Economic Data Doesn’t Disappoint While The Market Does

3 Min. Read Time

Upcoming Event

Join us on Thursday, March 25th at 9:00 am EDT for our event:

KraneShares’ Future of Green ETFs Summit.

Click here to register.

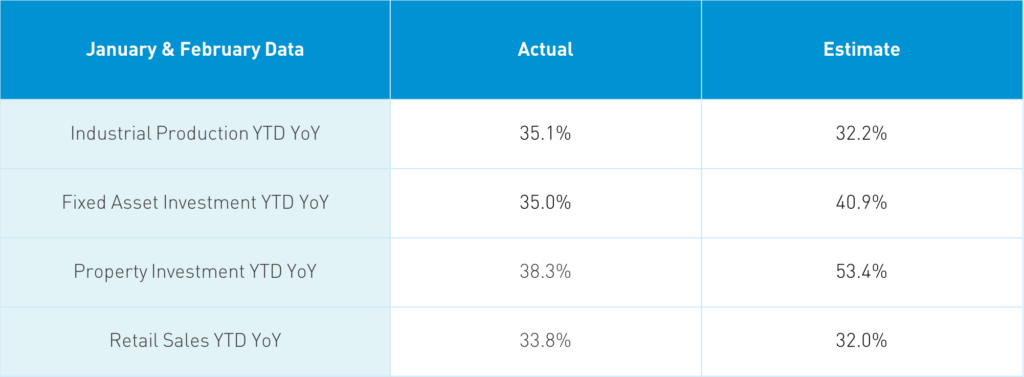

January/February 2021 Economic Data Release

Takeaway: January and February data were combined to provide a better comparison because Chinese New Year’s came in January last year and February this year. The year-over-year (YoY) comparison was going to be an easy one as China entered its quarantine during this period. The data did not disappoint. However, Fixed Asset Investment came in a touch light.

Meanwhile, Industrial Production was powered by the manufacturing category, which grew +39.5% YoY led by pharmaceuticals, which grew +41.6%, rubber, which grew +51.6%, metal products, which grew +59.5%, general equipment, which grew +62.4%, auto manufacturing, which grew +70.9%, and machinery, which grew +69.4%. The data also reveals the demand generated by work from home as computer and mobile phone output is well above average. Electric vehicle production is also surging. Fixed Asset Investment was a touch light but the figures themselves were very impressive. The same can be said for Retail Sales as restaurants saw 68.9% growth YoY while communication appliances (i.e. phones) +53.1%, jewelry +98.7% and auto +77.6%. Property development investment was driven by strong property sales and the robust value of the sales.

As such, the question remains: why was the market off?

