Market Corrections Are Tears in The Rain, Week in Review

4 Min. Read Time

Upcoming Webinar:

Join us on Thursday, March 2nd at 11:00am EST for

FAQ Webinar with Quadratic Capital Portfolio Manager, Nancy Davis

Click here to register

Week in Review

- Reopening, rising yields, and strong commodity performance drove the outperformance of cyclicals over growth in China all week in a bullish environment. The price of copper popper +4% in China Monday.

- After beating analyst estimates on Q4 2020 revenue, search engine Baidu announced an electric vehicle partnership with Geely Automotive Tuesday.

- Corrections in equity markets got real in China on Wednesday as nearly all sectors ended up in the red in Hong Kong.

- Green energy names were a bright spot in Mainland trading on Thursday as investors anticipate the release of new policies supporting the sector.

Key News

Asian equities were taken to the woodshed overnight. Yesterday’s US Treasury yield spike reminded me of the 2013 taper tantrum when Ben Bernanke said they were thinking of slowing quantitative easing. Just as Bernanke did not stop quantitative easing in 2013, policymakers this time around do not appear to be taking their foot off the gas pedal as markets become worried about rising inflation, as evidenced by rising commodity prices.

Global markets and economies are more interconnected than ever as yesterday’s US equity market action rippled across the globe. The Philippines either did not get the message or had a great time on their day off yesterday as the country’s market was a rare bright spot in Asia overnight.

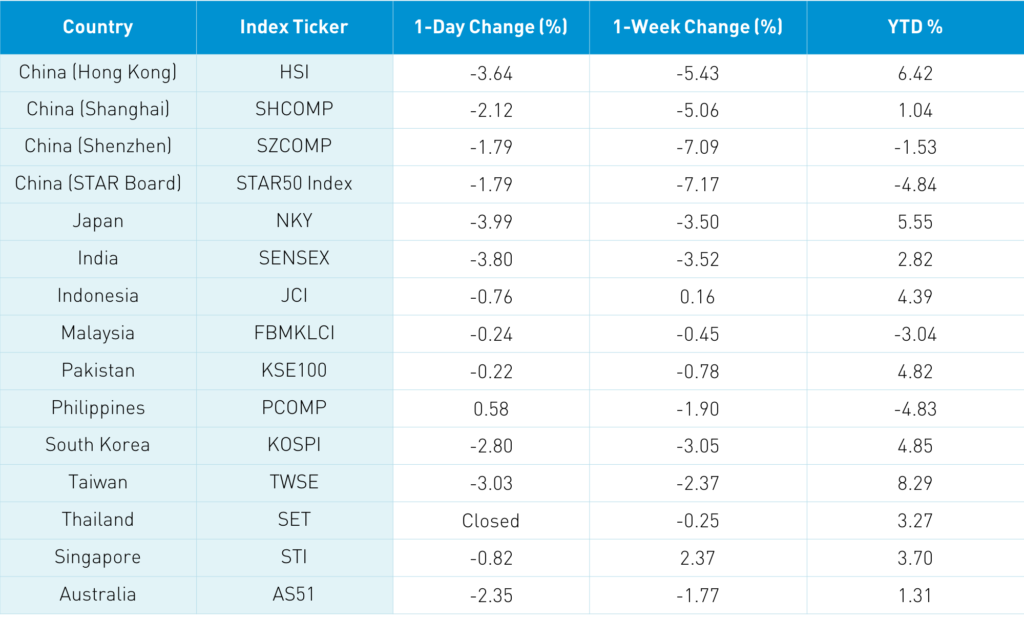

How bad was the selloff in Asia? Japan’s Nikkei 225 was off -3.99% with 3 advancing stocks and 222 down! India’s Nifty 50 was down -3.76% with ZERO advancers. Ironically, as we get closer to the end of quarantines due to the vaccine rollout accompanied by improving economic data we are experiencing a selloff. Ultimately, I believe Asia and emerging markets will benefit from capital being redeployed from US equities due to valuations post-an epic ten-year run. Similar to the final scene from Ridley Scott’s 1982 hit Blade Runner, corrections are like tears in the rain for the long-term investors, i.e. they get washed away. The 10-Year US Treasury yield is 1.47% versus 1.33% a year ago. The fact that it was a Friday, the month-end, and the MSCI index rebalancing day did not help markets. However, our broker called last night’s market action “orderly”.

