China Internet Stocks Hit By One-Two Headline Punch

2 Min. Read Time

Today’s news provided a one-two punch to China Internet stocks.

The SEC today announced they would start identifying the companies that do not allow the Public Company Accounting Oversight Board (PCAOB), a US regulatory agency that oversees public company accounting and reporting, to inspect their audit books as part of the Holding Foreign Companies Accountable Act. As we noted in a previous article, the SEC will accept reviews of audit work done by the “Big Four” US accounting firms, which audit most US-listed Chinese companies. The SEC will also require listed firms to provide documentation that they are not owned or controlled by a foreign government, which should not be a problem for China internet firms, which are majority privately owned.

While this move and the framework to avoid delisting were widely telegraphed, today's Reuters headline may have overemphasized the risk.

As for China regulation, we also had Tencent’s earnings call this morning, during which President Martin Lao addressed the new fintech regulations (need to hold 30% of loans, no loans to college students, max loan size RMB 200k) and said that the company is adhering to these rules with no impact to their fintech business.

Bloomberg had an article that the PBOC would create a data privacy unit, which would scrutinize internet firms' user data practices, though I have not seen this substantiated anywhere else. The market seems to have been spooked by the multiple negative headlines.

While today's price movement was dramatic, here are a few key points to consider:

- The CSI Overseas China Internet Index has seen a dip recently due to rising yields, a cyclical rotation, and increased regulatory scrutiny of the Fund’s holdings. The fund is down -26.3% from its peak in February.

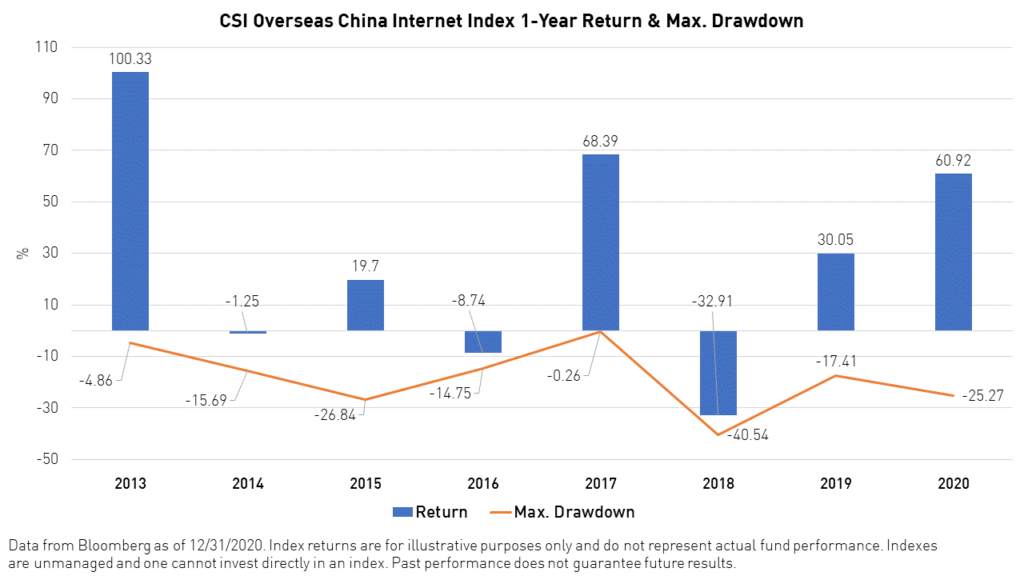

- The China internet sector can be volatile and drawdowns such as this have happened before. For example, 2020 saw a 25% maximum drawdown, but a 61% return for the year (see chart below).

- However, the traditional “old economy” within China/EM, which includes financials, energy, and utilities does not represent a long-term value proposition. The rotation to value is therefore likely not a long-term phenomenon for China/EM.

- China internet companies remain the drivers of growth in the economy with a continuous ability to deliver revenue growth. JD.com and Pinduoduo both just beat estimates on revenue, demonstrating their ability to grow revenues even without a pandemic.

- China retail sales overall were up 33.8% in the first two months of 2021 and online sales grew 21%. We consider such robust growth in online sales to be a positive signal for all E-Commerce players in 1Q21.

- Furthermore, the higher beta* nature of China internet companies might offer a stronger rebound out of the dip. We believe present market volatility represents a buying opportunity for long-term investors.

*beta is a measure of a security's volatility relative to the overall market.