Economic Data Leads Markets Higher

2 Min. Read Time

New Report

Click here to download our newest report: 2021 China Outlook: Full Steam AheadKey News

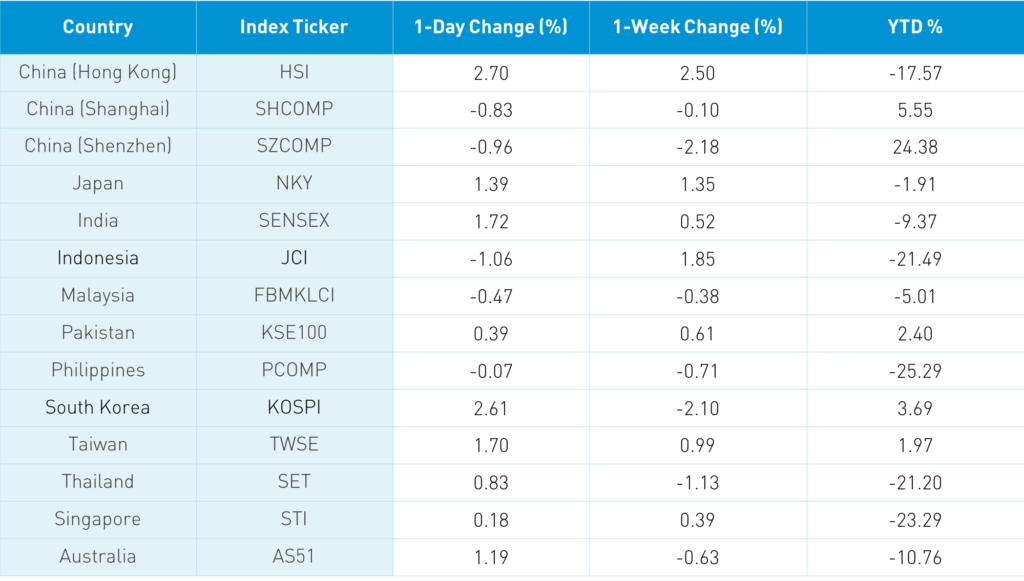

Asian equities had a strong day, almost the complete opposite of yesterday. Japan, Taiwan, and South Korea ripped today after falling yesterday. Shanghai & Shenzhen were up yesterday following the strong economic data, though off today on profit-taking. Hong Kong was the rare two-day winner. There were several catalysts beyond yesterday’s strong economic data:

- MASSIVE buying of Hong Kong stocks from Mainland investors via Southbound Stock Connect as yesterday’s record inflow was surpassed today. Southbound Stock Connect volumes were exceedingly high, running 3X the average as Mainland investors bought $3.43 billion of Hong Kong stocks. Southbound Connect trading accounted for 17.6% of Hong Kong turnover. US investors are being forced to sell Executive Order stocks, which local investors are happily buying.

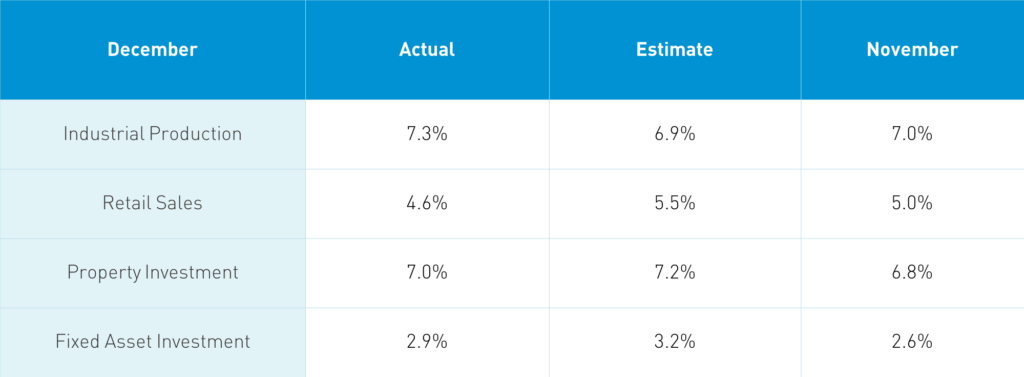

- Real estate: for China bears, China Evergrande must feel like a cat with nine lives after pre-paying a $2B bond payment due in February, which is a strong statement by the company. The market is anticipating that the vast majority of property developers will meet new regulations while yesterday’s property investment data improved in December from November.

