Two Sessions Tailwind, Week in Review

4 Min. Read Time

Week in Review

- Both the official and IHS Markit/Caixin PMIs for February were released Monday, indicating an expansion though at a lower rate than in January as Chinese New Year reduced the number of workdays in February.

- Asian equities were mixed this week as the taper tantrum proved to still have legs as commodities rallied and US treasury yields continued to climb. Growth stocks continued to sell-off.

- Investors buying the dip in growth stocks and speculation of a cut to banks’ reserve requirement ratio (RRR), which would free up cash for lending, led to a rally in Hong Kong and Mainland Chinese equities Wednesday.

- However, the market correction resumed Thursday. On a positive note, Chinese travel agent Trip.com reported better than expected results for the fourth quarter of 2020.

Key News

Asian equities opened lower following Fed Chair Powell’s disappointing speech yesterday before reversing and limiting losses due to Premier Li’s opening speech at the Two Sessions, China’s major policy meetings occurring over the next week.

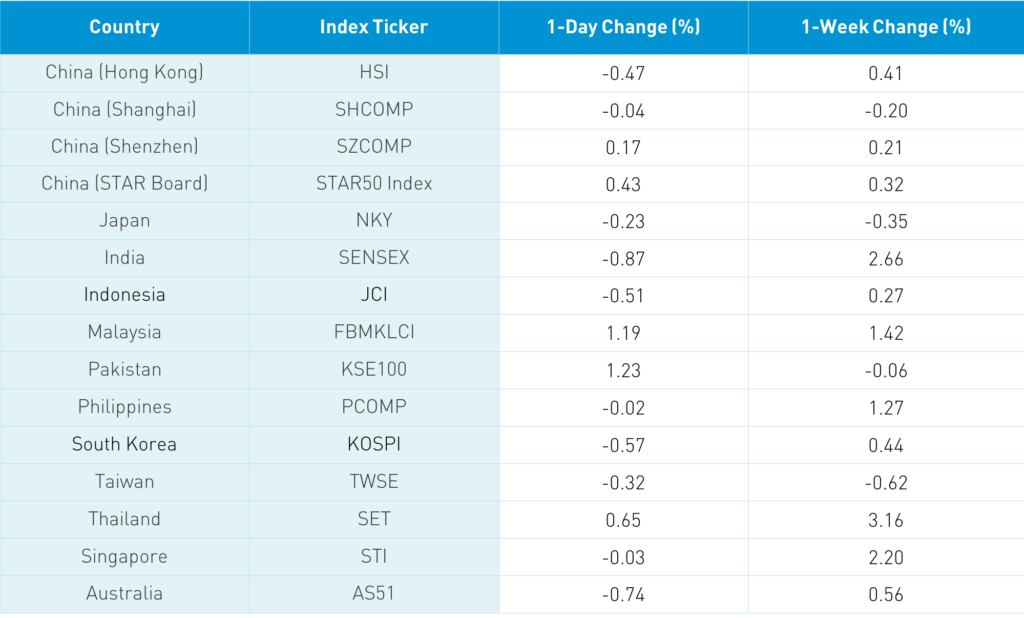

Close your eyes and guess what the week-to-date performance of China, Hong Kong, and Asia stock markets was? Take a look below. I would have guessed far worse as well. Media headlines and our brains are hard-wired in a way that often distorts the data-driven reality.

Premier Li’s speech articulated the areas of focus for China along with a release of the draft 14th Five Year Plan. As investors, we want to align ourselves with these policies. The key point that surprised markets to the upside was that China would run a fiscal deficit of 3.2% versus expectations of 3% or less. The market has been very worried about fiscal and monetary support being pulled quickly and the speech helped soothe those fears. Other key points included:

- GDP target of +6% though economists expect GDP to grow 8% this year

- Reducing debt will be a focus as coronavirus bond issuance will be halted while “defusing risks in the financial sector” will be a focus. The amount of debt issued will fall from 2020 levels.

- Raising domestic consumption will be a priority.

- Raising R&D investment in key technologies such as semiconductors to reduce foreign dependency will be another.

- The government will target 11 million new urban jobs and an unemployment rate of 5.5%.

- Raise the percentage of the population living in cities to 65% of the population

- Reduce carbon emission per unit of GDP in 2020 by 18%

On the downside, it is proposed that China’s retirement age of 60 for men and 50 for women will be raised. I believe the Two Sessions should be a catalyst for consumption names, e-commerce, solar/wind, EV, 5G, and semiconductors. We will also see earnings releases for Chinese companies listed in the US, Hong Kong, and Mainland China this month.

