Ant Group Rises From The Ashes

4 Min. Read Time

Video:

Yesterday, I was interviewed by CGTN on Alibaba's Q4 results.

Click here to view the replay

Key News

Takeaway: The “private” PMI survey is conducted by IHS Markit and focuses on medium and smaller companies, whereas the “official” PMI focuses on larger companies. The “official” PMI includes significantly more companies surveyed than the Caixin PMI, leading to higher volatility than the former. As a diffusion index, the release indicates a month-over-month expansion though the pace of growth slowed. The coronavirus flare ups in Northern China could be to blame for the lackluster release. Another potential culprit is seasonality as factory workers go on vacation for Chinese New Year. Additionally, it has been a cold winter in China, which might be having a negative impact on logistics. The release was not cited as a market moving event.

Ant Group will become a financial holding company, which could lead to the approval of an IPO. Alibaba’s Hong Kong listing reversed from a -4.92% loss in the last half hour of trading on the news. We delve into Alibaba’s stock reaction further though this morning’s news could be a strong catalyst. Confirmation from the company would help. As the saying goes, hopefully Ant Group rises from the ashes reborn and rises again stronger and wiser!

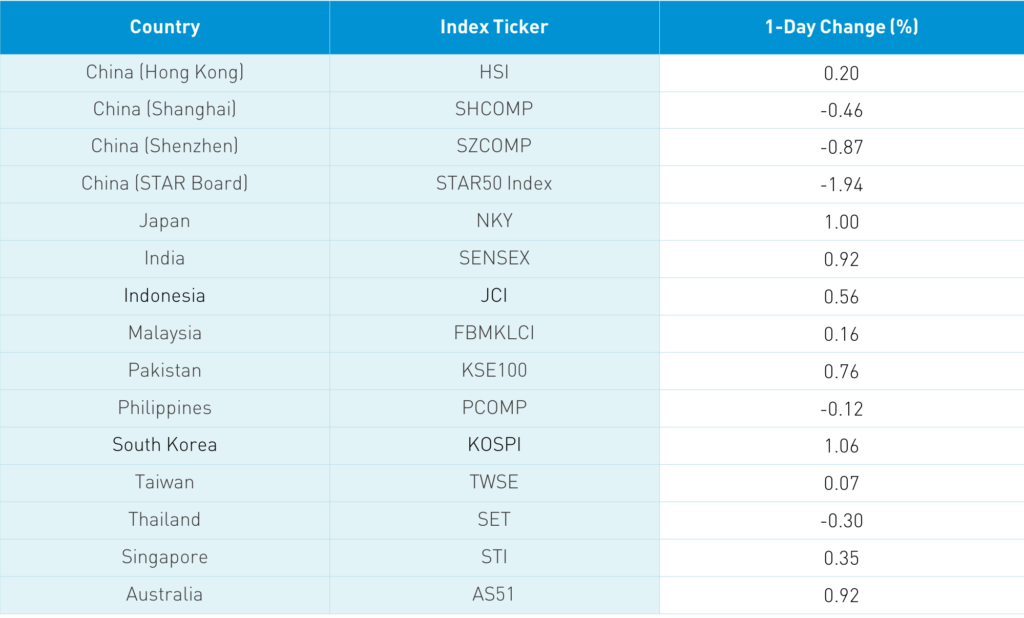

Asian equities were mostly higher today though Mainland China was an outlier to the downside. The PBOC took liquidity out of the financial system, which we have noted is unusual prior to Chinese New Year. The PBOC is worried that easy monetary conditions could create bubbles in real estate and, to a lesser degree, the stock market. However, I suspect that the former could be the main focus.

Shanghai, Shenzhen, and the STAR Board were off -0.46%, -0.87% and -1.94% overnight as the Shanghai rose just above the key 3,500 level on Tuesday. Foreign investors bought a healthy $529mm of mainland stocks today. CNY was flat while bonds backed up a touch.

