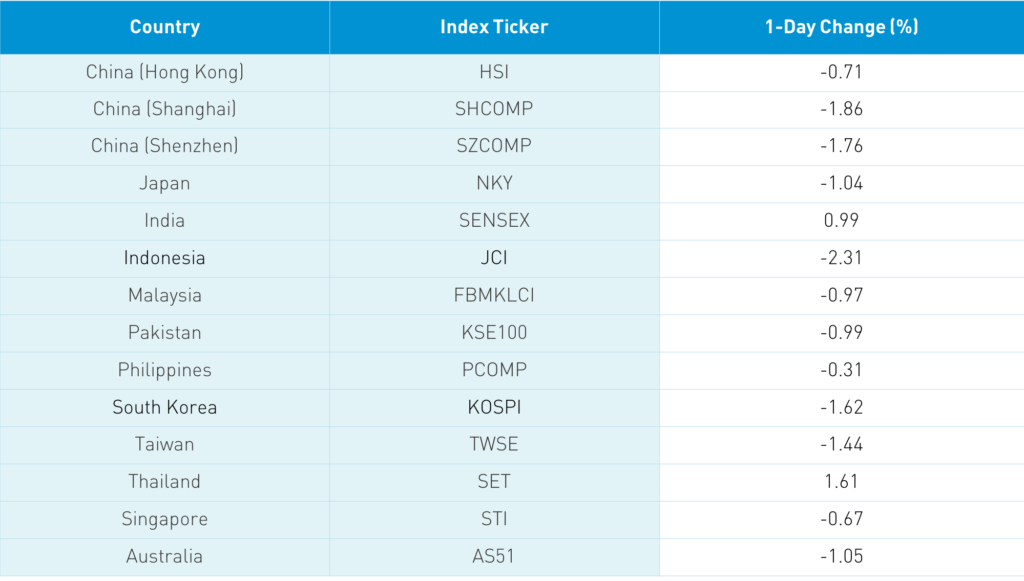

Asian equities were a sea of red with the exception of India and Thailand. Mainland China was off almost -2%, with some pointing to the stimulus being pulled. I disagree with the assessment, as we noted the Central Economic Work Conference stated yesterday that economic support would continue and be dialed back incrementally.

Mainland brokers universally pointed to the global rise in coronavirus cases as the culprit, which could lead to a rise in lockdowns and thus weigh on the global economy along with the expansion of the US’ technology export ban. We did have a Mainland media source note the strong rise of iron ore futures, which led to commodity prices falling. Copper futures were off -1.27% while energy and material stocks were hit in both Hong Kong and China.

Shanghai & Shenzhen were off by -1.86% and -1.76% respectively as profit-taking led to a pick-up in volume. Mainland liquor stocks and healthcare stocks were rare outperformers. The Hang Seng Index was off -0.71% as growth stocks fared better. Hong Kong volume leaders were Tencent, which rose +0.09%, JD Health, which gained +9.88% after being added to Southbound Connect today, Xiaomi, which was up +1.19%, Meituan, which fell -0.79%, Alibaba Hong Kong, which dropped -0.48%, BYD, which was off -6.24%, Ping An, which fell -1.88%, China Mobile, which dropped -0.91%, GCL-Poly energy, which was off -12.08% and Geely Auto, which fell -5.35%. I didn’t receive my morning note from a large Hong Kong broker, in an indication that many folks have started their holidays. Volume was light today. Foreign investors sold -$548mm of Mainland stocks while Chinese bonds rallied, and CNY appreciated a touch versus the US $.

Hang Seng Indexes Company Limited announced a consultation considering an expansion of the 52 stock Hang Seng Index (HSI) to include 65 to 80 stocks. The problem for the HSI is the sector exposure due to its 43% weight to financials! It isn’t a state-owned enterprise. New China growth stocks have vastly outperformed Old China value stocks in the last decade, though the weight in financials has weighed on the Hang Seng Index’s performance. By increasing the number of stocks, it would diminish the weight of financials, which up until recently was over 50% of the index. Some might point to the move as signs of a growth top, similar to the S&P 500’s addition of Tesla, though in the long run, the move does make sense if pursued.

The SCMP reported that Bytedance/Tik Tok’s rival Kuaishou is planning for a Hong Kong IPO. The move makes sense for Kuaishou to raise money to press its efforts against rival Bytedance. According to Bloomberg, the company has an expected value of $50 billion while looking to raise $5 billion.

Sina, the first US-listed Chinese company, will take its go-private offer to its shareholders today. Having listed back in April 2000, Sina followed a very similar path as fellow web portal Yahoo as e-commerce, online gaming, online education, and online video came to dominate web usage. Since the IPO, Sina has returned +189% versus the Nasdaq Composite’s 316% return though it had two tremendous runs in 2010/2011 and in 2017/2018. However, the returns have fallen on hard times recently. Hat tip for Sina paving the way as we bid adieu!

Asia and China scholar Ezra Vogel passed away this past weekend. While not necessarily a household name, the Harvard professor Vogel was a giant for his contributions to the West’s understanding of China and Japan. It would be easy to note the professor’s passing with the current state of US-China relations, though that would take away from his contributions in establishing US-China relations.

H-Share Update

The Hang Seng sold off in the afternoon to close down -0.71%/-82 at 26,119. Volume was off -14% from yesterday, which is -3% below the 1-year average while breadth was had just 9 advancers and 42 decliners. The 204 Chinese companies listed in Hong Kong were off -0.59%, with utilities and tech up +0.45% and +0.05%, while materials fell -3.21%, industrials -1.52%, energy -1.31%, discretionary -1.11%, and financials -0.98%. Southbound Stock Connect volume was light/moderate with Mainland investors bought $88mm of Hong Kong stocks as Southbound trading accounted for 12.2% of Hong Kong turnover.

A-Share Update

Shanghai & Shenzhen sold off into the close down -1.86% and -1.76% at 3,356 and 2,264 respectively. Volume increased 10% from yesterday, which is 13% above the 1-year average while breadth was way off with only 574 advancers and 3,171 decliners. The 521 Mainland stocks within the MSCI China All Shares Index fell by -1.5%, with staples up +0.53% while energy dropped -3.94%, materials -2.8%, financials -2.7%, tech -1.87%, discretionary -1.76%, utilities -1.73%, industrials -1.72%, and communication -1.61%. Northbound Stock Connect volumes were moderate as foreign investors sold -$548mm of Mainland stocks as Northbound trading accounted for 6.1% of Mainland turnover.

Last Night's Exchange Rates & Yields

- CNY/USD 6.54 versus 6.55 yesterday

- CNY/EUR 7.99 versus 8.00 yesterday

- Yield on 1-Day Government Bond 0.55% versus 0.65% yesterday

- Yield on 10-Year Government Bond 3.23% versus 3.27% yesterday

- Yield on 10-Year China Development Bank Bond 3.61% versus 3.64% yesterday