Key News

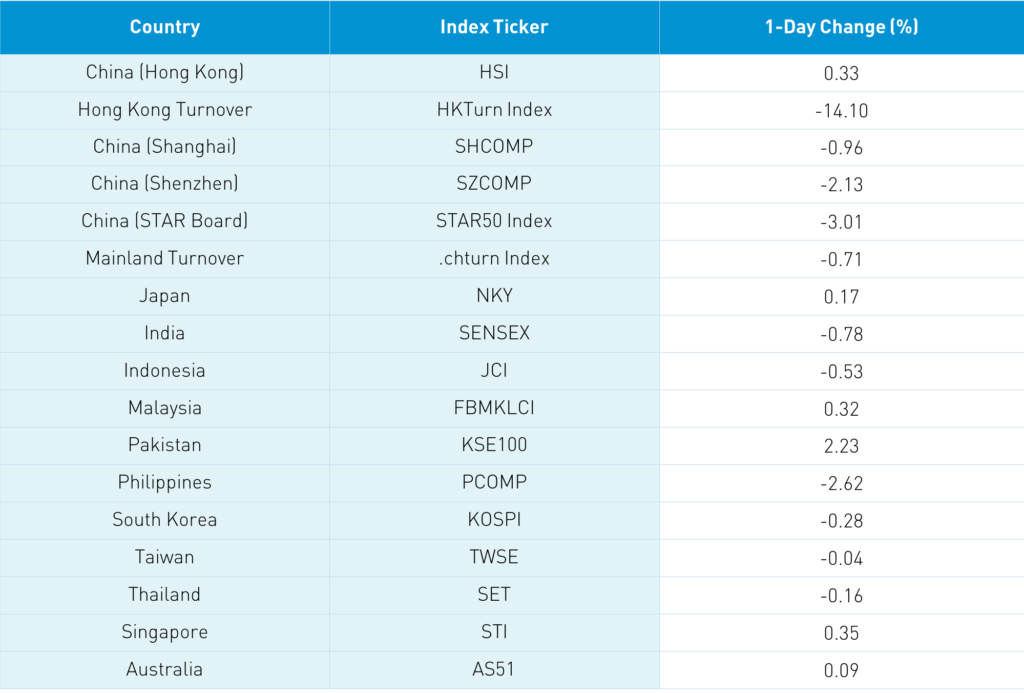

Asian equities were largely lower as US Treasury yields rose overnight despite the strong Chinese economic data release. Mainland investors were more focused on repo rates (short-term lending rates) as the PBOC rolled over RMB 100 billion in maturing notes with another 100 billion. What spooked the market was a small rise in both overnight and seven-day rates. Tight monetary conditions are the market’s biggest concern despite the PBOC saying “no sharp turns”. Because of the good economic data, policymakers are increasingly likely to believe the economy does not need support. I would agree though it will be pulled slowly, incrementally over time.

This concern is being combined with a cyclical/value rotation as the global economy reopens. While I agree that cyclical plays have an opportunity in the short run as hotels, airlines, amusement parks, and the like begin to see revenue return. However, I believe it will be just that: a short run opportunity. Combine that with large retail participation in global markets, and this rotation has a dramatic effect. Considering that China was the “First In First Out” regarding coronavirus, we know that many of the “work from home” stocks have come out of the quarantine in better shape today than previously.

The Office of Foreign Assets Control (OFAC) dropped Xiaomi from the Executive Order sanction list on Sunday, following a judge’s halt to the ban on Friday. While the company did not win the case, MSCI announced that Xiaomi will not be dropped from its indexes. The legal challenge is likely to be repeated by others as it provides a path for reversing the Executive Order.

Our friend Dan asked about food’s role in China’s CPI, which fell due to a fall in pork prices as China’s pig population grows. In doing some research on the subject, I stumbled across some data on China’s pork consumption. According to the CME, China consumes 53 pounds of pork person annually. This reaffirms my hope not to come back as a pig in China in my next life.

It is being widely reported that Baidu’s Hong Kong listing is 15X oversubscribed. Meanwhile, Autohome (ATHM, 2518 HK) listed in Hong Kong today, gaining +2.1%.

