Mainland Investors Insatiable Appetite for Hong Kong Stocks

4 Min. Read Time

Key News

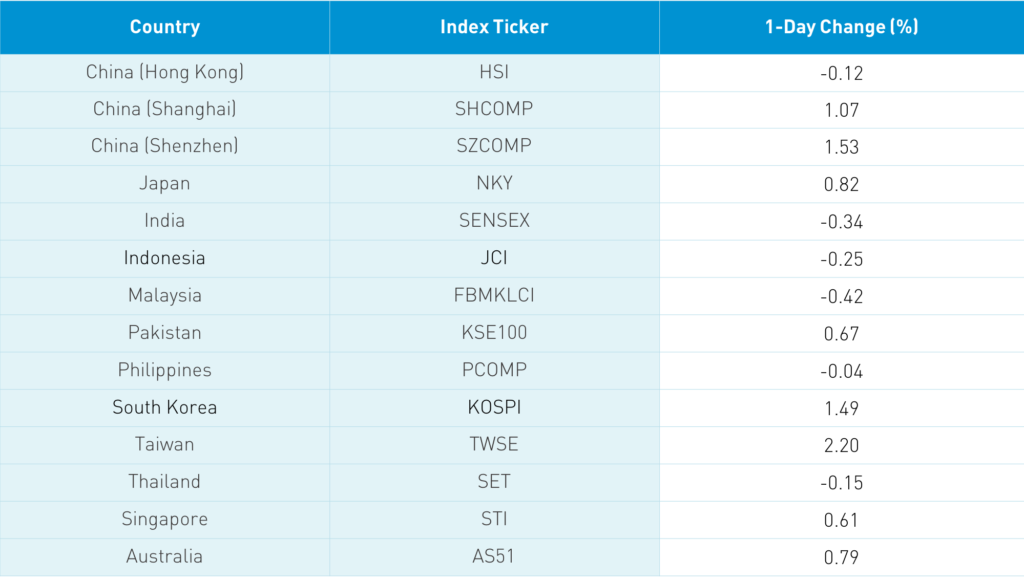

Asian equities were largely higher with Korea, Taiwan, and China outperforming while the Hang Seng took a breather from its recent run, challenging the 30,000 level. The market largely shrugged off reports that the PBOC will implement anti-monopoly rules on mobile payment providers, which is code for Alibaba’s Ant Group and Tencent’s WePay who have a duopoly. Ant has had significantly more revenue exposure than Tencent as evidenced by Tencent gaining +0.44% versus Alibaba Hong Kong falling -2.42%. If mobile payments users are limited to a percentage of market share, that should benefit others as JD.com Hong Kong rose +1.59%. It will be interesting to see exactly how the PBOC will regulate market share. As a comparison, Google’s massive market share over Bing and Yahoo is driven by consumer preference and product superiority. I can imagine that people have a similar affinity for Alipay in China.

The small coronavirus outbreak in Northern China led to a strong rally in Mainland Chinese health care stocks, though Hong Kong health care stocks didn’t get the message. There will be a big push to snuff the outbreak out prior to Chinese New Year and the massive travel that will take place. Along with the belief that the Biden Administration will push supportive policies, China’s 2020 green/clean energy output figures have been released, leading to a rally in cleantech, EV, and related metal stocks. We had another simple monster day of Hong Kong buying from Mainland investors via Southbound Stock Connect, totaling $2 billion bought as Southbound Connect trading accounted for nearly 17% of Hong Kong volume versus usually around 9%/10%. The rate of growth is slowing a touch as Tencent, Meituan, and Xiaomi saw big buying while some other names had balanced buys versus sells.

The Hang Seng eased in the afternoon, snapping its 5-day win streak closing off -0.11%, led by Hong Kong volume leaders Tencent, which rose +0.44%, BYD, which gained +1.8%, Alibaba Hong Kong, which fell -2.42%, Meituan, which was up +0.86%, Xiaomi, which fell -3.13%, Semiconductor Manufacturing, which fell -5.08%, Hong Kong Exchanges, which rose +1.58%, Ping An, which was off -0.69%, China Mobile, which fell -0.1%, AIA, which fell -1.33%, and cleantech GCL-Poly Energy, which gained +5.18%. Shanghai & Shenzhen had a strong day gaining +1.07% and +1.53% respectively as EV, cleantech/solar/wind, home appliance makers, and alcohol stocks outperformed. Foreign investors bought a healthy $878mm of Mainland stocks today via Northbound Stock Connect. Bonds and CNY rallied.

