Xiaomi Takes $11 Billion Sanction Hit, Chinese Financials Pre-Announce Positive Earnings, Week in Review

4 Min. Read Time

Week in Review

- Asian equities began the week mixed on high volumes. Hong Kong stocks outpaced Mainland China as Mainland investors buy Executive Order banned stocks in Hong Kong, knowing that foreign investors have to sell regardless of price. Nearly 500 structured products have been unwound by US banks in Hong Kong as a result of the order.

- Financials outperformed on Tuesday following news that Chinese regulators will now allow them to offload non-performing loans to asset managers.

- Alibaba announced plans for an electric vehicle joint venture with SAIC Motors Wednesday.

- Tencent Music, Joyy, Vipshop, Bilibili, Didi Chuxing, and Kuaishou are all gearing up for Hong Kong listings later this year.

- China’s export growth in December beat estimates coming in at 18%. China’s exports grew at an impressive pace throughout most of the second half of 2020, fueled by pandemic-induced demand for medical products.

Key News

Asian equity markets saw a bout of profit taking accompanied by higher volumes as South Korea and India underperformed.

The US Department of Defense added Xiaomi and eight other companies to the list of companies affiliated with the Chinese military. However, as of yet, the Office of Foreign Asset Control (OFAC) has not added the company to its sanctioned list. If OFAC were to do so, the US financial industry would have sixty days to divest holdings of Xiaomi’s Hong Kong listing, which makes cell phones, battery rechargers and Alexa-like devices. The sanction list delivers a guilty verdict without evidence though this might be breaking point for someone to step up and challenge this Executive Order in court. Xiaomi publicly stated overnight that it has no connection to the Chinese military. I have sarcastically called the Executive Order the Hong Kong investment banker employment act as Chinese companies are apt to pivot to Hong Kong over New York. Taking out one of the world’s top five largest mobile phone makers seems like a stretch as $11 billion worth of investment value were wiped out last night due to the selloff in Xiaomi’s stock. Hopefully, this is the final curtain call for stock bans.

China Merchants Bank and ICBC pre-announced positive earnings, leading to a nice rally in financials in both Hong Kong and Mainland China.

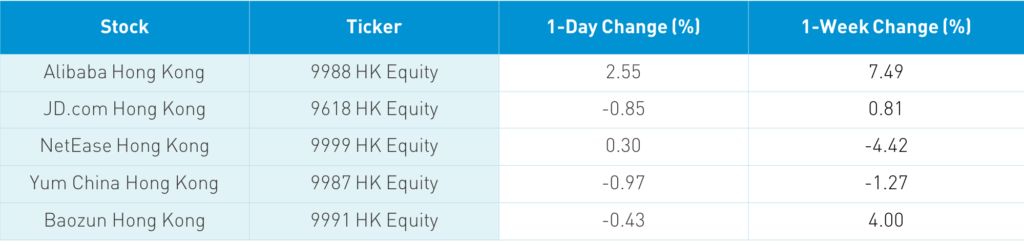

The Hang Seng Index, which includes Xiaomi, gained +0.27% while the Chinese companies listed in Hong Kong within the MSCI China All Shares Index gained +0.26%. Xiaomi, a volume leader in Hong Kong, plunged -10.26% on massive volume, Tencent gained +2.46%, Alibaba HK gained +2.55%, Yidu Tech’s IPO surged +147%, Ping An Insurance gained +3.51%, fellow sanction stock Semiconductor Manufacturing fell -1.78%, Meituan fell -1.79%, Geely Auto fell -4.88%, China Mobile fell -0.11%, and Guangzhou Auto gained +19.49%. Massive volumes were seen in Southbound Stock Connect trading overnight as Mainland investors bought Tencent, Meituan, and, to some degree, Xiaomi. Southbound Connect accounted for 15% of Hong Kong turnover, which 50% above the 1-year average. Meanwhile, health care was off as several companies sold shares.

Shanghai and Shenzhen gained +0.01% and +0.27%, respectively, as financials outperformed while growth and recently outperforming sectors were clipped thanks to profit taking once again.

We seem to be getting the classic post-breakout pullback. Next week, we will find out whether the previous resistance level becomes the support level or if the breakout “fills the gap,” i.e. falls back from the breakout.

Foreign investors bought $123 million worth of Mainland stocks today, which raises the weekly total of net purchases to $2.776 billion. That is a big week!

CNY was off a touch versus the dollar as every headline says that China hates the strong CNY while all of our brokers target CNY appreciation to between 6 to 6.20 per US dollar. Bonds sold off today while copper eased a touch.

Pinduoduo will not sponsor CCTV’s Spring Festival Gala, which celebrates Chinese New Year and is in the Guinness Book of World Records for the largest TV audience. The e-retailer has had two unfortunate incidents lately, the first of which was the death of an employee after a very long workday followed by an employee’s suicide. Chinese internet companies’ employees are known for working 996: 9am to 9pm, 6 days a week. The company is avoiding the spotlight in light of these two instances. I do not see how this would materially affect the company. However, given its recent strong performance, we could see some profit taking in the near-term.

It is being reported that Kuaishou’s Hong Kong IPO will occur on February 5th.

H-Share Update

The Hang Seng bounced around the room to close +0.27%/+77 index points at 28,573. Volume jumped +22% from Thursday to nearly twice the 1-year average while breadth was off with 16 advancers and 35 decliners. The 197 Chinese companies listed in Hong Kong and included in the MSCI China All Shares Index gained +0.26% led by financials +2.57% and communications +2.39%. Meanwhile, tech -5.17%, discretionary -1.48%, health care -1.28%, and staples -1.05%. Southbound Stock Connect volumes were high as Mainland investors bought $1.732 billion worth of Hong Kong stocks today as Southbound Connect trading accounted for 15.3% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen staged a late-day rally to close +0.01% and +0.27% at 3,566 and 2,366, respectively. Volume was off -7.6% from yesterday, which is still +20% above the 1-year average. Meanwhile, breadth was decent with 2,751 advancers and 1,055 decliners. The 513 Mainland Chinese companies within the MSCI China All Shares Index were off -0.44% led by financials +1.63%. Meanwhile, staples were off -2.34%, tech -1.99% and utilities -0.74%. Northbound Stock Connect volumes were high as foreign investors bought $123 million worth of Mainland stocks today. Northbound trading accounted for 6.9% of Mainland turnover.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.48 versus 6.47 yesterday

- CNY/EUR 7.84 versus 7.85 yesterday

- Yield on 1-Day Government Bond 1.41% versus 1.35% yesterday

- Yield on 10-Year Government Bond 3.15% versus 3.11% yesterday

- Yield on 10-Year China Development Bank Bond 3.54% versus 3.51% yesterday