The Hang Seng Index opened -1.95% and hit a morning low of -2.6% before reversing on Premier Li’s speech to close -0.47% though the broader Hang Seng Composite was off -0.75% and Chinese stocks listed in Hong Kong were off -0.89%. Hong Kong volume leaders by value traded were Tencent, which fell -1.59%, Meituan, which fell -0.88%, Xiaomi, which fell -3.74%, Alibaba HK, which fell -0.09%, Hong Kong Exchanges, which fell -0.66%, China Construction Bank, which gained +1.72%, China Mobile, which gained +3.36%, BYD, which fell -1.02%, Ping An Insurance, which fell -0.97%, and ICBC, which gained +3.6%. Mainland investors bought $305 million worth of Hong Kong stocks today. Tencent was a beneficiary of the Mainland buying while Meituan and Xiaomi were trimmed.

Shanghai, Shenzhen, and the STAR Board also opened lower, hitting morning lows of -1.34%, -1.66%, and -1.38%, respectively, before reversing to close -0.47%, +0.17%, and +0.43%. Volumes were off a touch from yesterday as I would rather see up days on higher volumes. We did see the YTD/2020 winners that were kicked to the curb recently bought back while the Mainland volume leaders by value traded were Kweichow Moutai, which gained +1.33%, broker East Money, which gained +1.89%, liquor stock Wuliangye Yibin, which pulled a James Bond gaining +0.07%, Longi Green Energy, which gained +1.37%, Sungrow Power, which ripped +6.13%, Ping An, which fell -2.09%, BOE Technology, which fell -1.58%, and BYD, which fell -1.07%. Foreign investors bought $81 million worth of Mainland stocks via Northbound Stock Connect in a volatile week with a net outflow of -$129 million. CNY was off a touch while bonds rallied and copper was smoked.

US investors will need to sell Xiaomi due to the Executive Order over the coming weeks. I have been complaining that I do not understand why the companies have refrained from challenging the Executive Order in court. Software company Luokung Technology has done just that, stating it has no ties with China’s military.

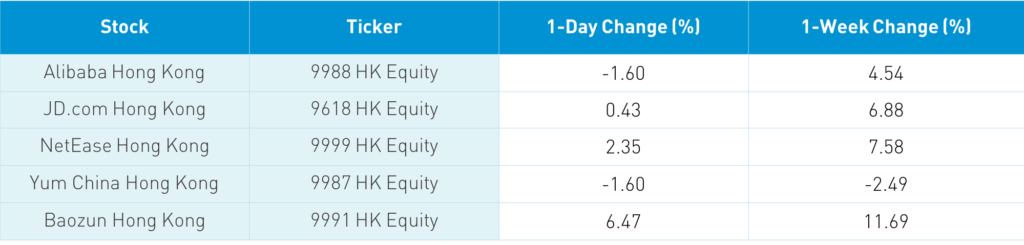

US-listed Chinese ADRs with dual listings come at a big discount to their Hong Kong share classes. BABA -1.61%, JD -2.95%, and NetEase -1.09%.

Controversial online education firm GSX beat analyst expectations on revenue while missing on the bottom line as they reported Q4 earnings before the US market open.

Q4 earnings continue next week. Pinduoduo and JD.com are expected to report next Thursday and Weibo and Sina next Friday. Export/import data for February will be released over the weekend.

H-Share Update

The Hang Seng opened lower but fought back to close -0.47% at 29,098. Volume was up +7% overnight, which is 159% of the 1-year average while breadth was mediocre with 18 advancers and 33 decliners. The 519 Chinese companies listed in Hong Kong and within the MSCI China All Shares Index were off -0.89% with utilities +1.15%, staples +1.03%, financials +0.67%, and energy +0.61%. Meanwhile, materials -4.25%, healthcare -2.66%, tech -1.66%, communication -1.61%, real estate -1.37%, industrials -1.05% and discretionary -0.61%. Southbound Stock Connect volumes were moderate as Mainland investors bought $305 million worth of Mainland stocks today as Southbound Connect trading accounted for 13% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen opened lower and then bounced around the room to diverge -0.04% and +0.17%, closing at 3,501 and 2,298, respectively. Volume was off -9% from yesterday, which is 101% of the 1-year average while breadth was decent with 2,726 advancers and 1,119 decliners. The 519 Mainland stocks within the MSCI China All Shares Index lost -0.6% with communication +0.88%, tech +0.22% and staples +0.04% while materials -2.49%, real estate -2.33%, industrials -1.17%, financials -0.64%, energy -0.59% utilities -0.45%, discretionary -0.43% and healthcare -0.27%. Northbound Stock Connect volumes were moderate/high as foreign investors bought $81 million worth of Mainland stocks. Northbound Connect accounted for 6.8% of Mainland turnover.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.50 versus 6.47 yesterday

- CNY/EUR 7.75 versus 7.78 yesterday

- Yield on 1-Day Government Bond 1.36% versus 1.43% yesterday

- Yield on 10-Year Government Bond 3.25% versus 3.27% yesterday

- Yield on 10-Year China Development Bank Bond 3.69% versus 3.72% yesterday