Southbound Connect, the trading venue allowing Mainland investors to buy Hong Kong shares, had another strong day of inflow as Mainland investors bought $1.59 billion worth of Hong Kong stocks. Southbound Connect trading accounted for nearly 17% of Hong Kong turnover. The pace of Southbound buying has slowed from last month but remains a major factor in Hong Kong’s recent outperformance. The Hang Seng Index gained +0.2% as the Alibaba news lifted the market out of the red at the end of trading. The Chinese companies listed in Hong Kong and within the MSCI China All Shares Index gained +1.05% as many growth companies outperformed. Hong Kong volume leaders were Alibaba HK, which gained +0.38%, Tencent, which gained +1.59% on strong buying via Southbound Connect, Meituan, which gained +4.68%, GCL-Poly Energy, which fell -2.67% after yesterday’s monster move, Xiaomi, which fell -2.53%, Wuxi Biologics, which fell -2.33%, Ping An Insurance, which fell -1.59% post earnings, energy giant CNOOC, which gained +3.55%, BYD, which gained +1.83%, and Hong Kong Exchanges, which was flat.

Alibaba reported strong results yesterday as revenue grew +37% year over year while net income grew +56% year over year. US investors sold the stock sending it lower by -3.85%. What gives? US investors sold due to the specter of anti-monopoly rules and Jack Ma’s vacation plans. Digging deeper, analysts believe the company will invest in growing its business, which could crimp margins in the near future. At the same time, Alibaba’s cloud computing unit reported that revenue increased +50% and broke even for the first time. Who is taking over Jeff Bezos’ seat of CEO at Amazon? Their cloud computing head. Think there is some upside to Alibaba’s cloud computing unit? Alibaba is issuing a green bond led by Citigroup, Credit Suisse, Morgan Stanley, JP Morgan and China International Capital Corporation. The company mentions in the prospectus for the offering that proceeds could be used for an acquisition, which could lift online video players as the company’s ability to attract more eyeballs to the ecosystem via entertainment offerings make sense to me.

Baozun HK was off -6.14% on news that the company is buying Full Jet, which is similar to BZUN, as it helps market luxury good providers navigate China’s e-commerce and social media landscape.

Lost in the Alibaba earnings news, online auto seller Autohome (ATHM US) also reported financial results yesterday that beat analyst expectations.

Next Tuesday after the close in New York MSCI will release the pro-forma for its Quarterly Index Review. The big questions going into the review: will STAR Board stocks be included in MSCI indexes as a dozen STAR Board stocks have been added to Northbound Stock Connect? My prediction: hard to say, but the index provide may wait until the June 1st Semi-Annual Index Review to add the shares.

The Wall Street Journal had two good articles worth reading. The first provided an overview of Hong Kong-listed delivery company Meituan. The second was on Biden’s team and their different views of China as the title takes a page from Doris Kearns Goodwin’s must-read book Team of Rivals: The Political Genius of Abraham Lincoln. Lincoln hired his primary challengers to key administration posts. Lincoln would always have them debate before making a decision, which was different (not saying worse) than Trump, who surrounded himself with like-minded thinkers. Ultimately, I believe John Kerry will play an outsized role due to his longstanding close relationship with Biden. Kerry receives a great deal of attention for wanting to solve global climate issues, which will require cooperation with China and India. I also believe that Kerry, as a veteran, knows that the US and China need better dialogue and communication.

H-Share Update

The Hang Seng overcame morning losses to gained +0.2%/+58 index points to close at 29,307. Breadth was off with 15 advancers and 33 decliners while volume was off -1.9% from yesterday but still 57% higher than the 1-year average. The 196 Chinese companies listed gained +1.05% led by discretionary +2.77%, communication +1.53%, industrials +0.89% while real estate -0.7%, materials -0.36% and staples -0.15%. Southbound Stock Connect volumes were high though off levels seen recently as mainland investors bought $1.594B of HK stocks as Southbound Connect trading accounted for 16.1% of HK turnover.

A-Share Update

Shanghai & Shenzhen bounced around the room to close -0.46% and -0.87% at 3,517 and 2,380. Volumes increased +5.83% from yesterday and 9% above the 1-year average i breadth saw 911 advancers and 2,939 decliners. The 511 mainland Chinese companies within the MSCI China All Shares were off -0.711% with staples +0.99%, health care +0.6% and financials +0.4% while tech -2.56%, real estate -1.14% and utilities -0.87%. Northbound Stock Connect volumes were elevated as foreign investors bought $529mm of mainland stocks today as Northbound Connect trading accounted for 7.3% of mainland turnover.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.46 versus 6.46 yesterday

- CNY/EUR 7.77 versus 7.77 yesterday

- Yield on 1-Day Government Bond 1.90% versus 2.15% yesterday

- Yield on 10-Year Government Bond 3.21% versus 3.19% yesterday

- Yield on 10-Year China Development Bank Bond 3.64% versus 3.60% yesterday

- China’s Copper Price -0.83% overnight