H-Share Update

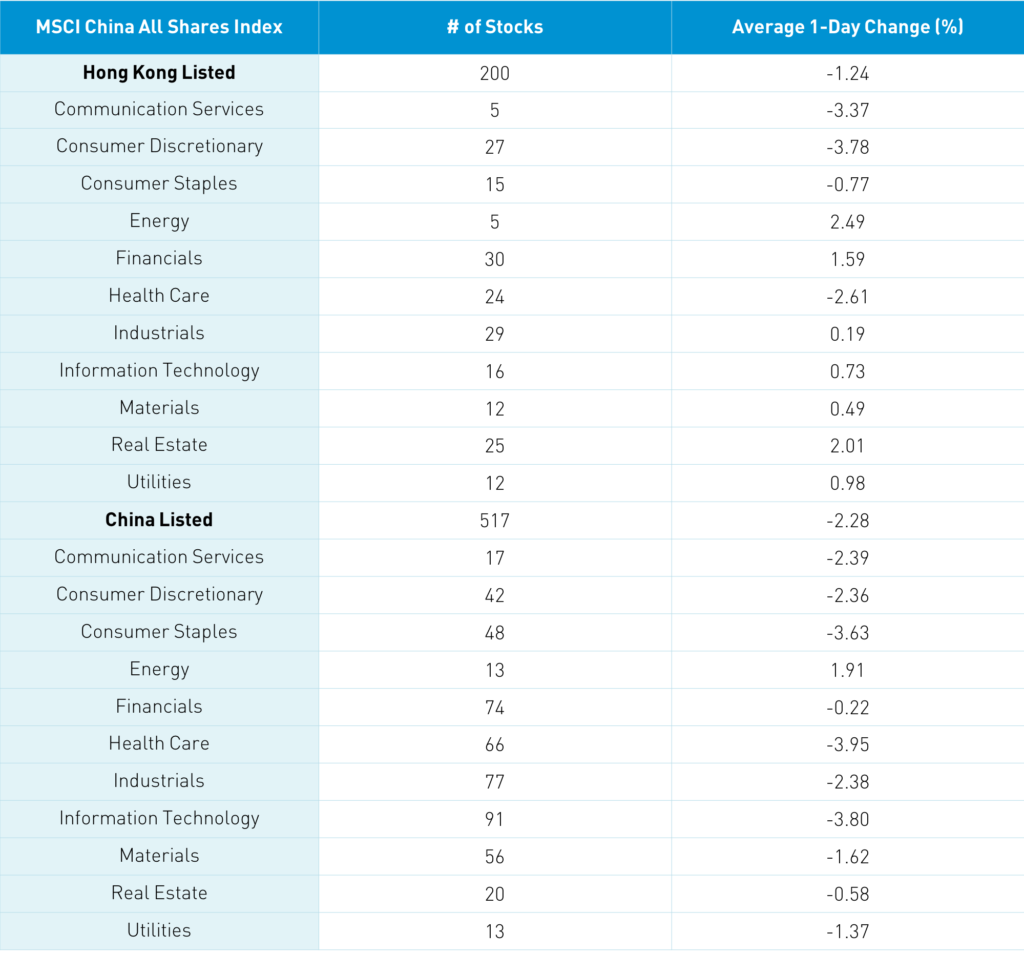

The Hang Seng Index gained +0.33% led by cyclical/value sectors at the expense of growth stocks as the Chinese companies listed in Hong Kong and within the MSCI China All Shares Index declined -1.24%. Growth sectors such as discretionary, communication and healthcare were off while energy, real estate and financials gained. Regulatory concerns account for some of the uncertainty as anti-competitive practices will be eliminated. Hong Kong volume leaders by value were Tencent, which fell -3.46%, Xiaomi, which gained +7.03% on news discussed below, Meituan, which fell -4.74%, Alibaba HK, which fell -2.04%, JD.com, which fell -6.17%, China Construction Bank, which gained +3.28%, HK Exchanges, which fell -1.68%, AIA, which gained +4.17%, Ping An, which gained +0.98%, and China Mobile, which gained +0.1%. Southbound Connect flows were moderate/light as Mainland investors sold $602 million worth of Hong Kong stocks as Southbound Connect trading accounted for 14.8% of Hong Kong turnover. Tencent, Meituan and HK Exchanges were net sells today.

A-Share Update

Shanghai, Shenzhen, and STAR Board were off -0.96%, -2.13%, and -3.01%, respectively, as growth names underperformed. The Mainland stocks within the MSCI China All Shares Index were off -2.28% led by healthcare, staples, discretionary, and communication. Mainland volume leaders by value traded were Kweichow Moutai, which fell -2.5%, Longi Green Energy, which fell -10% on a broker downgrade, CATL, which fell -8.54%, TCL Tech, which gained +2.46%, Wuliangye Yibin, which fell -5.08%, GEM, which gained +4.32%, Sungrow Power, which fell -9.41%, BOE Tech, which gained +0.82%, Tongwei, which fell -7.69%, and BYD, which fell -4.08%. Northbound Stock Connect volumes were moderate as foreign investors bought $567 million worth of Mainland stocks as Northbound Connect trading accounted for 7.2% of Mainland turnover. CNY appreciated a touch versus the US dollar, bonds were mixed, and copper gained.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.50 versus 6.51 Friday

- CNY/EUR 7.75 versus 7.75 Friday

- Yield on 1-Day Government Bond 1.65% versus 1.50% Friday

- Yield on 10-Year Government Bond 3.27% versus 3.26% Friday

- Yield on 10-Year China Development Bank Bond 3.67% versus 3.67% Friday