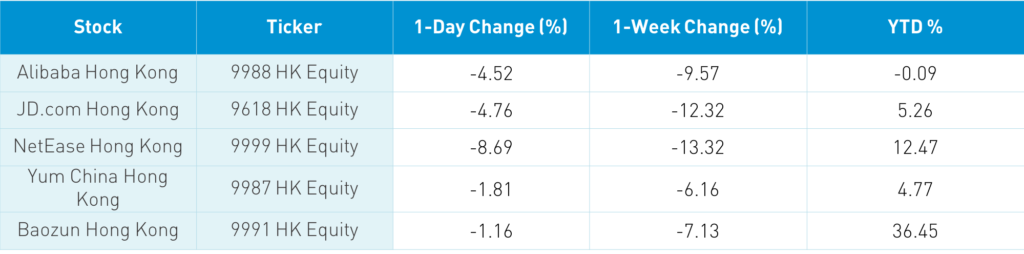

The Hang Seng lost -3.64% as Hong Kong volume leaders included Tencent, which fell -4.19%, Meituan, which fell -8.21%, HK Exchanges, which fell -5.36%, Alibaba HK, which fell -4.52%, Xiaomi, which fell -5.77%, Kuaishou Technology, which cratered -8.79%, BYD, which dropped -8.79%, Wuxi Biologics, which fell -7.91%, Ping An Insurance, which fell -2.36%, and GCL-Poly, which gained +3.26%. Southbound Stock Connect, the trading venue that allows Mainland investors to buy Hong Kong stocks, experienced a rare sell day, liquidating -$979 million worth of Hong Kong stocks.

Shanghai, Shenzhen, and the STAR Board were off -2.12%, -1.79%, and -1.79%, respectively. The only bright spot was in terms of breadth, which was not too bad with 1,646 advancers and 2,165 decliners. That being said, it was a relatively ugly day. Foreign investors sold -$871 million worth of Mainland stocks today as Shanghai stocks were net sold and Shenzhen stocks were net bought. CNY depreciated slightly as the US dollar rallied while bonds sold off and copper was off a touch.

MSCI will be adding three US-listed Chinese companies to their indices today and increasing the weights of two. VNET, LI, and DQ should see a strong uptick in trading volume at the end of the day as passive investors buy the stocks at the end of the day to match the “new” index on Monday. BEKE is seeing a pickup in its weight along with HUYA. I am not predicting they will go up, but volume will increase dramatically. For fun, pull up one of the three tickers to watch the power of passive as it will be on full display at 3:59.

There is chatter that Autohome (ATHM US) will file to list in Hong Kong potentially as soon as next week.

After the market’s close, Hang Seng Indexes announced that Alibaba Health, real estate developer Longfor Group, and hot pot restaurant Haidilao will all be added to the Hang Seng Index on March 15th.

Tencent’s WeDoctor may list in Hong Kong as early as next month.

Sina and Weibo are expected to release earnings after the market’s close today, though Sina will be going private.

H-Share Update

The Hang Seng opened lower and stayed there to close -3.64% at 28,980. Volume increased +24% from yesterday, which is 215% of the 1-year average while breadth was abysmal with 2 advancers and 49 decliners. The 196 Chinese companies listed in Hong Kong and within the MSCI China All Shares Index were smoked -4.37% with materials -7.02%, discretionary -6.66%, tech -4.86%, staples -4.79%, health care -4.62%, energy -4.24%, communication -4.21%, industrials -4.05%, financials -3.36%, utilities -1.17% and real estate -0.99%. Southbound Stock Connect volumes were moderate as Mainland investors sold a healthy -$979 million worth of Hong Kong stocks today as Southbound trading accounted for 12% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen were off -2.12% and -1.79% closing at 3,509 and 2,293, respectively. Volumes were off -2.81%, which put them just above the 1-year average while breadth was not so bad with 1,646 advancers and 2,165 decliners. The 511 Mainland stocks within the MSCI China All Shares Index were off -2.64% with materials -3.75%, energy -3.37%, financials -3.16%, discretionary -3.15%, industrials -2.87%, staples -2.68%, communication -2.18%, real estate -1.895, tech -1.69%, health care -1..68%, utilities -1.04%. Northbound Stock Connect had elevated volumes as foreign investors sold -$871 million worth of Mainland stock and Northbound trading accounted for 8.7% of Mainland turnover.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.46 versus 6.45 yesterday

- CNY/EUR 7.84 versus 7.89 yesterday

- Yield on 1-Day Government Bond 1.71% versus 1.61% yesterday

- Yield on 10-Year Government Bond 3.28% versus 3.27% yesterday

- Yield on 10-Year China Development Bank Bond 3.75% versus 3.74% yesterday

- China’s Copper Price -0.33% overnight