The three US-listed Chinese telecom ADRs have apparently appealed to the NYSE to be relisted. Instead of appealing to relisted, they should challenge the Executive Order in court. They were accused of having ties to the Chinese military. While the EO presumes guilt without evidence, a court of law would require the US to produce evidence.

Chinese e-cigarette/vaping company RLX Technology (RLX US) will list on the NYSE today, selling 116mm shares between a price of $8 to $10, which would raise between $932mm and $1.165.

The US-China Business Council sponsored Oxford Economics to calculate the toll of tariffs on the US economy in a recently released report. I’ll provide an overview tomorrow, but a fairly damning critique of tariff policies.

Online education firm TAL Education (TAL US) kicked off Chinese internet earnings this morning with a pre-market open release today. While top-line revenue beat, the company’s expenses ballooned in the quarter, which clipped the bottom line. The company had guided analysts’ expectations down as most understand the company’s operating environment has gotten more competitive due to coronavirus. Analysts won’t like that revenue guidance for the next quarter was below their estimates. Some of this is already baked into the stock, which hasn’t done anything since early July. The company did update their corporate PowerPoint, which articulates their opportunity set in the long run. Worth taking a look at!

- Revenue increased 35% to $1.119B from $829mm YoY versus estimate $1.087B

- Student enrollment increased 46.5% to 3,3997,030 from 2,318,000

- Total operating expenses almost doubled to $740mm from $399mm YoY

- Non-GAAP net income declined -79% to $10.4mm from $49.7mm YoY and versus estimate -$43mm

- EPS GAAP -$0.07versus estimate $0.006 and $0.03 YoY

- EPS Adjusted $0.02 versus estimate $.06 and $0.08 YoY

- Next Quarter Revenue Forecast $1.175B to $1.2B, which would be an increase of 37% to 40% YoY

H-Share Update

The Hang Seng eased in the afternoon session to close off -0.12%/-34 index points at 29,927. Volumes were off -11% from yesterday, which is still 2X the 1-year average while breadth had 25 advancers and 25 decliners (pretty sure that’s two days in row gainers and losers were the same). The 197 Chinese companies listed in Hong Kong within the MSCI China All Shares Index fell -0.25%, with materials +0.73%, communication +0.39%, and financials +0.22%, while industrials -1.7%, real estate -1.68%, tech -1.63%, and health care -0.68%. Southbound Stock Connect volumes were still high but off recent record-setting volumes as Mainland investors bought a massive $2.097B of Hong Kong stocks today as Southbound Connect trading accounted for 16.9% of Hong Kong trading.

A-Share Update

Shanghai & Shenzhen gained +1.07% and +1.53% to close at 3,621 and 2,449 respectively. Volume gained +18% from yesterday, which is 25% above the 1-year average while breadth saw 2,106 advancers and 1,608 decliners. The 512 Mainland Chinese companies within the MSCI China All Shares Index gained +1.66%, led by materials +2.9%, health care +2.36%, staples +2.34%, communication +1.89%, industrials +1.76%, tech +1.6%, and discretionary +1.57%, while real estate fell -0.69%. Northbound Stock Connect volumes were high as foreign investors bought $878mm of Mainland stocks as Northbound Connect trading accounted for an above-average 7.5% of Mainland turnover.

Last Night's Exchange Rates & Yields

- CNY/USD 6.46 versus 6.47 yesterday

- CNY/EUR 7.86 versus 7.83 yesterday

- Yield on 1-Day Government Bond 1.97% versus 1.94% yesterday

- Yield on 10-Year Government Bond 3.13% versus 3.16% yesterday

- Yield on 10-Year China Development Bank Bond 3.52% versus 3.54% yesterday