- Mainland Investors are buying Chinese mutual funds at a very strong pace according to several Mainland brokers. I need to do further digging on this.

Takeaway: First-In/First-Out along with a strong quarantine.

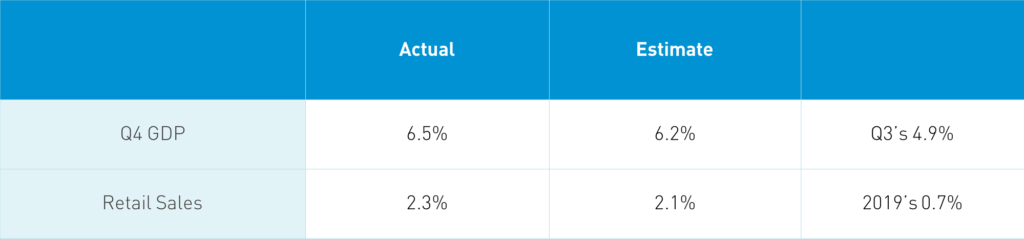

Takeaway: China’s old economy is being driven higher by foreign demand, real estate/property development, and internal stimulus, though retail sales were a touch light. This is an ideal Hansel and Gretel of the porridge – not being too hot nor too cold. Too hot would lead to supportive policies being pulled, which, after this data release isn’t going to happen soon. Retail sales' weaknesses will be front and center for policymakers as the service sector now accounts for 50% of GDP. An element of China’s recovery has been foreign demand for health care and work for home essentials such as laptops and desktop computers, which will diminish in the future.

H-Share Update

The Hang Seng gained +2.7%/+779 index points to close at 29,642. Volumes jumped +34% from yesterday, which is more than 2X the 1-year average while breadth saw 48 advancers and 3 decliners. Clean energy stocks had another strong day. Hong Kong volume leaders were Tencent, which fell -0.3% after hitting an all-time yesterday, Xiaomi, which rose +5.02%, Meituan, which gained +4.92%, Hong Kong Exchanges, which gained +3.94%, Alibaba Hong Kong, which was up+0.91%, Semiconductor Manufacturing, which gained +1.2%, China Mobile, which rose +1.42%, GCL-Poly energy, which was up +10.59%, Ping An, which gained +0.1%, and AIA, which rose +4.41%. The 197 Chinese companies listed in Hong Kong within the MSCI China All Shares Index gained +2.11%, led by real estate +7.11%, health care +3.95%, tech +3.72%, discretionary +3.61%, industrials +2.37%, energy +2.19%, staples +1.91%, financials +1.51%, and utilities +1.16%, while communications fell -0.14%.

A-Share Update

Shanghai & Shenzhen were hit by profit-taking -0.83% and -0.96% to close at 3,566 and 2,378 after gaining +0.65% and +1.29% yesterday. Volume was up +4.73% from yesterday, which is 20% above the 1-year average while breadth saw 2,184 advancers and 1,623 decliners. The 512 Mainland Chinese stocks within the MSCI China All Shares Index fell -1.24%, with real estate gaining +2.24%, utilities +1.04%, and financials +0.17%, while materials fell -2.17%, discretionary -2.03%, industrials -1.95%, staples -1.8%, health care -1.77% tech -1.72%, and communication -0.7%. Northbound Stock Connect volumes were high as foreign investors bought $141mm of Mainland stocks as Northbound Connect trading accounted for 7.2% of Mainland turnover.

Last Night's Exchange Rates & Yields

- CNY/USD 6.48 versus 6.49 yesterday

- CNY/EUR 7.86 versus 7.84 yesterday

- Yield on 1-Day Government Bond 1.84% versus 1.71% yesterday

- Yield on 10-Year Government Bond 3.16% versus 3.17% yesterday

- Yield on 10-Year China Development Bank Bond